Smallest quarterly fall in prices since 2007

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

2nd Apr 2012

Seamus Coffey - Lecturer in Economics, UCC

Recovery will require lending - that reflects fundamental value

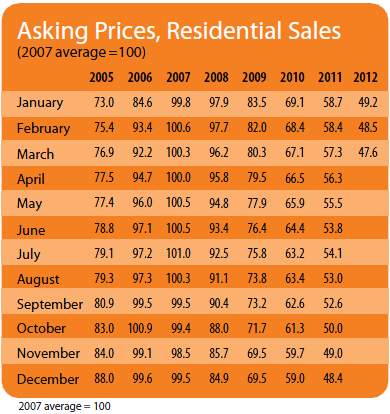

According to this latest daft.ie report, the first quarter of 2012 provided the least change in the property market since the middle of 2007. Asking prices continued to fall, but the drop of 1.7% is the smallest quarterly drop since the market collapse began in earnest in 2008. Meanwhile, in the rental sector, stabilisation has been present for almost two years and nominal rents at the start of 2012 are no different than they were at the start of 2010.

Measuring the fallMeasuring prices in the Irish property market continues to be an art rather than a science. Using mortgage market data, the Central Statistics Office reports that house prices fell by over 4% in the first two months of the year. When looking at falls from the peak, though, a different picture emerges. The daft.ie report shows a total fall of 53%, compared to 49% in the CSO index. The scope for divergence in estimates of falls from the peak will hopefully be put to an end when a National House Price Register is launched later this year.

House prices are always and everywhere a function of bank lending, but they do have a fundamental value to which they must eventually return. This can be given as a ratio to household income or, more usually, annual rents. A good guide is that house prices should be somewhere between 12 and 15 times the annual rent that a property can generate. This is a range that should never be ignored but often is.

A market that has normal level of activity would be near the top of this range but a malfunctioning market will be towards the lower figure and possibly even below it. And Ireland does not have a properly function property market.

A depressed marketData from the Irish Banking Federation show that there are fewer than 4,000 mortgages being drawn down each quarter, with around half of these going to first-time buyers and a further third to mover-purchasers. The remainder is largely accounted for by re-mortgages and top-ups. The residential investment borrower has virtually disappeared.

Anecdotal reports suggest that around 30% of all purchases are by cash buyers. This cannot be independently verified but a figure close to it would suggest there are around 4,000 residential property transactions a quarter. Ireland has a housing stock of around 2 million units. An annual turnover rate of less than 1% is indicative of a market that continues to be distressed.

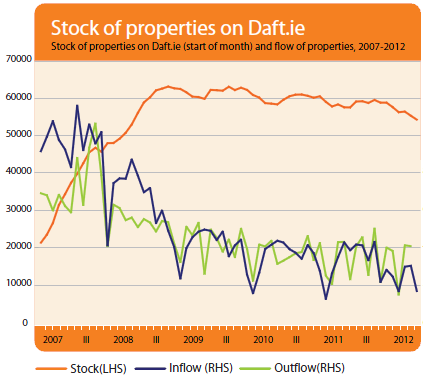

The stock of properties for sale on Daft.ie in March 2012 was 54,000, which is the lowest level in four years. This could be because properties on the market are selling quicker or because the number of properties being offered for sale is declining. The speed at which properties on Daft.ie found a buyer did increase slightly in the first quarter but two-thirds of properties remain on the market for four months or longer before finding a buyer.

