Price expectations adjusting downwards, but further reality check is required to reduce stock levels

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

8th Apr 2008

Dermot O'Leary is our guest blogger, analysing the Quarter 1 2008 figures.

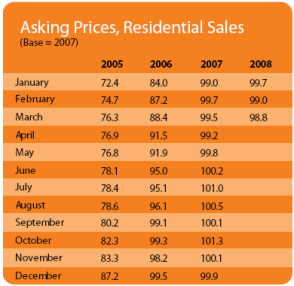

Property can be a pretty emotive subject at the best of times. Every seller has a personal view of the value of their own property. However, it is not the seller of a property that sets its value. Of course, sellers can set an expectation of the price they want to achieve, but in the end the selling price is decided by the interaction of supply and demand forces in the market. When the market is hot, as was the case in the Irish residential market in 2006 for example, sellers were quick to adjust their price expectations upward. According to the Daft.ie index, asking prices were rising at over 20% per annum in late 2006. As we know only too well, circumstances have changed dramatically since then, thus sellers are slowly realising that their price expectations will have to be taken down a notch or two in order to stimulate interest.

Difficult to escape the effects of the credit crunch

The most obvious cooling influence on the Irish housing market was the doubling of ECB interest rates from December 2005 to June 2007. More recently though, the international financial market turmoil has gotten all the attention, and it would be folly to suggest that Ireland, and the Irish housing market, will not be affected by these developments. In fact, credit standards have already started to be tightened with, for example, most lenders shying away from the 100% Loan-to-Value mortgage space, which had become very popular for first-time buyers who were finding it difficult to raise the initial funding for a deposit.

Asking prices have been slow to adjust downwards

Regardless of housing market trends, people need a place to live, so demand for housing has not just vanished. However, the price point at which this demand is triggered has been adjusted downwards. Indeed, this is reflected in the fact that house prices in the opening months of 2008 have been, on average, close to 10% below levels achieved twelve months earlier, according to ESRI figures. However, because of the emotions alluded to above, asking prices have been rather slow to adjust downwards, although there is evidence in the Daft.ie data for the first quarter of the year that vendors are starting to get the message that earlier expectations for house prices will not be achieved.

Asking prices are in fact being adjusted downwards at a faster pace more recently - while asking prices were largely static throughout much of 2007, in the first quarter of 2008, asking prices fell by 1.2% on average. We have already seen evidence that significant price cuts in some housing developments have been able to spur a rather impressive increase in demand. Vendors should take note. Taking a line from the 1969 Rolling Stones song, sellers are starting, and must continue, to realise that "you can't always get what you want" in terms of house prices.

Alan Greenspan, not so long ago, stated that there was no bubble in the US housing market. He believed at the time that there was simply a certain amount of froth in the market. The man certainly did have a way with words. Have a look at the dictionary definition for froth: "a mass of small bubbles". One of the key points that he was trying to make was that all property markets are local and are dependent on the unique conditions in place in those areas. This can certainly be the case in the US, given the vast diversity in the world's largest economy. But, can the same be said about the Irish housing market?

There are factors which will affect the whole market, the main one of which is movements in interest rates. For this reason, it is no surprise that price declines have been pretty widespread across the country; of the thirty-four regions identified by Daft.ie, twenty-four saw asking prices decline in the first quarter of 2008. However, the Daft.ie data also highlight some significant differences in the regional movements in asking prices; in Tipperary, asking prices increased by 8.5% over the past year, while asking prices in Wicklow were down by 8.0% over the same time period.

High stock levels indicate it is still a buyer's market

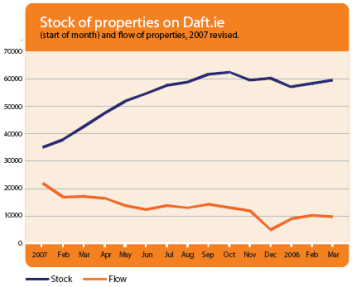

One would have to be brave to conclude that we have seen the end of house price declines. The headwinds in store for the Irish economy, including rising unemployment rates, tighter credit conditions and an international slowdown, have certainly got stronger since the turn of the year. Along with lower confidence levels, these factors do not suggest that there will be a near-term scramble to buy a home. On the supply side, the sharp reduction in the number of new houses commenced is undoubtedly a positive for house prices, but we must also take account of the stock of homes for sale on the market.

According to the Daft.ie data, the stock of homes for sale on the website has begun to stabilise over the past few months. However, closer analysis reveals that stock levels in Q1 were still 51% ahead of last year's levels. The stabilisation has been mainly due to the fact that the number of homes being put on the market has fallen quite significantly, by 48% year-on-year in Q1 in fact. This may be due to a number of reasons, including a realisation by the sellers that the market has reached a saturation point or that sellers are unlikely to achieve their desired selling price in the current market. To clear this stock, asking prices may have to be adjusted further downwards, and vendors should not let their emotions get in the way, as recent evidence suggests buyers are willing to move at the right price.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Properties

SNAPSHOT:

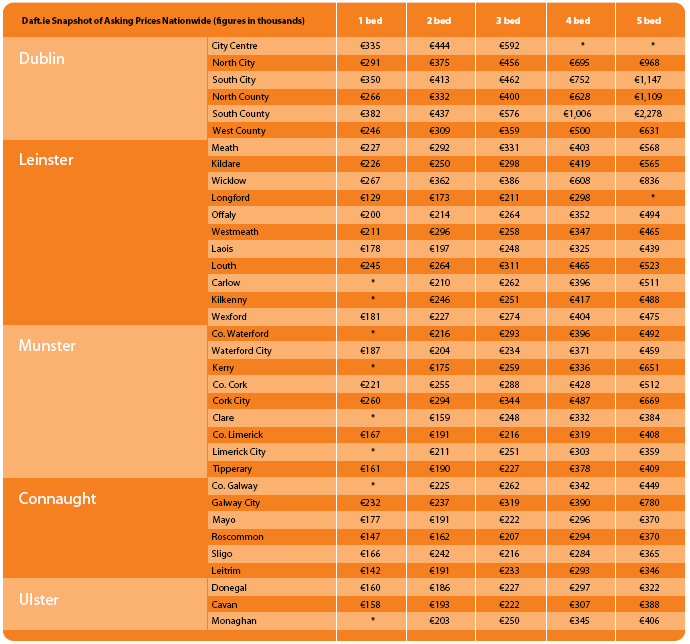

Average Asking Prices across Ireland in Q1 2008