Housing: In the eye of the storm?

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

1st Oct 2009

Emer O'Siochru BArch RIAI, Director of Smart Taxes, commenting on the latest Daft research on the Irish property market.

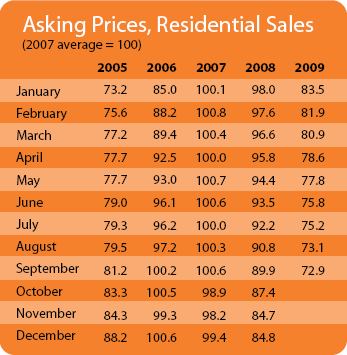

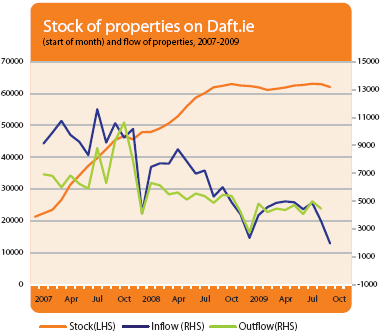

The first anniversary of the bank guarantee is nearing, and while the Irish housing market shows signs of less volatility it is still on a downward trend, albeit marginally less precipitously. Asking prices fell by 4.6% over the last three months, a smaller fall than the preceding quarter. The number of houses available for sale on the market is holding remarkably steady at around 60,000 at any one time. The most recent drop is probably the result of more realism by sellers, especially in the Dublin area, where asking prices have dropped by 30% from the peak in 2007 compared to only 25% outside the capital.

The graphs in the current Daft report show that houses in urban areas generally took a shorter time to find a buyer than in rural areas. Whether this was due to price cuts, wider demand (more investor interest) or deeper demand (more first time buyers) is difficult to say. It is interesting that the highest falls in value are in Dublin city centre (-33.7%), where the highest number of rented/investment properties might be expected. It would be useful to compare falls in rent levels to falls in asking prices in particular areas to see if one is influencing the other.

When we turn to Munster, we find a different picture - the region has experienced the smallest drops in asking prices, which are typically 20% lower than at the peak. The other side of this story is increasing time to sell, from 3 months in late 2007 to over nine months now, and unlike elsewhere the overall stock of properties for sale is still increasing. This could be simple psychological denial, but may more prosaically be accounted for by the more discretionary nature of much of the Munster housing market. Cork and Kerry are established second home, holiday and retirement home areas.

