Investment Key to Rental Sector Revival

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

16th Feb 2010

Michael Taft, Political & Economic Researcher, UNITE, commenting on the latest Daft research on the Irish property market.

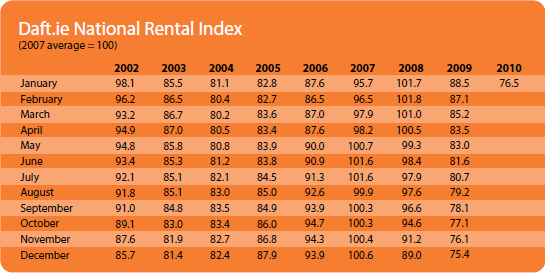

The 2009 rental market provides further evidence of an unbalanced, boom-and-bust property market on the slide. National asking-rents fell by 15 percent, consistent with falls in industrial, commercial and retail rents. End of 2009 rents were 12 percent below end of 2002 levels. Stock over-hang, negative equity, plummeting investment - you couldn't write a worse script.

Though numerous commentators are talking up the prospect of 'turning the corner', we may be entering a period of what the IMF has described as a 'statistical recovery but a human recession', something the Government's deflationary policies are clearly engendering. Their fiscally irrelevant cuts in public sector wages and social welfare rates (despite claims, such cuts will have little impact on the Exchequer's deficit) presage a general drive to depress income and growth. January redundancy notifications exceeded the 2009 monthly average. Consumer spending could come under pressure from anticipated ECB interest rate hikes later this year (the domestic banks will beat them to it). Some may be turning the corner; the rest of us are walking a different street.

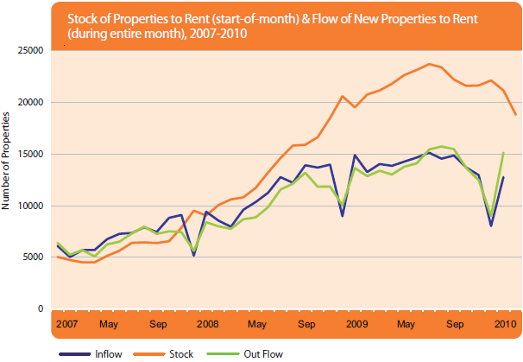

Falling rents may be welcomed by tenants but this may come at the price of reduced investment and more stock withdrawal (in the last six months of 2009, 20 percent was withdrawn - a result of over-concentration from the buy-to-let and tax-shield sectors). Rising rents - and January 2010 saw a slight increase, focused mostly on inner city Dublin - will be welcomed by landlords and their creditors but hardly by tenants, and certainly not by the enterprise sector which will suffer from displaced spending and upward wage pressures. The interaction of falling incomes, rising interest rates, higher unemployment and emigration could break in any number of directions for the rental market - most of them not good.

We need a ready supply of quality units at affordable rents which nonetheless provide a solid return to maintain investment (yields in 2009 were marginally above 2006 levels but this may come under pressure by next year without rent hikes). We need this to assist labour mobility and provide sustainable land-use. This is all the more the case when dealing with a commodity that is a social need, a special kind of good, and not just another item of consumption or capital.

To analyse the rental market using traditional instruments of supply, demand and return-on-investment can only take us so far. A significant section of the market is being kept afloat by massive public subsidy through rent supplement, the Rental Accommodation Scheme and the prospective social leasing arrangements. The escalating proportion of rent-subsidised tenants (estimated to be between a third and half of all tenancies) is such that traditional demarcations between 'public' and 'private' are no longer illuminating. Supply, demand and ROI are increasingly determined by public policy, not alleged free-acting market agents.

Historically, the private rented sector has been ignored by Governments although recent reforms such as abolishing bedsits are a welcome step. Nonetheless, the sector remains a fragmented, under-capitalised 'cottage' industry, lacking the professionalism and modern synergy with a strong regulatory culture that prevails in other EU countries. Much of this short-coming can be put down to the lack of institutional investors, insufficient regulatory over-sight, limited powers (and resources) for local government, and insufficient public capital.

