Asking prices fall sharply in final three months of 2011

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

3rd Jan 2012

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

What's another year? Confidence and finance the keys to recovery

And so another year of Ireland's property market crash draws to a close. It is unlikely that years down the line, 2011 will be remembered in the annals of Ireland's property market. It is much more likely to be tucked away between the start and end dates of what will be regarded as the legendary Irish property market crash.

But that does not mean that nothing of note happened in the Irish property market in the twelve months just past. I would highlight three significant developments, all of which happened in the final three months. The first was the announcement the Government is going to unveil its property tax plans early in the new year. By telling future buyers of property what their annual tax bill will be, this will reduce the uncertainty they face.

The second important development is the Budget announcement that rent supplement thresholds will be reviewed in the new year. By reducing the price floor in the rental market, this will have implications far beyond those in receipt of the supplement. For other renters, it will mean cheaper rents. And for property owners, it will mean lower house prices, because of the fundamental relationship between house prices and rents. A property's price is best thought of as a multiple of the annual rent that would be paid. In healthy markets, this is usually about 15 times the rent so if market rents fall, house prices should fall too.

Sharpest falls yet in late 2011

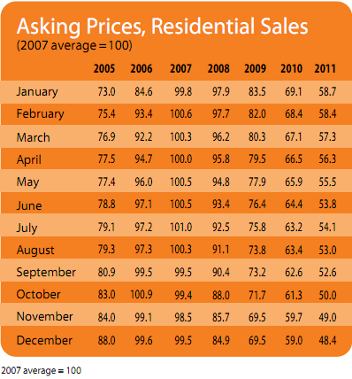

The third significant development was the dramatic fall in asking prices in the final three months of the year, outlined in this report. Until the third quarter of this year, the case could be made that house price falls had been slowing down. The typical quarterly fall had been over 5% in 2008 and 2009 but was under 4% in 2010 and into 2011. However, in the final three months of the 2011, the average asking price fell by almost 8%, by far the largest quarterly fall yet. It means that the fall in asking prices over the course of 2011 was 18%, as large as any of the falls seen in 2008, 2009 or 2010.

Such a dramatic fall in asking prices could reflect greater realism on the part of sellers, as they see fire-sale auctions resulting in prices 70% below the peak and cut their prices to compete. Or it could reflect the impact of on-going international economic uncertainty and pessimism about Ireland's economic future. More than likely it reflects both.

It is somewhat ingrained in Irish commentary to see larger falls as a bad thing and no doubt many, particularly those in negative equity, will see this dramatic fall in those terms. However, if you think of the fall in house prices as a necessary correction, whose size is determined by fundamental factors, then it is better for the prices to race to the finishing line than to crawl there.

Predicting the bottom

But how far must prices fall? Picking the bottom of the market is a mug's game. Nonetheless, income multiples and more reliable rental multiples do give us some indication of what to expect. They suggest that a fall from peak prices of around 60% is to be expected, provided rents do not fall substantially after rent supplement thresholds are reviewed. Given that the average asking price nationwide has already fallen 50%, one more year of house price falls could suffice.

Indeed, in parts of Dublin, the average asking price has already fallen by 60%. Does that mean we should expect to see prices rising again sooner rather than later? First things first: rising house prices is a bad thing. The golden rule of house prices is that over the long run, they don't increase any faster than inflation. We can see this everywhere: in Ireland up to 1995, in the US over the last fifty years or over the Netherlands over the last four hundred years. So, if we're seeing house prices rising any faster than about 2% a year, as we did during our bubble, something has gone wrong. What the market needs is stable prices, not rising ones.

Finance and confidence

One of the key points to remember, when we talk about the property market recovering, is that recovery in the property market does not mean an increase in prices. Recovery means an increase in activity. In 2011, banks issued about 13,000 mortgages. In 2006, the same banks gave out over 200,000 mortgages, meaning we've seen a fall in lending of almost 95%. Given that the property market in any developed economy is inextricably linked to the mortgage market, it's no surprise that prices are down 50% or more, if lending is down by over 90%.