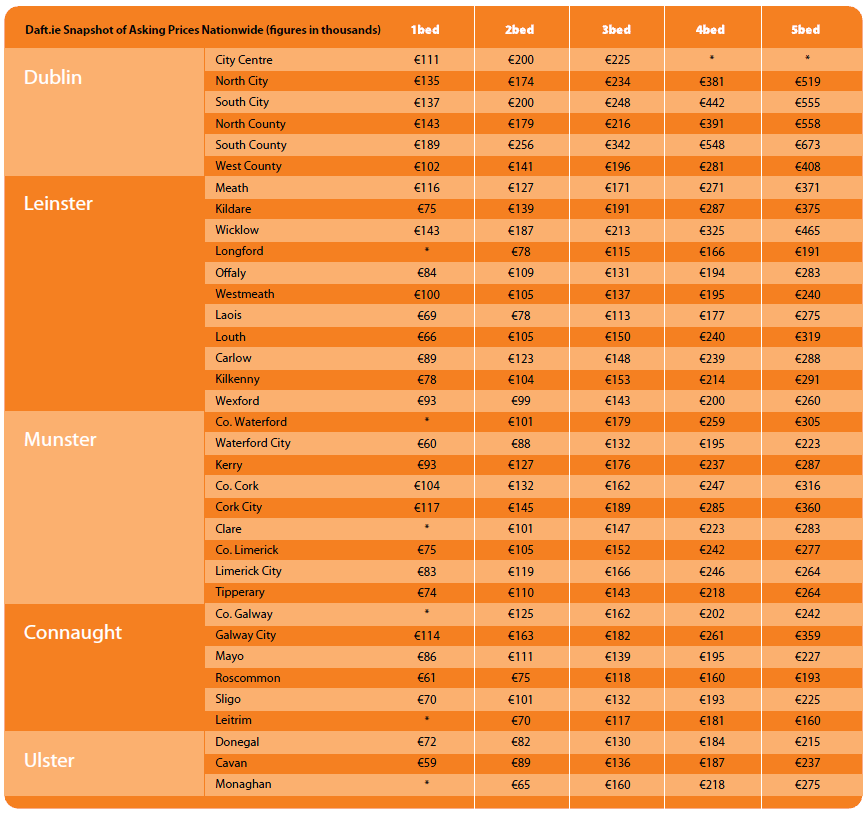

Thinking like investorsThe average asking price for the first quarter of 2012 was €176,000. In order to justify that price using the above range, the monthly rent should be somewhere between €1,000 and €1,250. Averages do not provide the necessary insight and this must be done on a town-by-town or even a street-by-street basis.

For example, a three-bed house in Cork City had an average asking price of €189,000 in the first quarter. The average asking rent for a similar property is €850 a month. The annual rent is still more than 18 times the asking price. At a ratio of 15 times annual rent, a monthly rent of €850 should equate to a price of around €155,000. By this metric, asking prices for three-bed houses in Cork City are still around one-sixth over-valued. This can be repeated right around the country. With the inability and unwillingness of banks in Ireland to issue loans a fall below this level is all but guaranteed.

The importance of lendingJust as the banks are almost certain to cause an undershooting of property prices relative to their fundamental value they must accept the responsibility for the market bubble that peaked almost five years ago. The banks based their lending model on the prices that people were willing to pay for properties, but seemed to ignore the fact that the price someone was willing to pay was based on how much a bank was willing to lend to them.

A house in a particular estate may have sold for €350,000 because one bank was willing to lend one purchaser the money for such a transaction. The other banks provided similar mortgages to other buyers on the basis that the first transaction provided the "market value".

The price reflects the amount of money that someone is willing to pay for a good. Value reflects the benefits that a good can offer. In most cases, these are the same but this does not have hold. Residential property provides accommodation service. As a result of the madness of the boom, we now have thousands of households paying a price for accommodation far in excess of the value they are receiving.

This reality must be addressed and the burden of the mortgage debt is largely a function of the actions of the banks so they must offer what ever forbearance is necessary to assist households. The banks must also realise that there are thousands of homeowners who will never be able to repay the huge loans they issued to them. It is very difficult to gauge the number of unsustainable residential mortgages that need to be ended but it could be anywhere between 15,000 and 30,000. These are households who are in deep mortgage arrears and negative equity and have little prospects of recovery.

The banks must face up to losses that exist on these loans. The homeowners must accept that they will never be in a position to repay the loan and that by surrendering the property they will be able to make a fresh start. Households with unsustainable mortgages must be allowed to do so.

The recovery in the housing market will not be when prices start to rise; the recovery will be when activity starts to rise. With our ailing banks still in no position to lend and the many problems created by the bubble still outstanding there is no sign that this is about to change.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Sale Properties

SNAPSHOT:

Snapshot of Asking Prices Nationwide