Stabilising rents point to importance of real economy

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

22nd Nov 2010

John Fitzgerald, Professor at the ESRI, commenting on the latest Daft research on the Irish property market.

Amid all the uncertainty and excitement concerning bail-outs and banks it can be easy to lose sight of what is important to long-term growth prospects - the performance of the real economy. One important aspect of this is the housing market. While the dangers of a housing bust were well flagged, its full consequences, especially in terms of the financial system, have proved even more serious than anticipated. For the housing market itself we have seen a collapse in prices since 2007 and, as a result, a collapse in building. Unthinkable though it may be under current circumstances, eventually new building will become profitable producing an inevitable supply response. At some point in the future things will change - we will eventually run out of vacant dwellings in desirable locations and prices will begin to rise.

It is far too early to predict when the market will turn. All the uncertainty about the macro-economy will continue to have serious consequences for household confidence for some time to come. Households, even if they were not scared before, must be scared today. Even with secure jobs and reasonable after tax incomes it will be some time before many people are prepared to contemplate a major investment, such as buying a house. House prices, though falling much more slowly still have some way to go. This is also suggested by the current yield on rental properties in Dublin, which is below what might be considered its "equilibrium level". However, the real economy continues to develop and the backdrop against which the housing market should be viewed is also changing.

One of the early and more surprising developments arising from the fall in house prices was an increase in the number of households in 2008/9. Over the period 1995 to 2005 the proportion of people aged 25 and over in Ireland who lived in independent households - had their own pad - did not rise significantly. On the face of this it was surprising given the huge increase in incomes. However, the very high cost of accommodation to rent or to purchase meant that Irish people shared an apartment or house or lived at their parental home longer than was common elsewhere in Europe (a similar pattern was apparent in Spain). With the fall in rents in 2008/9 this pattern changed and those who could afford the new lower prices (having jobs) took advantage of the more favourable market. This change in behaviour shows that people are sensitive to prices and rents.

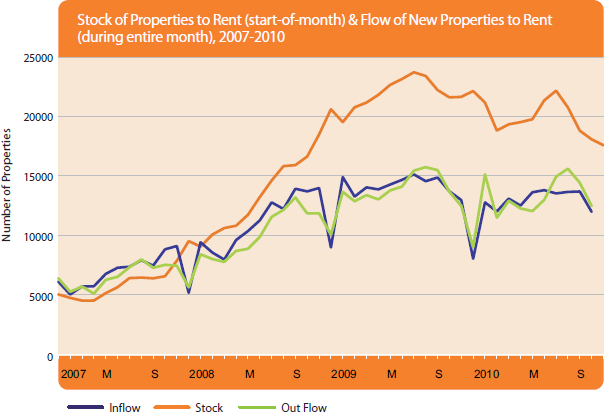

In Dublin and Cork an important factor has been the desire by those who financed much of the recent build, banks (and NAMA), to see some income coming in even if they could not be sold. (It is important to remember that NAMA, just like an old fashioned bank, wants to make money - it is unlikely to adopt policies that would destabilise the market.) Hence the supply of rental accommodation increased and prices fell. In turn, as discussed above, more people entered the market, renting where before they might have bought. The result has probably been a reduction in vacant dwellings in the greater Dublin area. The recent Department of the Environment study shows the relative stock of vacant dwellings to be lower in Dublin than in much of the rest of the country.

