Second Wave of Weakness to Come?

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

5th Apr 2011

Eoin Fahy, chief economist at Kleinwort Benson Investors, commenting on the latest Daft research on the Irish property market.

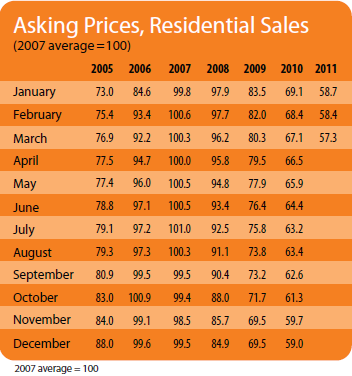

The huge decline in house prices over the last five years or so was caused in large part by the recession, which led to hundreds of thousands of people losing their jobs, and/or emigrating from the country. At the same time, the problems in the banking industry meant that credit became very hard to get. And of course the extremely high prices seen at the peak of the market (based largely on the absurd view that Irish property prices could never fall) had to reverse, even in the absence of a credit crunch or recession. The latest Daft survey shows that the fall in prices may be beginning to slow. Residential property asking prices fell a further 3.1% in the first quarter of the year, relative to the previous quarter, bringing the total decline since the peak to 43%. That fall was the second-smallest quarterly decline since the current crisis began in 2008.

It's likely that the relative improvement, or at least slower disimprovement, is because some of the factors driving house prices down are moderating. Jobs are not being lost at anything like the pace that we saw a year or two ago. Valuations are certainly not expensive on almost any measure. And while the credit crunch will certainly not go away, it is unlikely to get much worse.

But, and it's a big "but", a new set of problems may be on the way. Firstly, and most importantly, it's clear that the ECB is about to raise interest rates, probably as early as this week. And once interest rates begin to rise, they will surely to continue to rise steadily for the next year or two, as the ECB seeks to return rates to more normal levels, say 2% to 3% above the current 'emergency' rate of 1%. This will impact on house prices in several ways:

- New buyers will get a smaller mortgage approval for a given level of income, as the monthly mortgage payments increase.

- Existing mortgage borrowers will have to finance higher monthly repayments. In many cases the extra strain could push borrowers into arrears and for some that could mean that they have to sell their homes, increasing the supply of houses on the market.

- Potential buyers, even those that are not significantly directly affected by the increase in mortgage rates, will be concerned that higher interest rates will lead to further house price declines, and may defer their purchase.

Of course, many borrowers have already had to cope with interest rate increases, as all Irish lenders have passed on to their customers the much higher interest rates that the banks must now pay on the financial markets, given the question marks about the banks' credit worthiness. Some borrowers have already seen several interest rate increases. Borrowers on tracker mortgages have seen no increases at all, as their lending rate is linked to the ECB's official rate, which has not changed - yet! It is the tracker-rate borrowers who will, of course, suffer for the first time when ECB rates rise soon.

Secondly, there is a risk - though only a risk, not a certainty - that there could be a surge of repossessions and forced sales of properties. While the banks have, in general, been quite unenthusiastic about forcing families out of their homes, for obvious reasons, and have furthermore been very constrained by the new code of conduct for lenders, this may not last forever. At some point the so called "extend and pretend" policies of the banks (extend the loan and pretend there is a chance that it will ever be repaid!) will come to an end. In a benign scenario, by the time the banks get tough on borrowers, the recession will be over, house prices will be rising, and so the problems won't be all that large. In a less benevolent scenario, the banks won't be able to wait that long and will be forced to start repossessions and forced sales of homes while the economy and the housing market is still very weak - and that's a recipe for yet further declines in house prices, of course.

Thirdly, there is a risk that the very negative assumptions used in the banking stress tests, and the large capital requirements announced as a result, will frankly give borrowers such a negative outlook about the future that even those that can pay, don't pay, as they can't see why they should pay their mortgages each month when so many others will not. This is called "strategic default", in banking jargon. In practice, I doubt that this risk will materialise. I can't really see many thousands of people deliberately running the risk of losing their house, and of course ruining their credit records, even though they can afford to pay their mortgage. But while I don't expect it to happen, it remains a risk.

All in all then, while I believe that there are genuine grounds to think that the economy as a whole has passed the worst, and may even be recovering very slightly at the moment, I am far from convinced that the same can be said about the housing market. Significant risks remain, and higher interest rates, in particular, could do further damage to house prices in the months ahead.

HIGHLIGHTS:

Asking Prices, Residential Sales

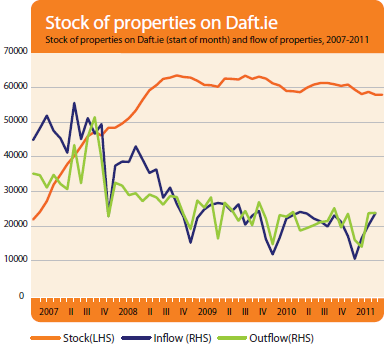

Stock and Flow of Sale Properties

SNAPSHOT:

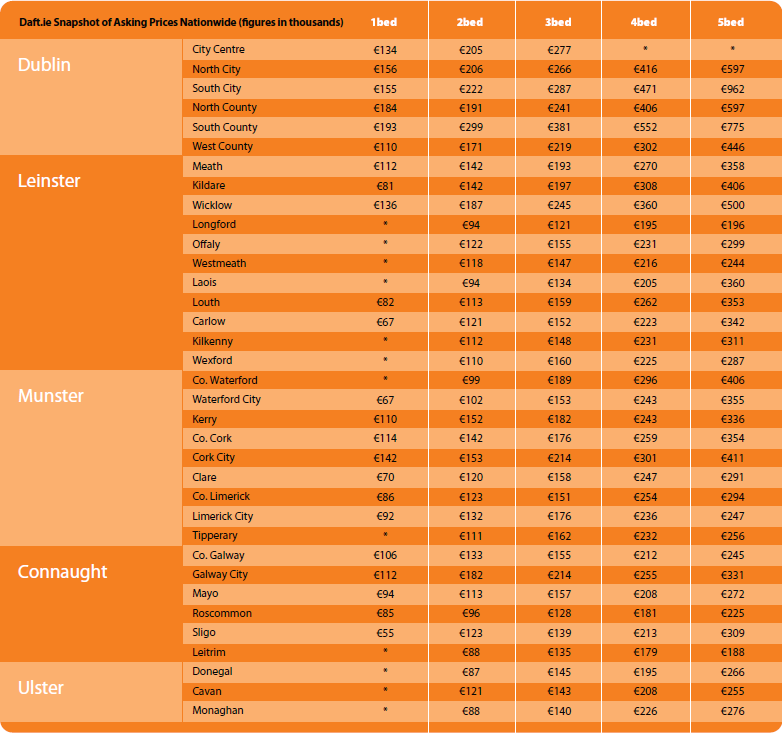

Snapshot of Asking Prices Nationwide