Economy Has Turned One Corner, But Outlook Remains Challenging.

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

13th Jul 2010

Jim Power, Economist at Friends First, Lecturer in the Smurfit Graduate School of Business, commenting on the latest Daft research on the Irish property market.

Following a barrage of absolutely dire economic and financial news over the past three years, it came as quite a relief to learn that the Irish economy technically emerged from recession in the first quarter of 2010. However, not everybody is convinced about the significance of this technical development and a vigorous debate is now developing about the real status of the economy.

Gross domestic product (GDP) in the first quarter was a hefty 2.7 per cent higher than the previous quarter, the first quarter-on-quarter increase since the final quarter of 2007 and so must be welcomed by even the most sceptical amongst us. This does confirm that the recession is technically over. However, the more realistic measure of domestic economic activity, gross national product (GNP) contracted by 0.5 per cent. This metric has contracted in every quarter since the first quarter of 2008 and in fact has fallen by a dramatic 16.5 per cent over that period. However on a positive note, the decline of 0.5 per cent in the first quarter is the lowest rate of contraction over that period.

It is clear that having fallen off a cliff over the past three years, the Irish economy has now hit the ground and the question is how quickly it can pick itself up and start to recover in a meaningful way. Consumer spending and business investment are still very weak, while the construction sector is still in steady decline. Exports on the other hand are doing well, but it is a selective performance, dominated by the mainly foreign-owned chemical & Pharmaceutical, and IT companies. The picture that is emerging is of an economy being pulled out of recession by the multinational sector, while domestic demand still remains weak, but there is increasing evidence that it is starting to level out.

Much has been made of the fact that the labour market situation is still poor, as evidenced by the live register reaching 452,882 in June. There is generally a time lag of up to a year between the bottoming out of the economy and an upturn in the labour market, so there is hope unemployment will have bottomed out by the end of the year. However, strong growth in employment thereafter is a different matter entirely. It is very hard to identify too many sectors that might be net job creators over the next two or three years, and in fact it is not difficult to identify those sectors that could well shed further jobs. Job shedding is not yet likely to have ended in manufacturing, construction, the retail sector and financial services and it is inconceivable that the public sector can be a net job creator over the coming years given the requirement to correct the public finances.

The outlook over the next couple of years remains very challenging, not least because the external economic outlook remains very fragile. A recovery in domestic demand is required, but this is likely to be slow to materialise, so it is essential that policy makers remain focused on what I would regard as three key priorities - getting credit flowing in the economy, improving competitiveness a lot further, and addressing the structural imbalances in the public finances.

The sovereign debt crisis in Europe is far from over and is imposing significant funding costs on errant governments around the EU, including Ireland. It is imperative for Ireland that the fiscal consolidation continues in order to control funding costs, which are already significantly higher than they should be. If Ireland were to show any signs of swaying from the path of fiscal austerity, the cost of funding would soar to Greek-style levels and that would be disastrous for a country that is currently borrowing close to € 400 million per week. There is also a requirement to fundamentally re-structure the public finances to achieve stability and sustainability in the longer-term.

A total reform of all elements of public spending is essential, but the tax base will also have to be broadened and made more stable and predictable. More workers will have to be taken back into the tax net, water charges based on usage will have to be introduced, all tax allowances will have to be critically evaluated, and a property tax that is not based on transactions will have to be implemented. A property tax will have to be carefully engineered to prevent distortions, but it appears to me that it has to be first and foremost based on site valuation, rather than house valuation. Politically this will be difficult, but we must have a more predictable tax base if we hope to fund the increasing demands on public spending from demographic change over the coming decades. In my view the most economically efficient tax system is one based on a broad base, with relatively low marginal rates. Ireland has been going in the opposite direction in recent years.

