Housing market expectations are starting to heat up

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

1st Apr 2014

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Housing market expectations are starting to heat up

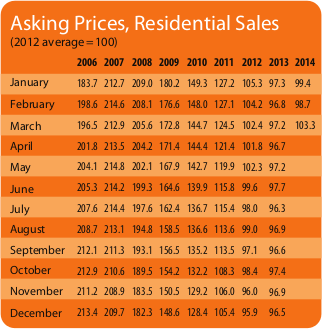

Dublin still dominates developments in the housing market. This latest Daft.ie House Price Report shows that annual inflation in Dublin list prices rose to 15% in early 2014, compared to a rise of just 0.5% 12 months previously. The rate of inflation is also accelerating - the average list price in the capital rose by 5.7% in the first three months of 2014, equivalent to the entire increase between July and December last year.

But it would be wrong to assume that house prices are still in decline throughout the rest of the country. While the year-on-year change outside Dublin remains negative, at -3.3%, this 12-month figure hides an increase between January and March of 2.3%. This quarter-on-quarter rise in list prices is the first one since mid-2007, ending a run of 26 straight quarters of falling values outside the capital.

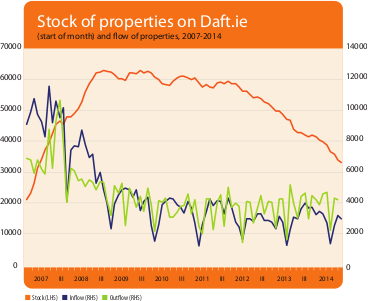

The end of price falls around the country is unsurprising when taken together with the figures on supply. The total stock of properties sitting on the market fell from 54,000 in March 2012 to 43,000 in March 2013 and to 33,000 in March 2014. To put the last two years into perspective, between early 2008 and early 2012, that figure had been stuck persistently above 50,000.

What makes the last twelve months different to the year to March 2013 is which parts of the country are contributing to the fall in stock. Munster, Connacht & Ulster (outside the cities) made up just over 40% of the fall in stock in the year to March 2013. In contrast, these three provinces have made up almost 60% of the fall in most recent twelve months.

This does not, however, mean that conditions in Dublin are easing. Quite the opposite, as it happens. There are currently fewer than 2,300 properties listed in the capital, the lowest since June 2006. Currently, less than 800 Dublin houses are coming on the market each month on average or 10,000 homes over the course of a year. In a city of roughly half a million households, this translates to just 2% for sale - a healthy market would see at least three times this amount coming on to the market each year and perhaps as much as six times.

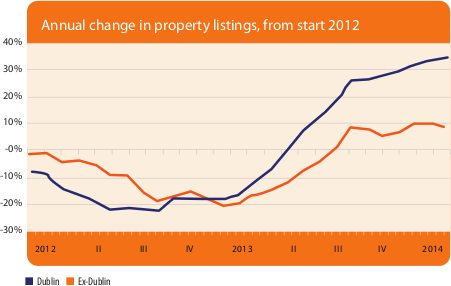

Unsurprisingly, the market in the capital is incredibly tight, with roughly 1,000 transactions a month in the second half of 2013 - well above new supply. One glimmer of hope for hard-pressed first-time buyers is the increase in fresh, mostly second-hand, supply that has emerged particularly in Dublin in the last nine months. The figure shows the annual change in property listings, for Dublin and for the rest of the country, from the start of 2012.

The total number of properties listed in Dublin rose from 6,900 in the year to March 2013 to 9,200 during the most recent 12 months. Hopefully a positive side-effect of rapidly rising prices will be to bring extra second-hand supply on to the market. As mentioned above, the Dublin market may need as many as 30,000 listings a year to meet the various sources of demand - first-time buyers, trader-uppers and trader-downers.

There does appear to be one side-effect already evident from the rapidly rising prices in Dublin. Starting in this report, a quarterly survey of housing market expectations will be included along with the other market metrics. The survey for this report, carried out in March 2014 with over 1,000 respondents, shows that expectations about future house price movements - which are key in driving demand - have become more optimistic in recent months.

In late 2012, the typical Dublin respondent expected prices to fall 4% over the coming 12 months. By late 2013, that had changed to an increase of 4% and by March the expected increase in house prices over the coming year had risen to 6%. Elsewhere, expectations have nudged upwards, from a fall of 1% in late 2013 to an expected rise of 1% in March 2014.

While one-year expectations influence the decision to buy now or wait, five-year expectations are probably a better reflection of how realistic - or indeed worried - those active in the housing market are. Currently, those in Dublin expect prices to be about 20% higher in five years than now, while those elsewhere expect a rise of 10%. The Dublin figure in particular is at the bounds of healthy increases - if the expected price increase rises even further over coming quarters, those who have been crying "bubble" since prices turned in the capital may have justification.

Ultimately, expectations may be the spark but credit is the fuel. Currently, the survey indicates that people are looking to buy a house worth about four times their income (4.5 in Dublin). This is in line with prudential lending. But currently, no regulation exists in relation to lending standards. An obvious step for the Financial Regulator would be to introduce a minimum deposit (i.e. a maximum loan-to-value). Experiences from other countries suggest that this simple tool can work wonders in stemming demand that is fuelled by expectations about prices rising in the future.

With more than half of all respondents worried about a lack of properties available, however, the supply of houses should be as much a concern for policymakers as the supply of credit.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Sale Properties

SNAPSHOT:

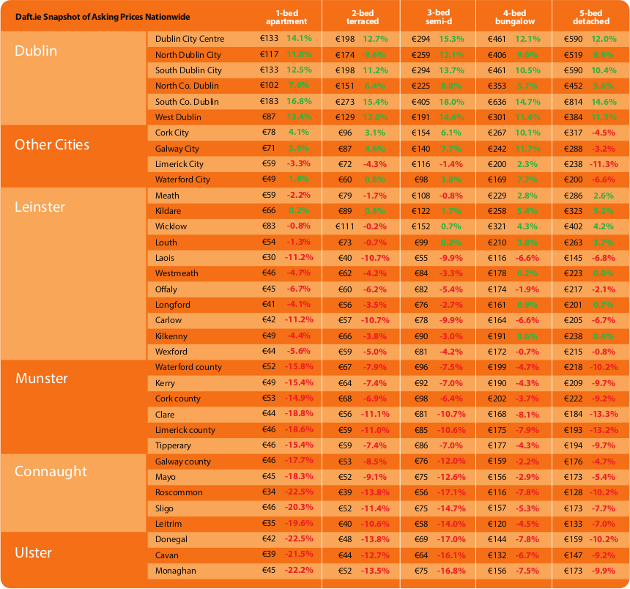

Snapshot of Asking Prices Nationwide