Where are we? Insights from the price-rent ratio

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

11th Nov 2013

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Where are we? Insights from the price-rent ratio

For pretty much everyone involved in the property market - including home-owners, would-be first-time buyers, investors and the Government - it is natural to wonder where house prices are now and how that compares to where they "should" be. I’ve put "should" in inverted commas, as there is of course, no definitive answer to this. Nonetheless, there are metrics we can use to assess the housing market and they can shed insight on the current level of prices.

A popular one is the ratio of household incomes to house prices. There is lots of barstool wisdom on this topic - indeed it was reported last week that some TDs wanted to tie mortgages to the historic relationship between house prices and income. While the price/income ratio is useful, it is at best a rule of thumb and can vary from generation to generation, so historic comparisons may not be relevant. For example, compared to incomes, house prices are going to be a lot lower when interest rates are high than when they are low and our current interest rate environment is very different to the one that applied in the late 1970s and early 1980s.

Survey evidence suggests that people are looking to borrow roughly 3.5 to 4 times household income when applying for a mortgage, so in general the price/income ratio seems roughly right but that is about as precise as one can be.

A second metric is the deposit required by the typical first-time buyer. This tells us less about where prices should be but is very informative about the amount of risk that the system (both borrowers and lenders) is taking on. A typical deposit of 20% means the system is well insulated against price downturns. A system with just a 2% or 5% deposit is not, as Ireland found out to its cost in the last decade. Again, hard figures are difficult to come by but Central Bank figures indicate that the deposit required of the typical first-time buyer recently was between 15% and 20%.

But while those investing in our real estate or in our banks will look at something like the typical deposit as a measure of risk, they also want a measure of return. How does the price of a property compare to its fundamental value?

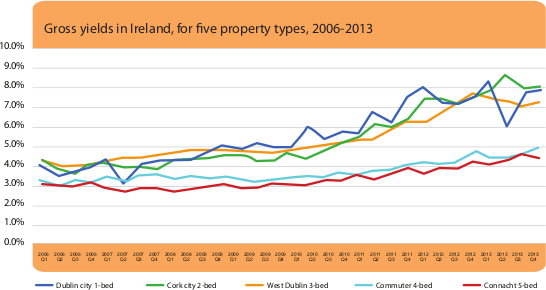

The graph shows the gross yield - that is, what fraction of the price is the annual rent - for five property types (from 1-bed to 5-bed, urban and rural) from 2006 to 2013, reflecting the latest figures contained in this Daft.ie Rental Report. How should this yield figure be read? In short, for homeowners, it should equal the mortgage interest rate plus a premium to reflect the risk of owning real estate (relative to the risk of renting).

Back in 2006 or 2007, someone like me might have stated that a 4-5% yield would be enough to both pay back the interest and reflect the risk taken. (In fact, I did think this.) These days, people think that realistically long-run interest rates for borrowing are likely to be at least 5% so the yield should probably be that plus whatever risk premium for buying rather than renting.

The significant correction in yields since 2007 - from 3% to 5% for 4-5 beds and from 4% to 8% for 1-3 beds - makes a lot of sense when viewed in this light. What we have seen in the Irish housing market over the last seven years can be understood as first prices correcting to reflect both risk and return being miscalculated and then - as rents fell reflecting unemployment and the decline of the real economy - prices have to fall by more to compensate.

What is interesting is the end of the upward trend in yields for, say, a three-bed home in West Dublin. In that segment, market participants seem to have decided that the balance between rents and prices is about right and the gross yield has fallen from about 7.5% earlier in the year to 7% now. This - together with reasonably healthy findings in relation to income multiples and the typical deposit - is encouraging for those affected by the housing market.

A concern remains, however, about the low yields on family homes, both in the cities and elsewhere. While the average yield for a 3-bed nationwide is now 6.5%, it is 5% for 4-beds and 4.2% for 5-beds. This may be a simple reflection of the fact that, unlike owner-occupiers, investors (who primarily own 1-3 beds) have to worry about tax on their rental income and so require a higher gross yield. Or it may be a sign that the correction is not fully over yet. The economic literature is remarkably silent on this point so unfortunately, only time will tell.

HIGHLIGHTS:

Rental Price Index

Stock and Flow of Rental Properties

SNAPSHOT:

Snapshot of Rental Prices Nationwide