Strong rental growth points to stabilising property markets

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

20th Aug 2007

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

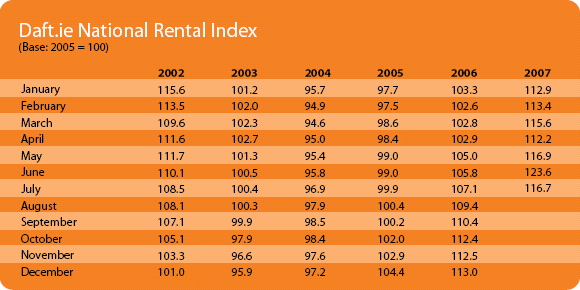

With high rates of home ownership and a booming economy, it is understandable that much of the focus in the past few years, when it came to the property market, was on house prices. The last six months have seen a shift, though, and the spotlight is well and truly on the rental sector. And while soaring house prices had been grabbing all the headlines, the rental market was also entering uncharted territory. Rents have risen in both absolute and year-on-year terms each quarter since late 2004. Recently, the pace at which rents have been rising reached record speed. As shown in the last Daft Rental report, the first quarter of 2007 saw rent increases of 10.8% compared to the same period in 2006. In the second quarter this figure increased to 12.4%

Meanwhile, all commentators agree that, when looked at in month-on-month or year-on-year terms, the house price boom is over, something fans of the Daft report have known since mid-2006, when asking price inflation started to slow dramatically. With house prices now static, all eyes are on the rental market to see what next for Ireland's property market. A healthy rental sector that absorbed a shift in supply from sales to letting would reassure people of the fundamentals and steady the nerves. A faltering rental sector, though, with rapidly rising inventories and tumbling rents, would not augur well for house prices over the next two to three years.

June rents mark new high

The average annual increase in rents in Q2 was 12.4%, more than twice the figure for the same period in 2006 (5.8%). June in particular marks a spike in rents sought by landlords where average rents where at the highest level ever since we start recording rental figures in 2001. The increase in rents during the second quarter was more or less across the board, with only two areas not showing sustained growth, Dublin's commuter towns, where rents dipped slightly, and Connacht/Ulster outside of Galway city, where they were static.

Excess of supply in Dublin's commuter towns

The fall in average rents in Dublin's commuter towns (Celbridge, Naas, Leixlip, Bray, Maynooth and Greystones) is particularly acute for one and two bedroom properties. In addition to falling rents and a glut of properties for sale in these areas, figures from the accommodation sharing market indicate that average income from letting a room fell in these towns. This indicates both an excess of supply generally in these areas and - more importantly - better value substitutes, either cheaper properties further out or properties at the same price closer to town. The fact that this is only happening in Dublin's commuter towns, and is not more widespread, more than likely says more about relative shifts in supply than an overall weakness in the market.

Rents 'hit a wall'

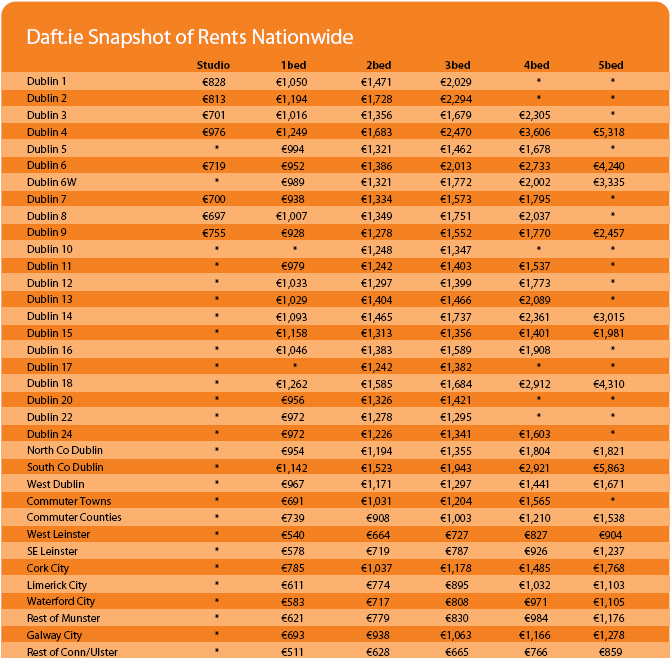

In Dublin city, while rents are still high, there are signs from the July figures that rents have fallen back in certain segments, particularly the key markets of Dublin City Centre and South Dublin County. Rents continue to rise, though, in the cheaper markets of North Dublin City - up 2.2% in July - and North Dublin County - up 1.2% in July. This indicates that in the rental market - just as can be seen in the sales market - affordability is now the key. The gap between Dublin City Centre rents and North Dublin City rents used to be consistently over €250 but in July fell below €200. Similarly, the premium enjoyed by Dublin City Centre over other areas, including South Dublin City, fell in July, suggesting that rents in the capital may have 'hit a wall' in terms of affordability: if asked to pay above a certain amount to live in the city centre, people would rather move slightly further out and pay less.

Affordability still key

As noted above, Dublin's commuter towns have been affected in all three property markets - sales, lettings and accommodation sharing. Part of the explanation may lie in the growing popularity of West Dublin, from new developments around the M50 to new interest in established suburbs such as Mulhuddart. The average net loan burden - i.e. the monthly mortgage repayment, after deductions for interest relief and taking into account income from accommodation sharing - for a three-bedroom property in the area is just over €1,000, where a double-room is shared. This is more than €100 cheaper than North County Dublin, the next cheapest area and - significantly - is still cheaper than Dublin's commuter towns. Not surprisingly, then, West Dublin offers the greatest expected yield in the country, at just under 4%.

Overall, rental inflation looks to have peaked - and more than likely, so have rents, as the bounds of tenants' ability to pay have been reached. With interest rates back at normal levels, demand has contracted and people are looking very closely at what they can afford. On the supply side, housing completions have been at record levels and there are more secondhand properties for sale now on Daft than ever before. Therefore, there has never been greater competition among sellers for buyers' attention. Therefore, static house prices are to be expected and, given rates of inflation generally, falls in real house prices are on the cards for 2007 and possibly 2008. In the long run, though, this is perfectly normal behaviour, as the market looks to correct the yield.

With such strong rental growth for the first half it is difficult to see any problems occuring in the rental market for the forseeable future. However, should rents start to falter in 2008, a recovery in the property market may take longer than expected. Watch this space!

HIGHLIGHTS:

The Daft.ie National Rent Index

SNAPSHOT:

Average rents across Ireland in Aug 2007