The rental market is changing, and changing rapidly

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

7th Nov 2012

Lorcan Sirr is a lecturer in housing at Dublin Institute of Technology. He is a renter, has been a home-owner, and until recently was also a landlord.

The rental market is changing, and changing rapidly

The Daft.ie Report has always been an interesting publication, providing a raft of rent-related information and giving a snapshot of life in the rental market. But who, and what, was this rental market?

With a small degree of artistic licence, I would say that it frequently comprised landlords with a couple of flats that they, often reluctantly, dealt with after their day jobs, if at all; more were landlords who had inherited their properties and really didn't have the knowledge, interest or resources to manage them properly (the 'accidental landlords'); even more were developers hanging on to their units until capital values improved; and finally, there's occasional landlord who took an active part in managing their property and tenants.

And on the tenant side? The rental sector has long had a maligned reputation as a refuge for unruly students, separated fathers, the unemployed, the poor, recent immigrants, and the socially marginalised. Government policy has always been so heavily weighted towards home ownership that there had to be something wrong if you couldn't or didn't own your own home.

The properties themselves reflected this tenant stereotype, with many being on the marginal side of habitable. And here I withdraw my artistic licence, for as a renter myself, I have seen what the rental market frequently offers - quite recently - and what landlords thought was acceptable to ask rent for: damp, draughty, cold, unhealthy units often not meeting basic human needs with barred windows and furniture that a dump would reject. The landlords wouldn't have stayed in their own rental units, but it was alright for someone else.

The average Irish landlord has between 1.6 and 2.1 properties, depending on which figures (below) are used, and less than 1.25% has ten or more properties, reflecting an undeveloped and amateur market. The amateur nature of the rental market is highlighted in the 31.72% discrepancy in the number of tenancies registered with the Private Rented Tenancies Board in December 2010 (231,828) and the number of tenancies recorded by the state Census just four months later (305,377). This is symptomatic of a fear of regulation - a typical amateur notion - rather than recognition that regulation would actually strengthen the market, and indeed, rents.

The legislation governing the landlord and tenant relationship also reflects this amateurism. No doubt influenced by demands at the time, the Residential Tenancies Act 2004 is now self-defeating in its function. It is heavily biased towards supporting the landlord and as such affords landlords a range of, in my opinion, spurious reasons whereby they can recover possession of their property.

The Act therefore perpetuates the amateur nature of the market by actively deterring those who would want to rent for the long term.

But the rental market is changing, and changing rapidly, and both the Act and landlords are going to have to adapt if they want to capture what the market has to offer.

The numbers of individuals and families renting has rocketed in the last five years. Across Ireland, about 29% of all people now rent, with 18.5% renting from the private sector. This is roughly the same level as in the mid-1950s. But what is more interesting is the speed of change: numbers renting in the private sector have increased 86% (up from 9.9%) since 2006.

Not alone that, but those renting have also changed, as is reflected in the rental increases for specific types of properties. Family homes are now in big demand as often previous owners feel reluctant to risk their savings again on the gamble that is property ownership.

Then there are the 'DOODs' - the Don't Own Or Drive cohort - who are well-educated, well-travelled, demanding, employed people who would rather trade a car-parking space and ownership for proximity to services and a decent location to live in. They could get a mortgage if they wanted to, but it's not really for them.

These groups are the antithesis of those who have traditionally rented in the private sector. And no, not all these renters are hanging on until the market 'recovers'. The recent SCSI/Red C survey shows that 61% of renters would be happy to rent long term, suitable property and terms being available.

Rents in solid established suburban locations are increasing, meaning that although the type of renter may be changing, where they want to live is not. Rents are up in Dublin in general and Galway city, and falls in rent are easing elsewhere. Rental stock is falling everywhere.

All this means there is a new market out there ready to be satisfied. It also means that to capitalise on this market several things have to change.

1) Broadly, landlords have to professionalise and increase the standard of accommodation on offer to meet the requirements of an increasingly demanding tenant sector. If they don't, they will miss out on the prime tenants who are now out there seeking accommodation. It also means registering with the PRTB as required by law. It isn't an option.2) The Residential Tenancies Act has to change to better balance the needs of tenants with those of landlords. The RTA is currently the opposite of what it needs to be, and deters potential renters from the market rather than supporting them.

3) Government policy has to translate into legislation. Equity of tenure is a commendable concept, but would be better still if it had the force of law where it balances the rights of those who want to rent with those who want to own.

The Daft.ie Report started off with a relatively narrow market at its core, but that market has now grown considerably. It may come as a surprise even to itself, but Daft.ie and its figures arguably reflect the most significant cultural shift in the Irish property-psyche in the last fifty years.

Enjoy.

HIGHLIGHTS:

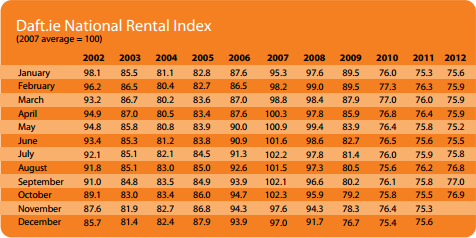

Rental Price Index

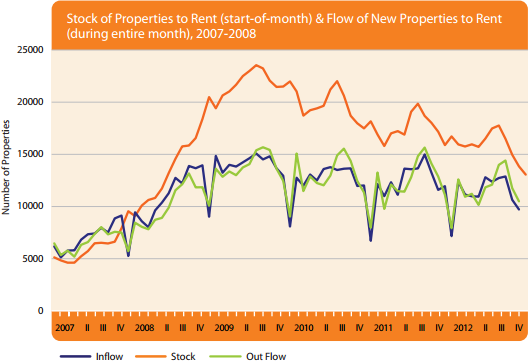

Stock and Flow of Rental Properties

SNAPSHOT:

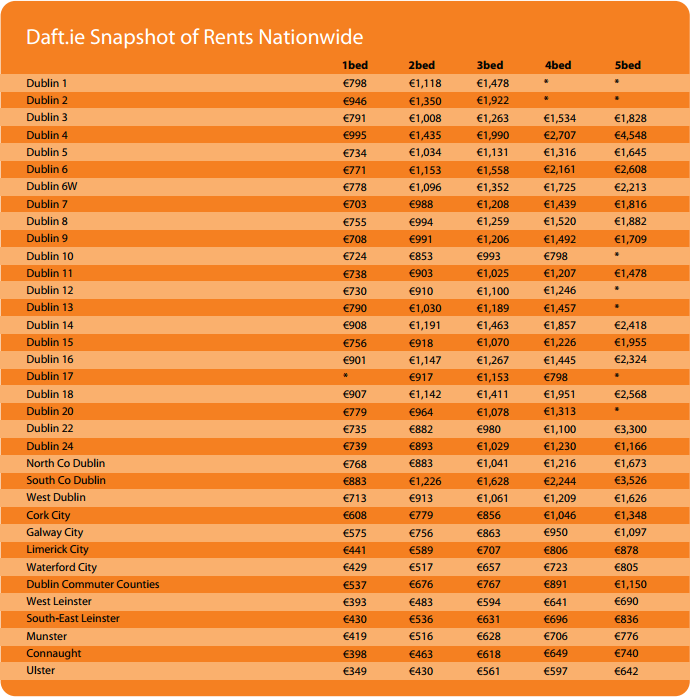

Snapshot of Rents Nationwide