We require a fundamental overhaul in the rented sector to increase investment, standards and tenant-safeguards while maintaining consistent rent levels and long-term yields. How do we get there from here? In other countries long-term stable institutional investment is attracted through special vehicles such as Real Estate Investment Trusts in the US. Here institutional funds were channelled through buy-to-let which contributed to the fragmented, boom-and-bust rental market. In other countries, rental markets provide life-long living, accommodating a range of demographics from singles, to families with children to pensioner; here, local authorities, shifting from managing housing stock in blocks and estates, are increasingly managing the leasing of a wide variety of private sector units spread out geographically and varying widely in standards; indeed, local authorities have found it difficult to find accommodation that reaches its' standard for tenants.

The public sector will be crucial to achieving such a transformation. Though tax incentives and other subsidies will be essential, large-scale institutional investment will be understandably wary at first. To kick-start this process, new municipal housing authorities or publicly-structured housing associations/cooperatives could be established. This would provide economies of scale, lower input costs per unit, raise management standards and design a market accessible and attractive to all demographics. Such vehicles could attract institutional investment, even by guaranteeing yields over the long-term. To the extent that such bodies would provide for both the public and private markets, traversing a divide that doesn't functionally exist in many sectors, this could reduce the cost to taxpayers.

This transformation would be accompanied by complete financial, rent and yield transparency. There is no reason why data regarding rents paid, yields and available stock should not be freely available to all. The private rented sector is plagued by lack of data which is why Daft provides a considerable public service.

In this new dispensation, the fortunes of the small-scale investor and provider could also flourish. Working from a new base-line of standards, rent levels and yields, the committed investor could inject flexibility into the market in terms of product differentiation, location and provision without disturbing the underlying stability.

As Dr. Nat O'Connor of TASC points out, the idea that middle to high-income people will all become owner occupiers is coming to an end. Hence, the renting demographic will broaden. In short, the future will be renting.

All the more need, then, for a quality-driven market - stable, professional, and profitable. This will no doubt require considerable upfront public investment. But the social and economic returns would be high. And such investment could be a small antidote to the Government's deflationary policies. This would help ensure that any statistical recovery is translated into a human recovery.

HIGHLIGHTS:

Rental Index

Stock and Flow of Rental Properties

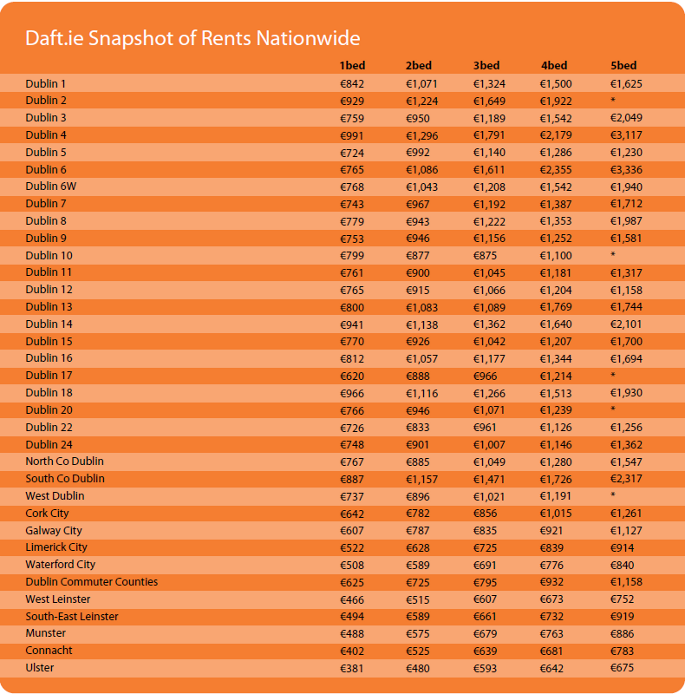

SNAPSHOT:

Snapshot of Rents Nationwide