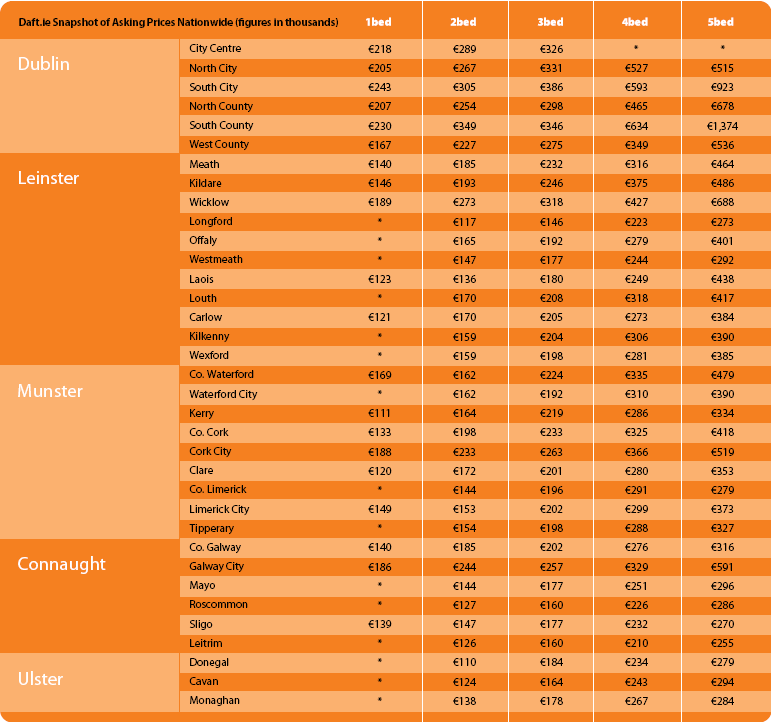

House prices in Connacht & Ulster (excluding Galway city) are already the lowest in the country, typically €182,000 - €220,000, but they are still remaining unsold for over a year. We do not have breakdown by construction date, but from what one sees driving around the West, most are new. As rural houses are generally larger than urban, these prices must be approaching construction costs, meaning that their site value has eroded to very little. These areas enjoyed the longest lived and most generous tax relief in the country and are the heart of Namaland. Not only are they worth next to nothing, many have already cost the exchequer considerable sums.

Meanwhile, the Leinster commuter belt around Dublin shows similar trends. It has some of the largest falls in asking prices, more than 30% in Meath, Louth and Westmeath, but unlike the urban areas, not matched by shorter time to sale.

One can well imagine the family desperation that these figures represent; two parents with one job between them; in negative equity, certainly; their home nestling in a forest of fading for-sale signs.

The self reinforcing cycle of housing-needing construction workers-needing housing has reversed as CSO figures show net emigration of the very kind of people that buy and rent houses. Economist Brendan Walsh estimates that the number of individuals aged under 45 years (who might loosely be identified as potential 'first time buyers') will collapse from 24,000 a year in 2002-06 to minus 6,000 in 2016-21.

The bankers are unprepared for the next great wave of personal debt that is swelling up and will hit them in 18-24 months time. The current NAMA deal leaves their balance sheets so perilously weak that they will have little choice but to cut jobs and raise rates and fees. None of this augurs well for families in debt.

It is Dickensian that the totally inadequate Mortgage Interest Supplement Scheme is all that stands between many Irish families and the debtors prison. The Law Reform Commission report on personal debt is very welcome and should be immediately acted upon, but it makes no recommendations to address the root problem of crippling mortgage and other personal debt. The government should do more for indebted homeowners than offer an earnings attachment or a rental lease of their own home. Substantial write-down of the original loan capital owed must be part of the solution.

Another mechanism is the 'Equity Partnership' proposed by the Urban Forum which is a clever way to swap debt for equity. Families in serious mortgage arrears can transfer their home to an Equity Partnership and stay put paying a cheap rent with the option to pay more when they can afford, to regain ownership. Equity Partnerships also offer social housing providers a better economic deal than leasing under the new 'Rental Accommodation Scheme' (RAS), a way of resolving the perennial estate management problem as well as dissolving distinctions of tenure and income in housing schemes.

Demographic change and global recession has put a stop to the gallop of land speculators and politically connected developers for the time being but the final solution will come only when unearned upswings in land value are taken out of the property profit equation - permanently. There is no better way to do that than an annual land value tax (LVT). LVT removes 'hope value' leaving developers and builders to profit only from the quality and efficiency of the design and construction of their product - like any normal business. When the Building energy Rating (BER) of houses listed in the Daft Report becomes a reliable predictor of house value, we will know we are getting there.

Under LVT, the 'hope value' of the land is collected by local and central government and used to build and maintain the services and infrastructure that added most of the value in the first place, and which is needed as communities expand. LVT short-circuits the natural boom-bust cycle generated by economic and population growth, holding property prices steady and affordable, and business competitive. The surplus generated in these conditions can be given back as a citizens' allowance or dividend. In this way LVT can be very progressive; a fact that was recognized by Union Representative Brendan Hayes on the Taxation Commission who dissented from many aspect of the final report because of their effect on ordinary working people and the poor.

Emer O'Siochru BArch RIAI, is an Architect and Planning and Development Surveyor, currently Director of Smart Taxes, a policy development network funded by the Department of the Environment; a founding member of Feasta the Foundation for the Economics of Sustainability and through the new Environmental Partnership, a member of the Housing Forum. Emer is also principal of EOS Future Design, a sustainable systems and settlements developer.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Properties

SNAPSHOT:

Snapshot of Asking Prices in Q3, 2009