Tsunami of negative news battering buyer confidence

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

9th Jul 2008

Fergal O'Brien is our guest blogger, analysing the Quarter 2 2008 figures.

I was in national school in 1986 and we were always sent to bed as soon as the 9 o'clock news came on the TV but I still recall Anne Doyle's headlines on our faltering economy from those dreary days. Anne Doyle is still reading the news and her headlines of recent weeks remind me a lot of the mid 1980s. Thankfully of course I know our economy is not on a path back to 1986 and we can all point to an array of indicators to prove that the fundamentals of the Irish economy are on a much more solid basis than they were then. Nevertheless, there is a weakness not seen for many years and the current barrage of negative commentary and news on the Irish economy is further damaging the already fragile property market. Right now it takes a brave buyer to keep their head about them when all around are losing theirs.

Fundamentals and sentiment now both in declineWhile sentiment in the residential property sector has been weak for almost two years now, the past month has probably seen the sharpest decline in buyer confidence. The ESRI/IIB consumer sentiment index hit an all time low in June and the most recent increase in the European Central Bank (ECB) base rate will further damage confidence. During much of the past year it could be argued that the fundamentals of the housing market were actually improving as falling prices, stable ECB rates, rising incomes, stamp duty changes and substantial improvements in mortgage interest relief combined to improve affordability. More recent months have seen a reversal in some of these fundamentals, however, as the credit crisis hit Ireland with a vengeance. The main lending institutions have tightened mortgage criteria in recent months - 100% mortgages are a thing of the past and an increasing number of potential buyers are finding it difficult to secure credit. There has been a series of increases in variable mortgage interest rates since the spring, while many institutions have increased the cost of tracker mortgage products.

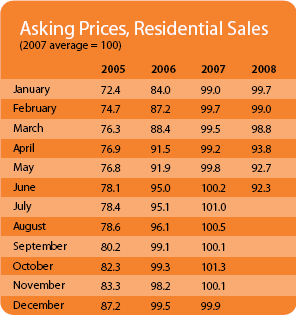

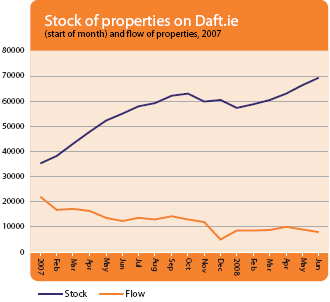

The impact of a combination of tighter credit arrangements and plummeting sentiment is clearly evident in the housing market trends of the most recent Daft.ie report. As would be expected prices in Quarter 2 fell in almost every county and nationally prices were 6% lower than in Quarter 1. What is most striking in the report, however, is the very sharp reduction in activity in the market. The 'flow' of properties on to the market declined sharply during Quarter 2, while stock levels rose to 70,000 units and have doubled in a period of just 18 months. The 'flow' of properties was just 8,000 units in the month of June and was 50% lower than in June of last year.

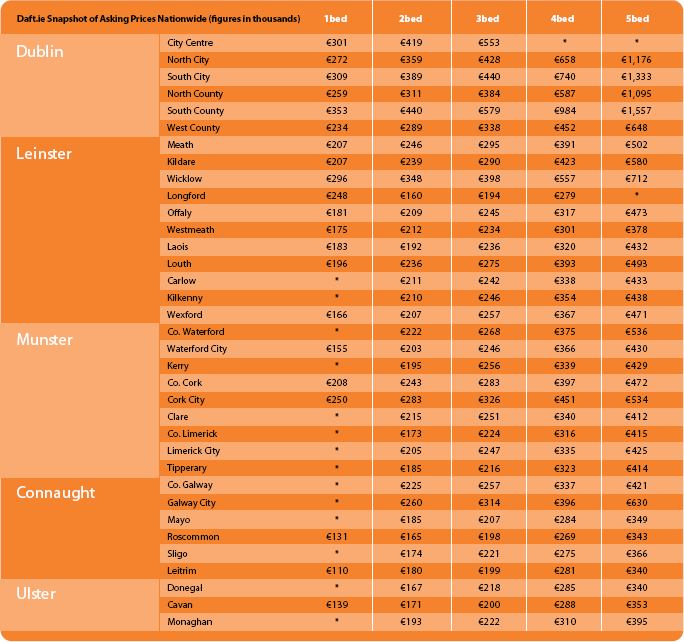

Price trendsAsking prices were down 7.9% nationally in the 12 month period to June 2008. Prices declined in every county over the past year with the sharpest falls recorded in Dublin, the commuter counties of Leinster and parts of Connacht/Ulster. Asking prices have held up much better in Munster, in Limerick, for example, prices have only fallen 1.6% in the past 12 months and actually increased marginally in the most recent quarter. It also appears that the pace of price decline has eased in Dublin in the most recent quarter but has accelerated in the rest of Leinster and in much of Connacht/Ulster.

Significant divergences emerging at regional levelThe price trends and the stock data suggest some significant diverging housing market trends for the different regions. The most recent quarter in particular has seen a sharp reduction in prices in commuter counties and in those counties which had previously benefited from generous tax reliefs through the Rural Renewal Scheme. With the price of oil close to $150 a barrel and pump prices in Ireland hitting record highs, I suspect that many prospective and current property owners are reassessing the cost benefit of long-term commuting. We have already seen in the US that house prices in commuter areas are falling much faster than in urban areas as oil prices have rocketed. This trend is likely to become more evident in Ireland in the coming years as economic and quality of life factors discourage long-term commuting patterns.

Excess housing supply also appears to be greatest in the regions and in some of the commuter counties. The counties which benefited from excessive tax reliefs in the past are now likely to experience a severe housing contraction for many years to come. The most extreme example of this can be seen in Longford where the number of new house registrations (using the Homebond and Premier data) totalled just five units in the first five months of 2008 compared to 650 units in the corresponding period in 2006.

In search of silver liningsIn relation to both the wider economy and the housing market it can be difficult to see an upside in the short-term when such negative data-flow continues to wash over us. Overall I remain very positive on the medium-term outlook for the Irish economy. Once the current housing correction is behind us and international credit markets return to some form of normality, the evidence supporting the ESRI view of near 4% trend growth in the economy is compelling. The housing market correction is already well advanced as housing starts have reacted swiftly to over-supply and stock levels in much of the country could clear fairly rapidly once confidence returns to the market. I suspect we will hear a few more terror inducing headlines from Anne Doyle before the end of this year but as we look into 2009 a moderation in world oil prices and subsequent reductions in ECB interest rates could be the kick-start that the Irish housing market desperately needs.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Properties

Average Asking Prices across Ireland in Q2 2008