2010: a turning point for Ireland's property market

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

7th Jan 2010

Alan McQuaid, Chief Economist, Bloxham Stockbrokers, commenting on the latest Daft research on the Irish property market.

For the vast majority of people 2009 was a year well and truly to forget, with the Irish economy contracting at a record rate and unemployment soaring as a result. The global financial crisis continued to dominate matters with the availability of credit or rather the ongoing lack of it, remaining the key theme. Against this background it was hardly surprising that the domestic property market continued to suffer, with house prices falling sharply all across the country. Indeed, the latest property review from daft.ie makes very sober reading, with little indication that things will improve dramatically on the housing market front any time soon.

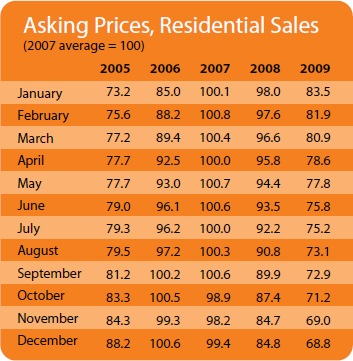

According to the survey, asking prices last year were down around 19% on average following a decrease of almost 15% in 2008, while in the final quarter of 2009 they dropped to just over €242,000, a staggering €110,000 or so below their peak. Dublin City Centre has been the worst hit area during the housing market downturn and this was again evident in the latest review, with asking prices in the fourth quarter of last year down 42.5% from their peak. However, all areas of the capital saw sizeable falls, with North County Dublin the least affected, but still down close on 31% from the peak in early 2007. Outside Dublin, one could pick any county and see a similar result, with prices in Cork and Galway down around a third in the final quarter from where they were at the height of the boom. Limerick posted the best result, though here again prices in the fourth quarter of 2009 were still almost 21.5% off peak.

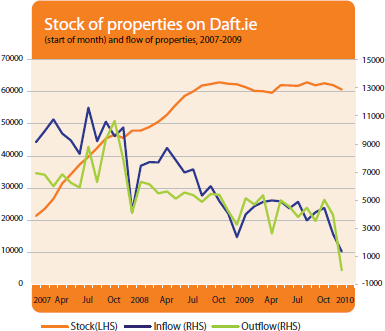

That said, there are some seeds of comfort from the Daft report, with the average time to sell a property falling from the previous quarter. The typical Dublin property is now taking about four months to sell, compared to seven months elsewhere in Leinster and more than nine months in other parts of the country. Meanwhile, the stock of properties for sale in the country remains above 60,000 units, but in Dublin that represents a decline of 17% in the year. The overall message in the report is that while house prices continue to adjust downward, there appears to be an easing off in the rate of decrease.

The collapse in property prices has seen many households falling into negative equity and with thousands losing their jobs, the numbers in mortgage arrears has increased dramatically. And the brutal impact of the recession on families is evident from the fact that almost 1,000 repossession orders were initiated in the High Court in 2009, up close on a third on the 2008 total of 758. In the current circumstances it is hard to be optimistic on the prospects for the property market in the immediate future. Indeed, it is difficult to see the property market improving dramatically until labour market conditions get better and consumers become more confident about their job prospects going forward. And even then, consumers will be relying on the banks to make credit more freely available than what they are doing at the moment.

Although houses have in general terms become more affordable in terms of price, this is of little comfort to potential purchasers if credit is still very tight. As such, it is therefore imperative that the country's banking system is put back on a sound footing as soon as possible. This must be the Government's main objective of 2010, because businesses/enterprises cannot hope to create jobs if money is not freely flowing around the economy, and unless underlying labour market conditions improve then the property market will continue to stagnate.

The Irish economy has faced extremely difficult conditions over the past couple of years, though recent indicators suggest that the worst of the downturn is over. But how soon the country returns to sustainable economic growth is open to debate. Still, with signs that economic conditions are improving globally, there are reasons to be optimistic, especially as a small open economy, Ireland is highly dependent on its export sector to boost its national wealth. Indeed, one thing is for sure and that is the export sector will be the key driver of the economy over the next couple of years, and for exports to boom, significant price adjustments will have to be made. There was major progress on this front in 2009, but more will need to be done in 2010 and that means further price falls, including those for houses, particularly in the first half of the year.

My own view on the economy is that we will see positive year-on-year growth in the second half of 2010, and that may result in a slight increase in house prices towards the latter part of the year. However, in overall terms, I would expect house prices to drop another 10-15% on average this year, with Dublin again seeing the biggest decline. But as prices start to recover, Dublin should see larger gains than elsewhere, though the major cities should quickly follow the upward trend of the capital. Looking further ahead, I expect house prices to be higher on average in 2011 than in 2010, and should rise on a five-year view as the labour market returns to normal.

That said, the level of any increase in house prices over the next few years is likely to be only in single digits, with three factors - the banks' adoption of a more cautious stance to lending than in the 'Celtic Tiger' era, the return of interest rates to 'normal' and the possible introduction of a property tax for 'principal' homes of residence - all weighing negatively on the market.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Properties

SNAPSHOT:

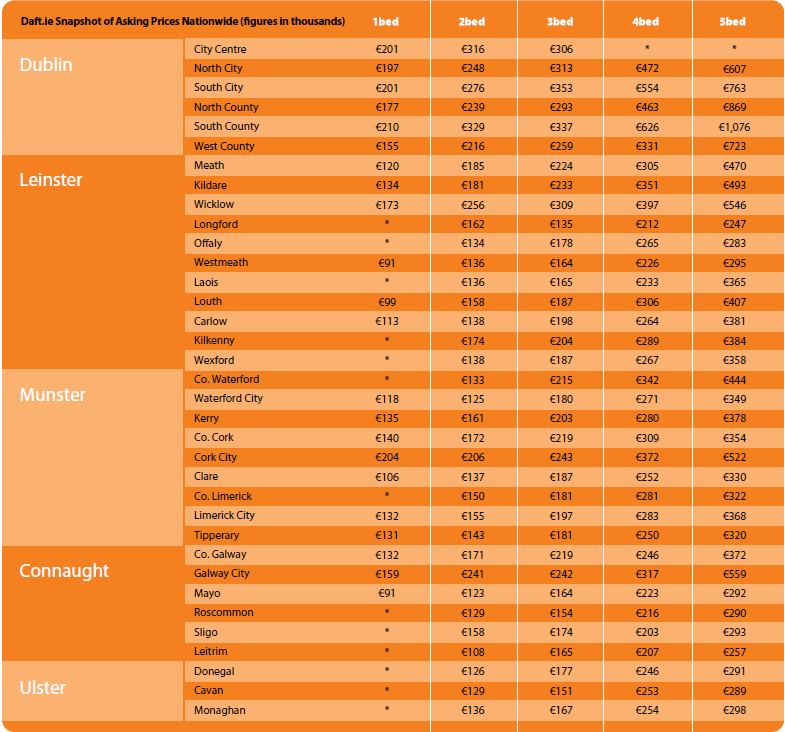

Snapshot of Asking Prices in Q4, 2009