Latest figures suggest a 75% fall in land values

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

5th Oct 2010

Patrick Koucheravy, Economist at CBRE Ireland, commenting on the latest Daft research on the Irish property market.

In 1961, the poet Robert Frost was reportedly so blinded by the glare of the sun at JFK's inauguration that instead of reading his prepared poem for the occasion, he recited from memory The Gift Outright, sixteen lines on the relationship between the people of the United States and the land they were destined to inhabit for better or worse. It begins, "The land was ours before we were the land's." While the relationship between the people and the land looms large in the national psyches of both the US and Ireland, it is still easy for us to take the land for granted. In the property market, recent discussion on the impact of the bursting of the Irish credit and property bubbles has been primarily concentrated on house prices with little reference to the knock-on impact on land values.

Reporting on changes in the Irish property market in recent years has focussed primarily on the values of buildings, both residential and commercial. But considering the establishment of NAMA - with its estimated €6 billion in loans associated with land in Tranches 1 & 2 alone and more to come - and the scale of the problems in our banking system that originate with loans on land transactions, the connection between the value of homes and the value of land has never been more relevant and important to understand.

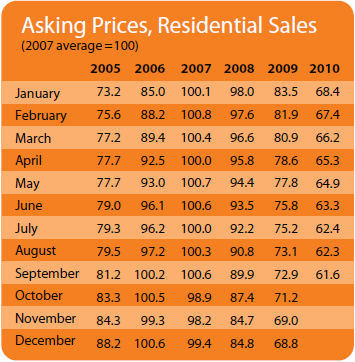

Due to a lack of large development land transactions since the onset of the recession, it is hard to pin down an overall average land value per acre in Ireland. We do know, however, that the huge drop in land values that we've seen over the past two years comes as a result of not only falling house and apartment prices but also three further factors: lower residential densities demanded in the market, an oversupply of zoned land in many local authority areas and a lack of funding for land purchases. The Daft Report has been instrumental in estimating changing trends in the former. As of September 2010, asking prices have fallen by 40% from peak according to the Daft Report, with a fall of 3% over the three months of third quarter.

As far as residential densities are concerned, as prices have fallen across the board for houses and apartments for sale, the buyers that remain in the market are looking to get more for less; more bedrooms, more space - in essence, lower densities than would have prevailed during the boom years. Additionally, developers are not willing to take the risk associated with building high-density developments; higher density means more units to sell and also requires a longer turnaround than individual homes. In 2007, a suburban town in the greater Dublin area would have seen planning for a density of upwards of 25 residential units an acre (higher density was seen as a solution to a perceived housing shortage). In the current market a density of 8 to 12 units per acre is more realistic. The lack of funding to facilitate transactions exerts further downward pressure on prices.

We can get a sense of the changes in land values by using some simple arithmetic. For example: where before a developer may have been able to expect to sell 25 units at an average of €370,000 each, a total of €9.25 million in revenue per acre, now the same developer would be able to only expect to build around 12 units per acre at an average of €195,000, total revenue of €2.34 million. Just based on these average asking prices from Daft and falling densities, we're looking at a drop in revenue per acre of 75%. Not only does this figure ignore VAT, building costs and a margin allowing for developer profit and risk, it is based on Daft asking prices and not the final sale price of the house or apartment. If buyers are still negotiating sellers down from asking prices, then the decline in land values is even more staggering. So, although house prices have fallen by 40% from peak according to the Daft Report and commercial property prices in Ireland have declined by up to 60% in the most recent cycle, the knock-on impact for land values is even more pronounced.

As previous Daft Report guest bloggers and we at CB Richard Ellis have frequently stated, a national house price database is essential at this stage. So too is a true accounting of the number of vacant residential units in the country, which we are set to receive from the Department of the Environment in the coming weeks. With this information, not only could we engage in more robust analysis of the residential property market, but we could also assess the impact that house price movements are actually having on land values.

While funding is limited for all property investments these days, there is almost no appetite for funding of land deals at the banks; the few transactions that are occurring are primarily cash deals at huge reductions from prices that might have been achieved just three years ago. Every sector of the property market is different, but it is extremely unlikely that land values will improve until we see improvements in rents and prices in other market sectors, which of course rely on the macroeconomic situation, specifically job creation and business expansion. The next cycle will be no different in that respect.

In no previous property cycle in history have we seen land values rise until it again becomes profitable to build. Rents must rise, prices must rise and only then will banks lend to land transactions, leading to a recovery in land values. Land prices followed property prices down. Land will eventually follow them up as well.

HIGHLIGHTS:

Asking Prices, Residential Sales

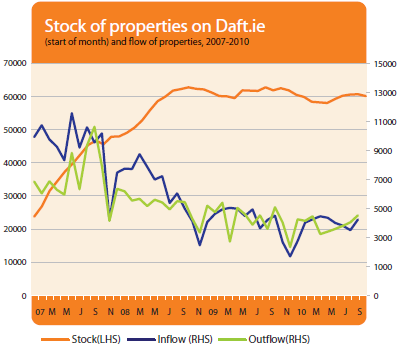

Stock and Flow of Properties

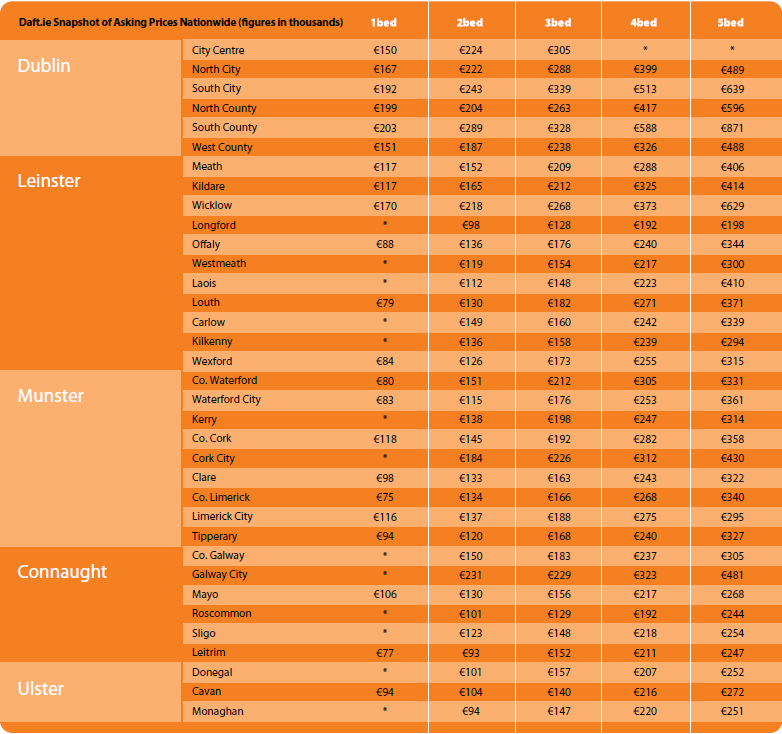

SNAPSHOT:

Asking Prices in Q3, 2010