Rent inflation a clear signal of supply constraints

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

2nd May 2013

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Rent inflation a clear signal of supply constraints

Ireland's property market continues to fragment along urban and rural lines. The most recent Daft.ie House Price report outlined how asking prices in Dublin were up year-on-year for the first time since 2007, while outside Dublin, prices were over 10% lower than a year previously. Much the same trend is evident from the rental market, outlined in this report, with rents in Dublin 5% higher than a year ago but static elsewhere. The average monthly rent in Dublin is now €77 higher than it was in late 2010 - that's almost €1,000 extra a year.

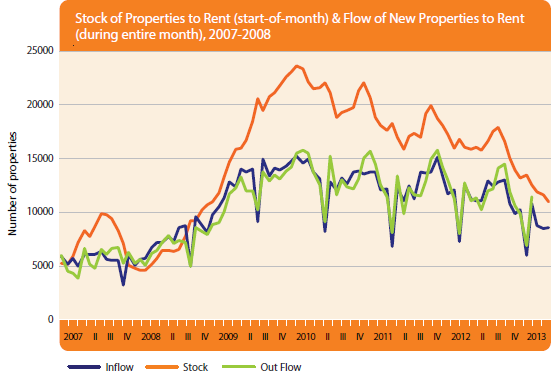

The reason for these varying trends is supply. Looking at the rental market in Dublin, there are now fewer properties available to rent than at any point since early 2007, when rents were rising at double-digit rates. Whereas this time last year, a renter in the capital would have over 4,000 units to choose from - or indeed over 7,000 to choose from in 2009 - currently, there are fewer than 2,000 homes on the market in the capital.

At the same time, there is talk of a glut of housing in Ireland. The focus of what we talk about, when we talk of Ireland's property glut, is the "ghost estate". According to the Department of the Environment, Ireland's 3,000 or so ghost estates contain 180,000 units, thus it is hard to conceive of a shortage of accommodation. But it is important to look at what is being measured with those numbers. Of the 180,000 units, roughly half are occupied, while the bulk of the remainder are only at planning permission stage.

Indeed, of the 50,000 units in ghost estates in Dublin, less than 10% are complete and vacant (700 houses and 4,000 apartments), while the same number again are partially complete. Roughly speaking then, for all Ireland's ghost estate worries, when it comes to the capital, there are at most 5,000 homes lying vacant in ghost estates, with another 5,000 units potentially able to come on to the market within the next 18 months with some work. About 90% of these units are apartments, suggesting that when they do come to the market, it will be to the rental market, rather than the sales market.

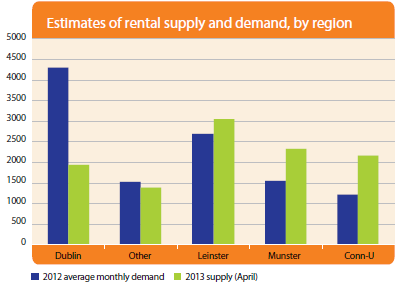

How does this compare to demand? Would 5,000 extra units both this year and next flood the rental market? The graph overleaf shows the average number of units rented out by region, during 2012. In Dublin, typically about 4,300 units were rented out each month - but only 4,200 were listed, eating away at the stock of supply. The result is that now the supply on the market in Dublin is less than half that required to meet a month's demand. In other cities, supply and demand are roughly equal, while elsewhere in the country, particularly outside Leinster, there is still more supply than demand.

After over five years of a relatively one-dimensional analysis of oversupply, it is time for policymakers to add some nuance, both by region and by type. We know from the Census that there is something in the region of 300,000 empty dwellings in the country. But we also know from the Department of the Environment that at most 35,000 of those are in ghost estates.

Therefore, Ireland's oversupply problem is overwhelmingly a problem of one-offs and one-offs are disproportionately a rural phenomenon. Between 10% and 15% of all dwellings in rural Munster, Connacht and Ulster are empty one-offs. In contrast, the same category constitutes approximately 3% of residences in Dublin.

It is sometimes argued that whereas Dublin may not be blighted with over-supply, instead of building again, we can get people to sprawl into its commuter counties. There are unfortunately two limitations to that argument. Firstly, evidence from the housing market suggests that while people were happy to commute an extra hour a day in the boom and pay the same price - as they would benefit from rising house prices - the same logic does not apply today. An extra half hour each way is associated with a 10% discount on prices, everything else being equal.

And secondly, even then, it is not clear that there are that many units available in Dublin's commuter counties. Physical geography can be deceptive - the four traditional commuter counties may be large but they contain only half the dwellings of the capital. Including one-offs, Dublin has approximately 23,000 houses that are either vacant, partially built or not-yet-started but with planning permission. All four commuter counties have only a further 24,000.

Dublin is a city where about 10,000 new households are formed every year, according to statistics on first-time births. New properties coming on the market through aging and executor sales probably total less than 4,000 a year, while the current rate of completions in the capital is about 1,000. The maths simply doesn't stack up - to avoid potentially harmful spikes in prices and rents in the capital in the near future, new supply will be needed.

HIGHLIGHTS:

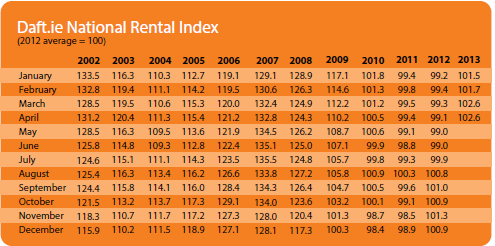

Rental Price Index

Stock and Flow of Rental Properties

SNAPSHOT:

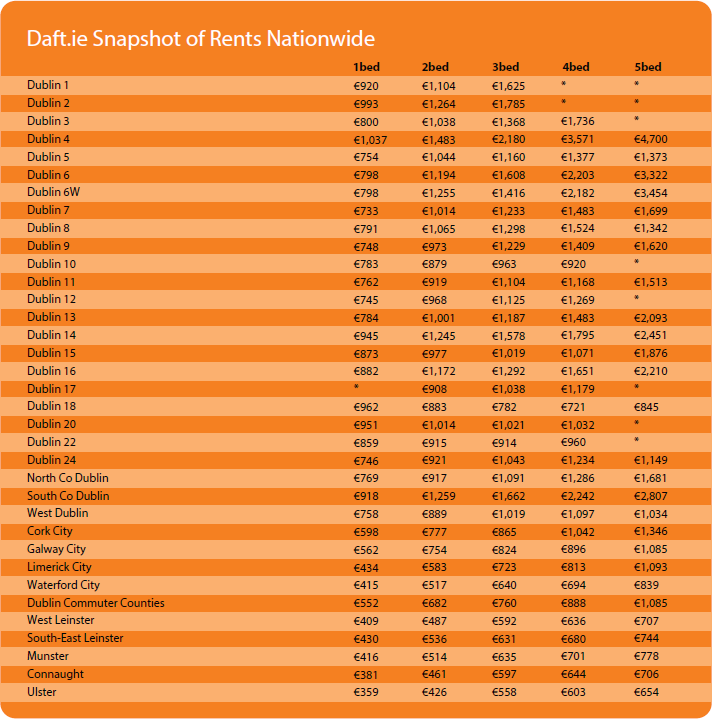

Snapshot of Rents Nationwide