Housing Market on hold while waiting for an economic turn-around

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

17th Nov 2009

Dr Charles J. Larkin, Department of Economics, Trinity College Dublin, commenting on the latest Daft research on the Irish property market.

The world economy - and in particular the OECD grouping of 30 economically advanced nations - has undergone the most severe recession since World War 2. Among that club, Ireland has suffered the most acute economic contraction of all: GNP has fallen 13.6% from peak - or by more than 20% if foreign-owned export-orientated sectors are excluded. This has taken its toll on jobs, with unemployment rising to 12.6% in October and expected to reach 14% within months.

There are many origins of Ireland's crisis but the primary cause is macroeconomic imbalances, in particular in housing. The spectacular boom and bust of the housing market has seen investment in housing fall by more than half and house prices are falling rapidly. At the same time, household face falling disposable incomes, with unemployment, increased tax burdens and negative wealth effects arising from falling house prices. The government has had to adjust also, with reduced public services and public sector pay. Its priority now is servicing national debt, which is rising rapidly due to deficits of almost 13% this year and next. Ireland faces economic déjà vu, with a fiscal vista reminiscent of 1978/1979.

The OECD's recent review of the Irish economy indicated that the decline has begun to bottom out. This heartening conclusion does not imply a return to higher incomes, reduced unemployment or increased property prices. Ireland's membership of the Eurozone means Irish borrower enjoy historically low interest rates, but also that unilateral currency devaluation is not an option. International competitiveness can only be regained through general reduction of price levels. Vital elements of this process will be wage reductions in the non-traded sector and reductions in rents.

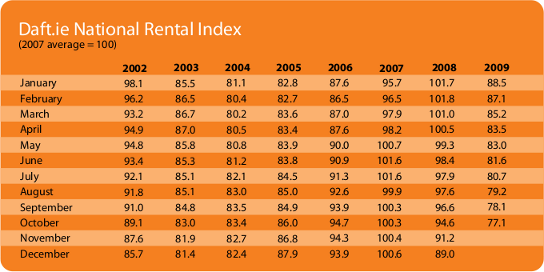

The third quarter Daft.ie Rental Report reveals significant reduction in rents across the country, with an average national reduction of 18.4% over the 12 months to October 2009. Average monthly rent is now €775. Reductions in urban areas have been quite marked. In Dublin, rents have fallen consistently with an average reduction across all sections of the city of 24.5% from peak and 20.7% from the fourth quarter 2008. Rents in the capital are now lower than in the first quarter of 2000. The most acute reductions were in Dublin's City Centre, where rents have fallen 26.1% from peak and 21.3% from the fourth quarter 2008, returning an average of €924 per month. It is now common practice to tell the story of the Celtic Tiger in two stages: the first of export-led growth, the seond of an easy-credit fuelled property/consumption bubble. Rents are now back to the levels of the export-led growth phase.

While Dublin's rents have fallen most, rents in other cities have also been significantly reduced in the last 18 months. On average, rents in the cities outside Dublin have fallen 19.5% from peak. The only exception to the ongoing falls is Galway City, where rents appear to be levelling off with a small quarterly increase of 0.4%. In total, rents there have fallen from peak values by just 15.6%, compared to larger figures in Cork (21.5%), Limerick (21.8%) and Waterford (19%). Elsewhere around the country, rents continue to fall but generally at a slower pace. Rents in Connacht (16.6% from peak) and Ulster (18.4%) have fallen by significantly less than those in Dublin Commuter Counties (24.3%), or Munster (21.4%).

These statistics reflect dramatic shifts in Irelandis demographic patterns. Net outward migration has begun, with 65,100 people leaving the country from April 2008 to April 2009. Of these, 30,100 were nationals of recent accession countries (69.4% male) and 18,400 Irish nationals (62.5% male). This represents a significant change. Net migration has not been negative since 1996. Peak inward migration was in 2006 at 71,800 persons, coinciding with the peak of the Irish property market. The peak of the rental market was in February 2008. This change in migration may pose challenges to the rental market over the medium term. The rapid increase in birth rate (at 74,500, births for April 2008 to 2009 were the highest in the State's history) may result in new sources of demand as households become first-time buyers, trade up or withdraw rental rooms from the market.

Historically, property crises coupled with financial crises produce sharp and lasting falls from peak value. In Ireland's case, economic recovery will depend upon export competitiveness. Addressing macroeconomic imbalances in the property market will be an important part of this process. This quarter's data indicate that a correction is afoot that will bring about such a real devaluation. The key issue is that of time. Households, already saving heavily, are in the process of adjusting to what Nobel Prize winning economist Edward Phelps refers to the "new normal" of lower growth and higher unemployment over the medium term. Adjustments will take time and typically overshoot before a new equilibrium is established. This may lead to fluctuations in the short-term, but long-term recovery in the housing sector cannot occur without the easing of credit markets and increases in real income.

HIGHLIGHTS:

Rental Index

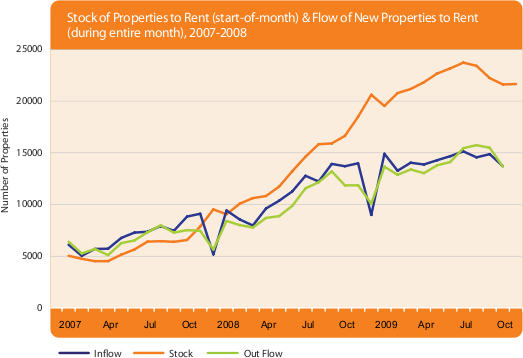

Stock and Flow of Rental Properties

SNAPSHOT:

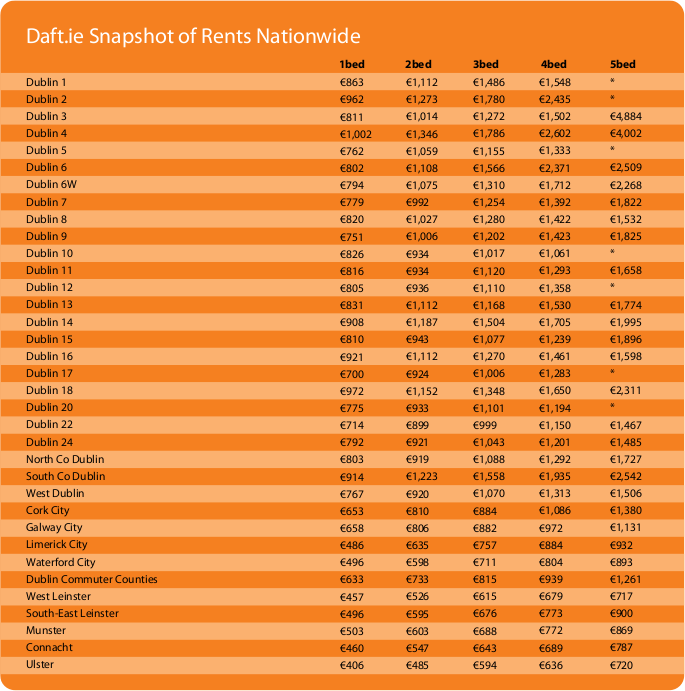

Snapshot of Rents Nationwide