Market slowdown: is there an end in sight?

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

12th Feb 2008

Dan O'Brien is our guest blogger, commenting on the latest Daft research on the Irish property market.

The future of Ireland's property market will be determined not only by domestic supply and demand factors, but also by developments in international equity prices, European interest rates and migration flows. Looking first at stock markets, recent weeks have seen economic uncertainty rise sharply as international developments have added to home-generated worries. The US economy has slowed sharply and equity markets almost everywhere, including Ireland's, have suffered badly.

But the global gloom is overdone. Investor sentiment internationally has over-reacted to America's woes. Moreover, the US policy response to the slowdown has been unprecedented, both in its speed and its magnitude. Outside the US, the rest of the global economy is enjoying one of its strongest periods of economic expansion ever. As most of this is driven by strong fundamentals, we at the Economist Intelligence Unit are forecasting only a modest slowdown globally in 2008 and continued strong expansion over the medium term.

This underlying strength of the world economy augurs well for Ireland as one of the most globalised economies on the planet.

From global equities to Irish rents

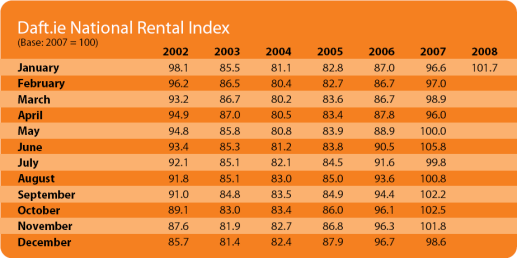

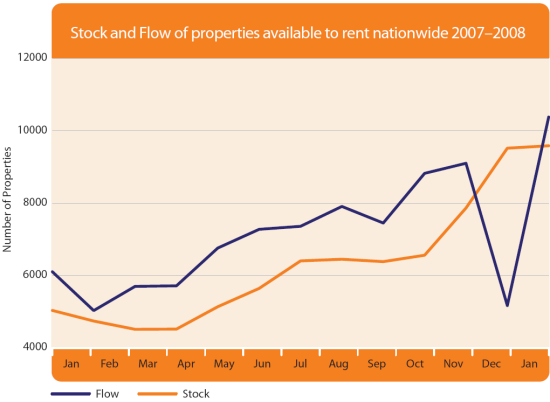

It is too early to tell whether nervousness internationally will cause a further deterioration in sentiment in Ireland. It is certainly to be hoped that it will not, because there is considerable downside risk for the Irish economy currently, with most of it related to the property market. Nationwide, the supply of property available for rent on Daft has almost doubled in the past year, with most of the surge taking place in the second half of the year. Although demand for rental properties is likely to have expanded too, it will not have matched the doubling in supply. The inevitable result is to be seen in rents: the strong increases in the past couple of years are slowing sharply.

Why the sudden surge in supply? The most likely explanation is those who had invested in property but had not sought a rental income are now doing so. As interest rates rose, so did debt servicing costs, while at the same time capital gain evaporated as prices stopped rising. The likely result - those who had been willing to forego rental yield are less and less willing to do so.

If the increase in rental supply continues, watch for falling rents.

Interest rates: what chance of relief from Frankfurt?

The US Federal Reserve cut interest rates by 125 basis points in the last week in January. There have been frequent calls for the ECB to follow suit. Although the euro area economy does not face the same domestic imbalances that could tip it into recession, it will feel the drag from lower growth in the US (though to what extent is the subject of fierce "decoupling" debate among economists). As the European economic cycle is now past its peak, the low-point of the downturn could be made deeper by external factors. But the ECB will want to see much hard data confirming a slowdown before acting.

With the next move in interest rates a crucial determinant of sentiment in the Irish property market, it is important to look at how the ECB is likely to act. Provided euro area growth slows gradually, as we at the Economist Intelligence Unit anticipate, the ECB is likely to stay its hand in the months ahead. There are four reasons explaining why the ECB will not follow the Fed in lowering interest rates. First, in general the ECB prefers cruise control to the Fed's aggressive use of accelerator and brake when using the interest rate tool. Second, whereas the Fed is often accused of being too willing to do the bidding of financial market participants, the ECB is deaf to traders' cries of pain. Third, with little hard evidence that the six-month old credit crunch is pushing up retail interest rates significantly, the bank continues to worry about rising indebtedness and its consequences. Fourth, as the ECB is set to miss its inflation target by the widest margin ever, it is not about to take chances with price stability. With survey evidence pointing to rising inflationary expectations, it has repeatedly said that it is ready to raise rates if it sees evidence of second round effects (i.e. wages chasing prices).

