Top end of the market hit the hardest as rents continue to fall

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

17th Aug 2009

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

This latest Daft Report shows that rents are falling at double-digit rates around the country. This fact will no doubt be good news not only for new and returning students, but for all tenants around the country. As students start their hunt for accommodation this week, the typical student renting a double-room in Dublin city centre can expect to save about €1,000 over the course of the coming academic year, compared to last year. This is about the same amount that two students renting a two-bedroom property in Galway or Limerick might expect to save.

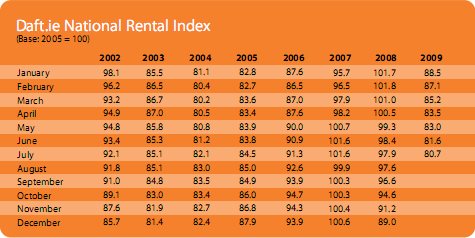

Urban areas hit hardestRents have now been falling month on month for almost a year and a half. In early 2008, the average rent in Dublin was over €1,300. By July 2009, that had fallen to just over €1,000. Cork has seen a similar 20% fall, with the average rent in the city now below €850. Around the country as a whole, rents are typically between 15% and 20% below their peak

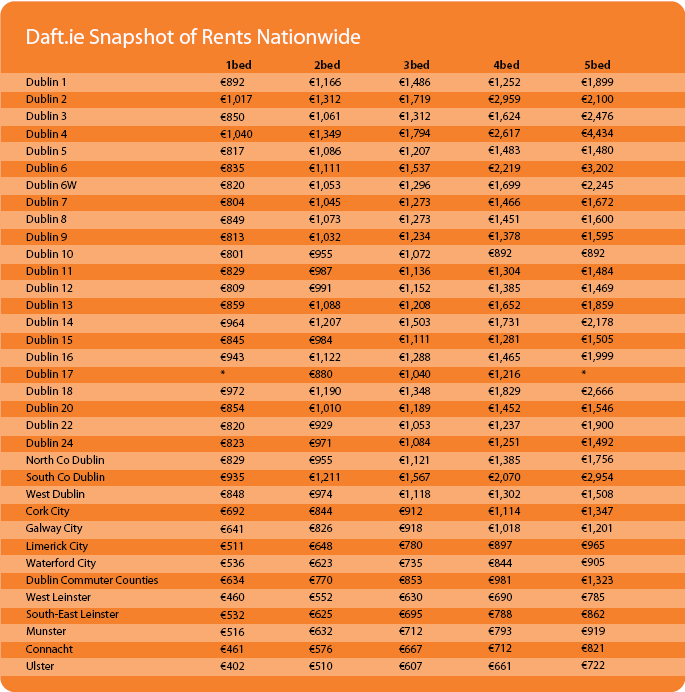

The regional spread of falls is interesting, though. It is urban areas, Ireland's larger rental markets, that are seeing the biggest falls in rents, in both euro and percentage terms. In South County Dublin, rents are on average 23% below their peak, whereas in Connacht, the fall has been 14%. In certain parts of the country, for example Kerry and Donegal, the fall has been closer to 10%.

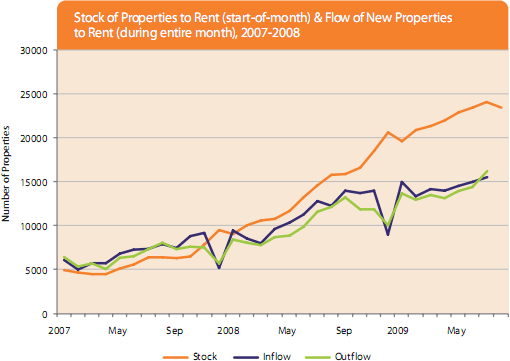

The supply-side puzzleThe primary reason rents are falling is due to increased supply. Basic economics tells us if there is competition among tenants, rents will rise and if there is competition among landlords, rents will fall. The total number of properties available to rent at any one time on daft.ie has risen steadily over the last two years, suggesting much more competition among landlords. On August 1st 2007, there were 6,200 properties available to rent nationwide. On August 1st 2009, there were 23,400 properties to rent, almost four times as many.

On the face of it, then, the explanation is easy. The increase in supply has far exceeded any increase in demand from would-be first-time buyers staying in rented accommodation while house prices fall. But while the overall point is certainly true, the fner details suggest a more complicated story. Why is it that South County Dublin, where there has been a 160% increase in properties to rent, has seen a fall in rents almost twice as large as Munster and Connacht, where there has been a fve-fold increase in properties available to rent?

Confidence versus afordabilityThe answer may lie in the diference between short-run and long-run pressures on the property market, when it is in a bust. To see why, one can look at the sales market. As last month's House Price Report showed, the average asking price in South County Dublin, which peaked at €680,000, has fallen over 30%. By comparison, asking prices in South-East Leinster have fallen just 18%. It is easy to think why prices at the top end of the market have fallen more than prices in cheaper areas: while the boom fuelled house prices everywhere, the very top end of the market saw the biggest excesses.

In economic terms, the lower the house price bracket, the more prices are driven by afordability, i.e. determined by fundamental criteria such as average wages and interest rates. The higher the price bracket, the more prices are driven by confidence, i.e. determined by 'future expected value', what the buyer thinks the property will be worth when it is sold again.

Confidence swings much faster than afordability, so as boom has turned to bust over the last two years, those houses whose prices are determined by confidence to a greater degree have taken the bigger hits. We can see the same pattern emerging in the rental market. The Daft Report analyses 16 regional markets around the country. On average, the higher a regional market's peak rent, the larger its percentage fall has been so far.

The short term versus the medium termWhat remains to be seen, though, is what the dynamic in the market will be beyond the short term. The end of falling rents may be near. On August 1, for the first time in over two years, apart from the usual end-of-year market clearing in December, there were fewer properties available to rent than a month previously. If that blip become a trend that continues for the next year, and if Ireland's output and unemployment pictures look to have turned a corner by early 2010, rents may stabilise, particularly in Ireland's more expensive markets, where sentiment is paramount.

The great unknown in all of this is the extent and future impact of overconstruction during the boom years. In an economy that needs perhaps 40,000 new properties a year, an average of 80,000 were built in recent years. This means that there is potentially a factor for downward pressure in house prices and rents even when sentiment has turned the corner. It is worth noting that more new homes were built in Connacht and Ulster between 2002 and 2008 than were built in Dublin in the same period, even though Dublin has twice the population. This suggests that the impact of overconstruction on rents and house prices is likely to be diferent in diferent parts of the country.

But for the moment, the news is all good, at least for students and their fellow tenants.

HIGHLIGHTS:

Rental Index

Stock and Flow of Rental Properties

SNAPSHOT:

Snapshot of Rents Nationwide