Banks will say that much of the fall in their lending is due to a lack of demand: trader-uppers are stuck in negative equity, while first-time buyers are either unemployed (and possibly emigrating) or, if they are employed, worried about their jobs and their take-home pay.

But while fifty thousand 25-34 year-olds have emigrated and another fifty thousand are newly unemployed, there are still over half a million 25-34 year-olds - the household-forming age - at work. These are the people who would, in other circumstances, be kick-starting activity in Ireland's property market.

They are not doing so because of two factors: a lack of finance, but also a lack of confidence. Finance is down to the banks and banks will not resume lending until the stress tests stop punishing them for doing so. Without finance, there's a real risk that prices will overshoot on the way down.

Confidence is trickier - government policy can do little overnight to boost perceptions of Ireland's economic future. It can have an impact, though, by removing uncertainty about property tax, which it is doing, but also by publishing transaction prices, bringing in lending guidelines (including a maximum loan-to-value) and changing how banks fund mortgages. Because overshooting on the way down increases the likelihood of another bubble down the line, these measures are not so much luxuries as necessities.

HIGHLIGHTS:

Asking Prices, Residential Sales

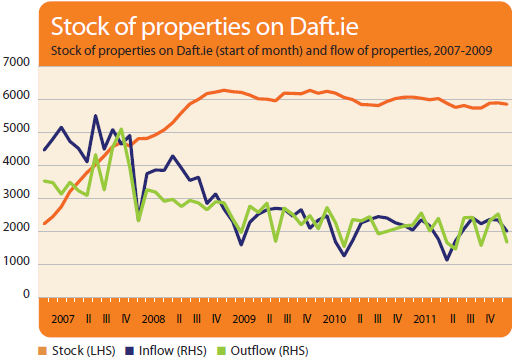

Stock and Flow of Sale Properties

SNAPSHOT:

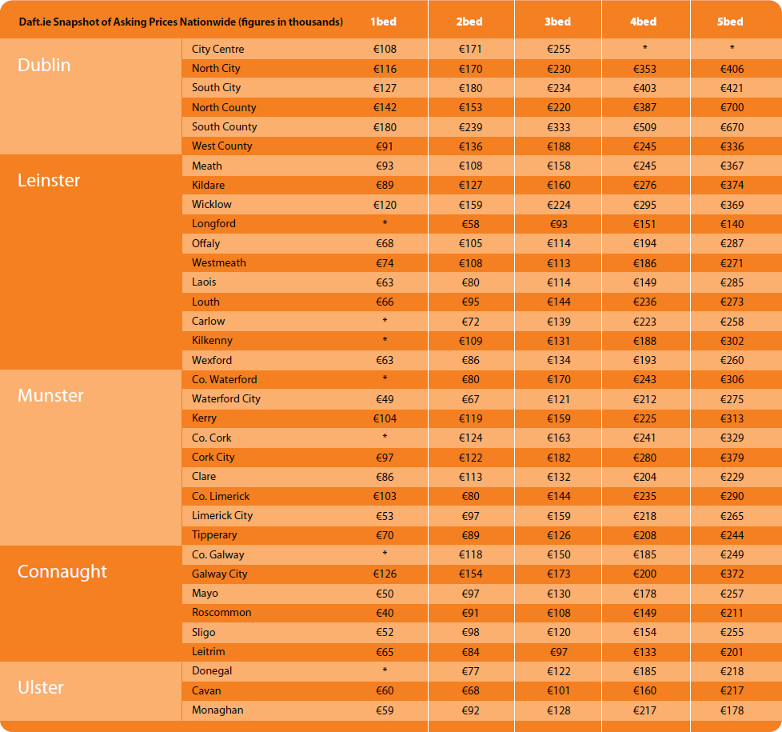

Snapshot of Asking Prices Nationwide