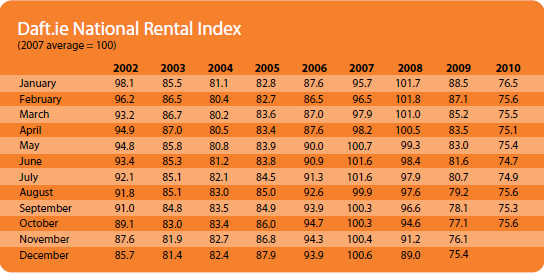

What the DAFT rental index shows is quite interesting. Having seen very substantial falls in 2008 and 2009 it would now appear that rents in Dublin have stabilised. This is apparent from the data for the last few months. It is clear from this that the supply of properties to rent is equal to the flow of new households being formed - the market is in a temporary equilibrium. This is happening in spite of the very significant outflow of people through emigration. This situation could persist for some time with stable rents. However, at some point, with the supply of properties fixed, new household formation through new renters could begin to put pressure on the market. This may not seem likely now with major fiscal retrenchment in prospect and, hence, low growth likely in 2011. However, the recovery in the tradable sector of the economy, which is clearly under way, will eventually begin to drag the rest of the economy back to growth. Then, with employment rising, incomes stabilising and prospects becoming brighter, more people will seek rental accommodation. In turn, as the excess supply dwindles rents will begin to rise. Initially such a small rise in rents will not have much impact. However, when it becomes well established it will have a number of effects. It will cause some of those renting to assess whether, in the face of rising rents, house purchase might be attractive. Eventually, as returns for those owning rented property rise and when there is some limited bounce back in house prices, there will be a gradual perception that Ireland will need some more dwellings in high demand locations.

All of this is some way off today. Much will depend on the vigour of the recovery in the tradable sector. In July when we envisaged a fiscal adjustment of €7.5 billion over the period 2011-14 I felt that such a turnaround could occur in 2012 or possibly 2013. With the doubling of the fiscal adjustment, and its consequential effects in depressing domestic demand, this could be postponed till 2013-14.

The first sign that things are beginning to turn will be a move towards rising rents. This will predate any recovery in house prices and any new building. As of today it is clear that rents have stabilised. From now on I will be watching the DAFT index seeking signs that rents are beginning to rise. I don't expect to see much action over the coming year but time will tell.

HIGHLIGHTS:

Rental Index

Stock and Flow of Properties

SNAPSHOT:

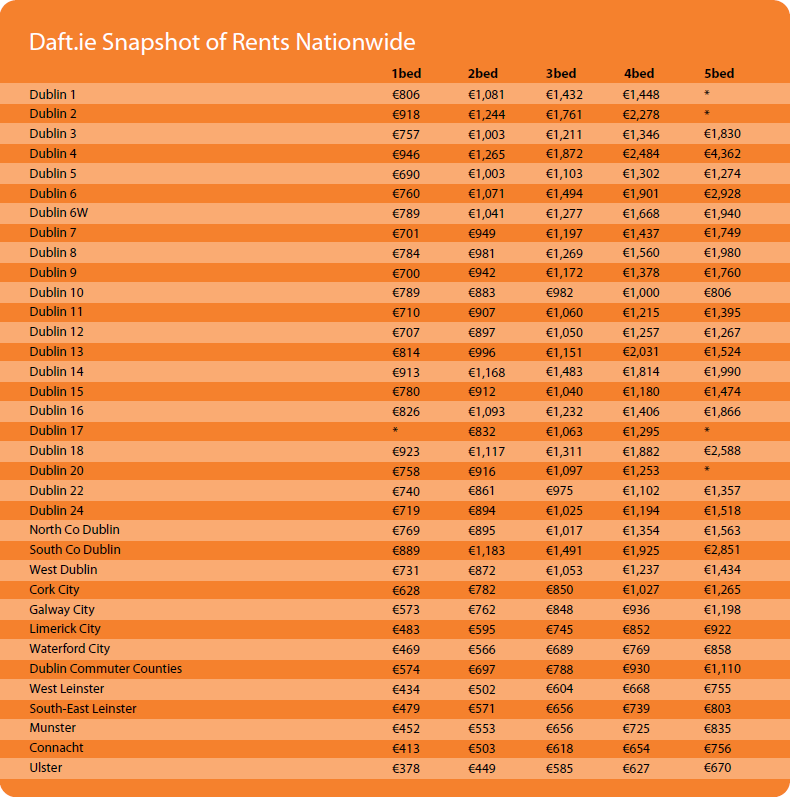

Asking Prices in Q3, 2010