Rents rise by half a percent in early 2011

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

10th May 2011

Cormac Lucey, chartered accountant and lecturer at the Irish Management Institute, commenting on the latest Daft research on the Irish property market.

Ireland had one of the biggest bubbles in recorded history, as measured by the growth in credit relative to national income. It should have been no surprise, therefore, that we would experience one of the biggest busts. And, since 2008, the economic news from Ireland has been unremittingly dismal.

Therefore, I would have expected rents in Ireland to have continued the sharp downward trend evident in 2008 (-12%) and 2009 (-16%) into 2010. The economic news flow and reality in 2010 was truly awful. Forecasts of Irish economic growth continued to fall. The ESRI predicted annual net emigration averaging 50,000 per annum. Deposit outflows from Irish banks led to a dangerous dependence on emergency ECB and to lack of availability of bank credit. The government was forced to turn to the IMF/EU/ECB troika for funding. Having made budgetary adjustments of €15 billion prior to Budget 2011, Ireland had to brace itself for an additional €15 billion worth of budgetary adjustments.

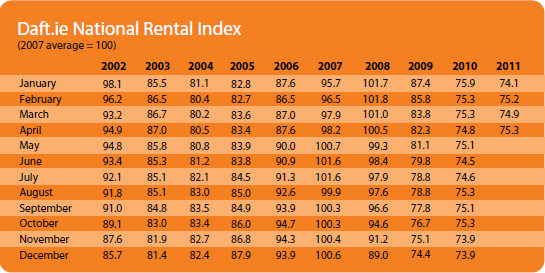

But the evidence supplied by the latest Daft.ie Rent Report is that rents in Ireland did not continue their sharp downward trend in 2010. Instead rent levels have stabilised. Rent levels in April were marginally (0.6%) higher than a year previously and markedly (1.5%) higher than a quarter previously. Indeed, rents in Dublin have risen in three of the last four quarters.

The fact that rents do not appear to have dropped in 2010 challenges my previous thinking and raises an important question: why have rents stabilised despite an enormously challenging economic environment?

The most likely explanation is that the underlying Irish economy should be able to generate annual economic growth of the order of 3% per annum. And, while our economy has suffered some horrendous setbacks over the last few years, the impact of new horrors is now being counter-weighed by the economy's underlying growth potential. It's not that things are getting dramatically better. It's just that bad news is now being counter-balanced by underlying forces of growth in the economy. So, on a net basis, economic activity and related variables (such as rent levels) are now stabilising.

This underlying resilience in the real economy is heartening when one considers that all of Ireland's economic policy settings are currently set against growth:

- With many billions of budgetary adjustments still ahead of us, fiscal policy will remain very restrictive.

- Turning to monetary policy, the ECB has started raising interest rates even though a recent Credit Suisse study suggested that an appropriate policy rate for Spain, Ireland, Greece and Portugal would be minus 4.6%! After a decade where ECB policy rates were inappropriately low for Ireland, we now face several years where they will be inappropriately high. The systematic mispricing of credit - and all of the economic distortions which flow from that - is set to continue.

- Following the recent stress tests, Ireland's credit policy is starkly restrictive with banks reducing the amount of credit extended to the economy as a matter of official government policy.

- And, with the Euro strengthening in recent times, recent currency moves are imparting further deflationary impulses to an economy.

So, like a boxer who has taken several shuddering blows to the head, the Irish economy is bloodied, reeling and stumbling. But it refuses to hit the canvass even as more blows rain upon its head. That is the good news. But the bad news is that a stabilisation in economic activity and rental levels are just a necessary but not sufficient condition for a fully-fledged economic recovery. The root of our economic disaster lies not in the fall in national economic output, appalling though that is.

The root of our economic disaster lies in our national balance sheet. The asset side is dominated by property assets which continue to fall in value. Meanwhile our liabilities mount. All the while, our equity (total assets - total liabilities) shrivels.

Ireland is experiencing both the processes of debt-deflation (described by Irving Fisher in the 1930s) and a balance sheet recession (the model recently used by Richard Koo to describe Japan's multi-decade recession). For Ireland to truly hit bottom we need a lasting floor in property prices and a halt to the destruction of our national equity / wealth. That looks a long way off.

Rental yields in Ireland (annual rent divided by property value) are averaging 4.0% according to the Daft.ie Rental Report. Such a low rental yield looks absurd and unsustainable when a risk-free investment (German government 10-year bonds) currently yields 3.3%. If Irish residential property was traded on the stock market could it possibly merit a Price/Sales ratio of 25?

Absurdly low rental yields are a signal that residential property prices still have a considerable distance to fall. They are a signal that the equity positions of house-owning Irish citizens will continue to shrink. And they are a signal that, while economic activity may stabilise, consumer spending will remain under pressure as citizens, fearing a pauperised old age, save to repair their ravaged balance sheets.

Rent levels have stabilised. Property prices have not.

HIGHLIGHTS:

Rental Price Index

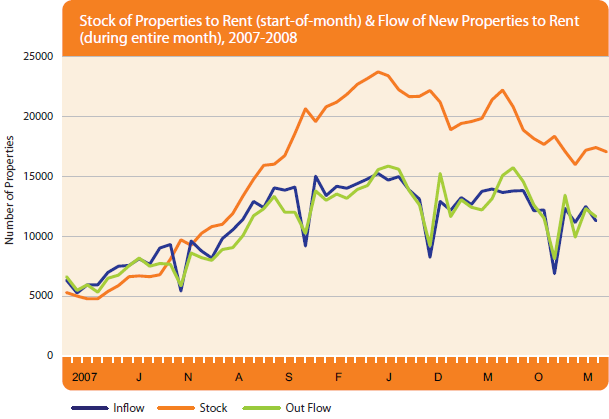

Stock and Flow of Rental Properties

SNAPSHOT:

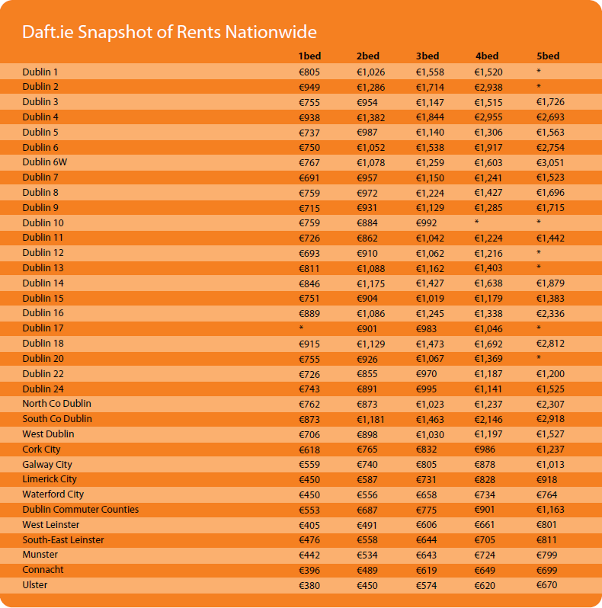

Snapshot of Rents Nationwide