2013: After six years, time to build again?

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

2nd Jan 2013

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

2013: After six years, time to build again?

Ireland is emerging from one of the worst property market downturns in the post-war developed world. Economists typically focus on what are termed "real house prices", i.e. comparing house prices with prices elsewhere in the economy. Studies show that severe housing busts are typically long and brought about in large part by higher prices elsewhere in the economy, and perhaps also a weakening currency.

In contrast, however, Ireland's housing bust has been remarkably rapid and has occurred entirely without inflation elsewhere in the economy. And, by necessity, there has been no devaluation of the currency used in Ireland - which is now continental, not national. In this sense, the Irish crash looks more like a US city or state - such as Detroit or Nevada - than other national housing crashes.

End of the downturn?

How can we say that Ireland is actually emerging from the downturn? In one sense, we can't. In large parts of the country, particularly in Munster, Connacht and Ulster outside the cities, there are still the same symptoms as we enter 2013 - rapidly falling prices (up to 20% in the last year, in some places), a large overhang of houses on the market and only a small proportion of properties selling in four months, a reasonable time in a healthy market, for any property to find a buyer.

Nonetheless, in Dublin in particular, but also in its hinterland and in the other cities, there are a growing number of indications - many of them contained in this report - that the market in late 2012 is by far the closest to stable in a long time.

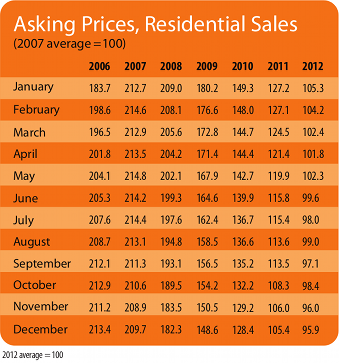

For example, this time last year, asking prices in South County Dublin were falling at an annual rate of 22%. In the final quarter of 2012, they were actually 3% higher than a year previously. In Dublin city centre, prices fell by 25% during 2011 - but rose marginally over the course of 2012. In contrast, asking prices are still falling rapidly in Munster, Connacht and Ulster. Indeed, for the first time since prices started to fall, the fall from the peak is greater in Connacht-Ulster (55.9%) than in Dublin (55.4%).

There are some who doubt the relevance of asking prices. And yet, these encouraging signals from asking prices are repeated across a range of other indicators. For example, this is the first Daft.ie Report which also includes an analysis of transactions prices, based on the new Residential Property Price Register.

A major limitation of the Price Register is the lack of information on the property sold, for example type or size. For roughly 5,000 transactions in 2012, it has been possible to match back to the original listing on Daft.ie. This enables the like-for-like analysis required to say definitively whether and how fast prices are rising or falling. And the picture is remarkably similar to what is emerging from asking prices. For example, in South County Dublin, the annual fall in prices went from 20% a year ago to just 1% now.

Supply-side issues

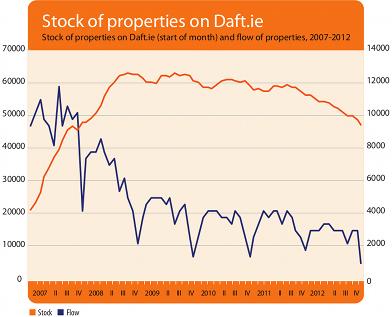

Ultimately, prices are the symptom - the outcome of the market process - rather than the cause. To see what will happen next, we must look to what is happening underlying supply and demand. In relation to supply, the total number of properties on the market nationwide is at its lowest in five years.

This is being driven by Dublin, where there are fewer properties for sale than at any point since February 2007. The number of properties sitting on the market has fallen by 50% in the last couple of years. There is now no backlog of Celtic Tiger housing in the capital. Even in Munster and Connacht-Ulster, stock for sale is back at mid-2008 levels, although this represents a fall of 20%, rather than 50%, in the numbers sitting on the market.

Similarly, the Dublin market is showing very healthy figures for the time taken to sell a property. Nationwide, it is now the case that 4 in 10 properties are selling within 4 months, compared to 3 in 10 a year ago. Once again, this improvement is being driven by Dublin, where almost two thirds of properties sell within 4 months currently. There has also been an improvement in time-to-sell in the other cities and in Leinster. In Munster and Connacht-Ulster (excluding the cities), there has been very little improvement in conditions.

Looking to 2013

Looking ahead to 2013, it is clear that the end of mortgage interest relief may have an adverse impact on the market in the first half of the year. Effectively, some of the demand from 2013 was stolen and crammed into 2012 instead. Nonetheless, levelling the playing field between buying and renting long-term is an important step in creating a healthy property market. As is an annual property tax, which is effectively replacing Celtic Tiger-era stamp duty.

Nonetheless, all the indications are that a balance has been reached in Dublin - and possibly in the other cities - between supply and demand. With the pull of the cities stronger in the crash, the Government needs to start planning now for building the new homes the cities will need over the coming decade. This may sound odd, as property oversupply still blights much of the country, but the mistakes of the past should not mean avoiding making more mistakes in the future.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Sale Properties

SNAPSHOT:

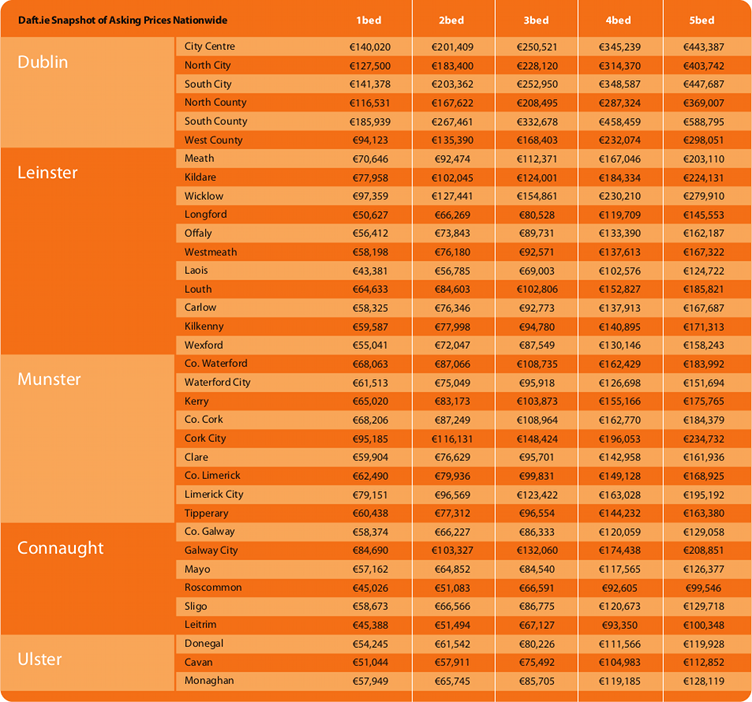

Snapshot of Asking Prices Nationwide