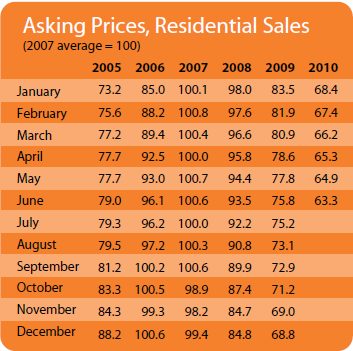

The need for a sustainable source of tax revenue from property is clear when one considers the ongoing uncertainty in the property market. The latest data from Daft.ie continue to suggest that activity in the housing market remains weak. Based on the demand and supply dynamics of the market, it is not too surprising that asking prices fell by over 4 per cent in the second quarter and that prices have fallen by over 7 per cent between January and June. On the demand side, the lack of adequate credit availability and low levels of buyer confidence due to a variety of factors are hampering demand. On the supply side, there is still serious excess supply all over the marketplace and this will be exacerbated by NAMA and financial institution engaging in fire sales over the coming years.

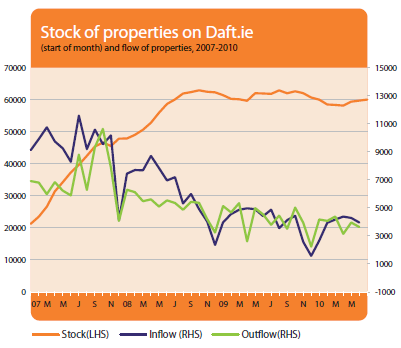

The latest Daft.ie supply data show that the total stock of properties for sale is rising again, and is now approaching 60,000. This probably reflects a view amongst aspiring sellers that the market may be starting to bottom out and they are now moving to sell. Having failed to anticipate the magnitude of the imminent house price collapse at the beginning of 2007, I am now far from convinced that the market is yet bottoming out. I anticipate that average prices could fall by around 12 per cent this year, and completions could be lower than 12,000. Any meaningful recovery in 2011 looks unlikely. The housing market is not yet out of the woods, nor is the overall economy. A little progress made, but considerably more to be made.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Properties

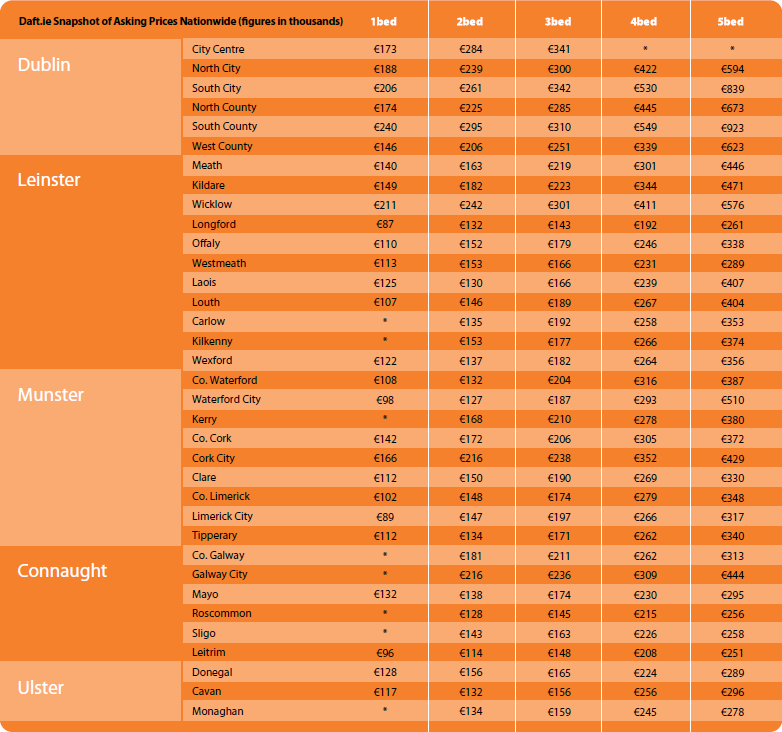

SNAPSHOT:

Asking Prices in Q2, 2010