Don't bank on a cut in interest rates in the months ahead.

The supply-side miracle

In addition to these important external factors, which will affect demand, local factors - determining supply - are also important. Figures for the first nine months of 2007 show the most rapid decline in housing completions in Ireland in the forty-year history of the index. What's more, the pace of the decline is accelerating. From a rate of zero year-on-year growth in the final quarter of 2006, the contraction reached -23% by the third quarter of 2007. How low could it go and where will it settle after the current period of instability? Although many estimates of where the long term trend in housing output range between 50,000 and 60,000, this seems very high when long-term trends are

considered. As the graph illustrates, supply in the UK, US and euro area is subject to a certain degree of short and medium term volatility, but long-term averages are remarkably stable. Indeed, it is the relative inflexibility in supply, when considered against the backdrop of bettering financing conditions and rising incomes that explain the upward trend in property prices in most rich countries in the past decade.

Ireland's supply side, however, has been spectacularly different to the rest of the core of the developed world over the past decade. While the quarter-century period from when the data were first gathered (1970-95) followed the same stable pattern as elsewhere, the subsequent period is simply without parallel. The demand conditions in Ireland over the past decade have been uniquely strong relative to other countries, both in terms demographics and incomes. But they have not, however, been so unique as to explain the increase in supply. And one of the basic rules in economics is that when supply increases more rapidly than demand, downward pressure on the price follows.

History suggests that housing over-supply in Ireland is underestimated.

Migration: a two way street

One of the drivers of demand for property has been a rapidly expanding population. With the highest fertility rates in Europe

and rates of inward migration unsurpassed by any other continental country, Ireland's population grew by 19.4% between

1995 and 2006. But labour mobility is a two way street. Recent immigrants to Ireland are likely to be unusually mobile, and can

be expected to up sticks quickly not only if they lose their jobs, but even if opportunities elsewhere appear relatively better.

Nor should the possibility of the return of "indigenous" emigration be discounted. It is little remarked upon, but young Irish people have continued to leave the country in large numbers. In the five years from 1997 - the very height of the boom - outflows averaged 28,000 a year. In the previous five year period, when unemployment was in double digits, the average number leaving the country was 33,000. Although Irish emigrants recently have probably left for short periods of horizonbroadening, my guess is that the Irish remain unusually mobile. Moreover, the prospect of leaving home in an era of cheap airfares, email and Skype is considerably less daunting than it was the last time the country haemorrhaged its youth.

There is considerable scope for a marked turnaround in the recent demographic trends which have supported property prices.

HIGHLIGHTS:

The Daft.ie National Rent Index

Stock and Flow of properties available to rent nationwide 2007-2008

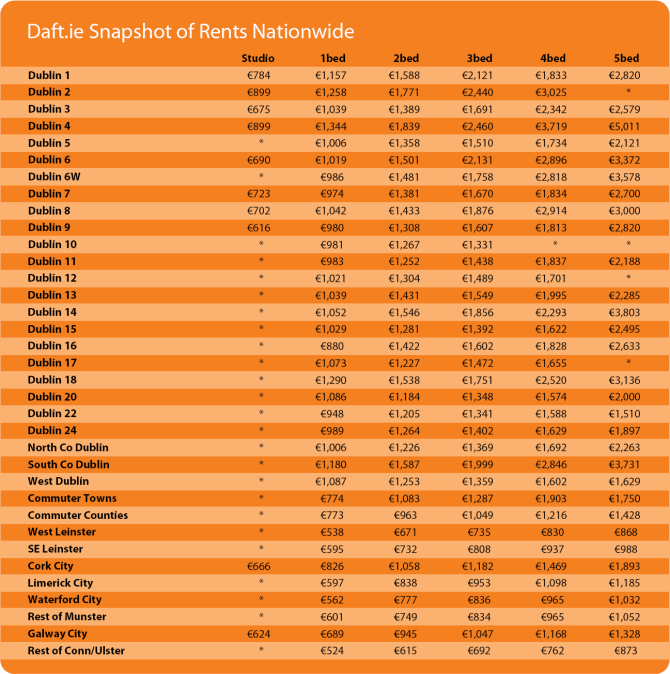

SNAPSHOT:

Average Rents across Ireland in Q4 2007