Effect of mortgage caps seen in reverse two-tier market

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

7th Jul 2015

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

The official line from the Central Bank is that the measures it took to cap mortgages earlier in the year were taken for the sake of financial stability, rather than for the sake of the housing market. In other words, the main objective of macroprudential policy is to make sure Ireland's banks don't collapse again, not to make sure Ireland avoids another housing bubble. Strictly speaking, that is not the Central Bank's job.

Nonetheless, such a technical distinction is largely irrelevant as, across the developed world, the housing market is now central to financial stability. Therefore, if financial stability is the end, housing market stability is one of the principal means to that end. Given all that, the Central Bank is likely to be very happy with the early results of its measures.

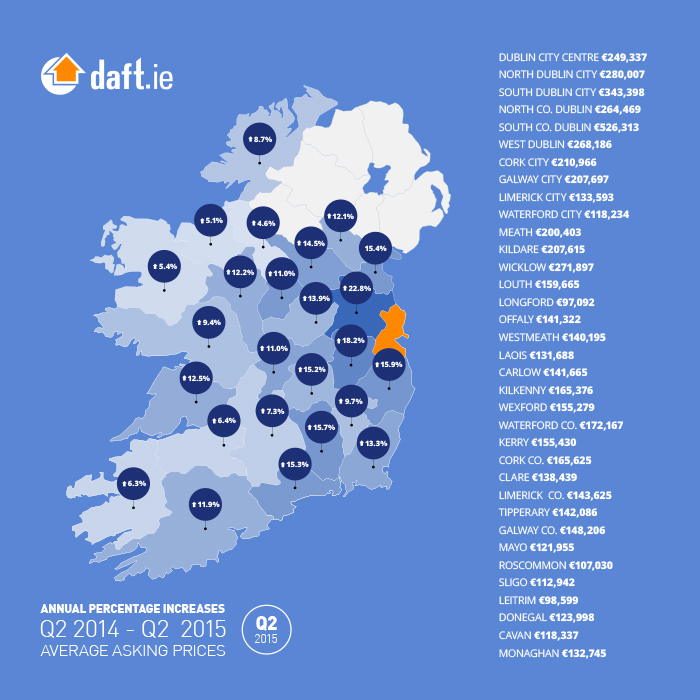

To see this, think about the housing market nine months ago, before the Central Bank had announced that it was even interested in capping mortgages. By that time, average list prices in Dublin had risen for 9 quarters in a row. Not only were prices consistently increasing, they were doing so at a faster pace with each passing quarter: by September 2014, prices in Dublin were increasing at 25% a year - and by 30% a year in markets such as Dublin 3, Dublin 7, Dublin 15 and West Dublin. In two short years, prices had not only bottomed out in the capital, they had risen by nearly 50% in areas such as Dublin 6, Dublin 14, Dublin 18 and South County Dublin.

While the early phase of the increase may have been a normalisation of expectations about future house prices - similar to what has happened elsewhere in the country more recently - the longer it went on, the more the housing market of the 2010s resembled that of the late 1990s. In the late 1990s, a shortage of supply at a time of strong demand sparked rapid house price increases. These increases fed into expectations, which combined with loose credit to create one of the world's worst housing bubbles on record.

Breaking the link between past house price growth and future house price growth requires normalising expectations and stabilising the link between credit and the real economy. The Central Bank's measures have done this, albeit not without some transitional bumps. Late 2014 saw asking prices fall across the country, as housing market participants worked through the effects of what was expected to be a mandatory 20% deposit.

But the actual caps required only a 10% deposit of many first-time buyers and something close to a 15% deposit for many first-time buyers in Dublin. This, combined with a rush of mortgage approvals before the new caps came in, saw a surge in prices in early 2015. As we pass the middle of the year, though, nearly all those with “old” mortgage approvals have either bought or seen their approvals expire. What we are left with is the new mortgage market and the housing market it can support.

The top of the market has seen the Central Bank caps have their desired effect. Compared to September 2014, the average asking price in Dublin 6 is actually 2% lower nine months later. In the country's four other most expensive markets, South County Dublin (+2.8%), Dublin 4 (+2.5%), Dublin 6W (+0.8%) and Dublin 14 (-0.3%), prices are effectively unchanged from their level nine months ago. In contrast, outside Dublin, prices have risen by 9% in the same nine months. A lot of the talk two years ago was of a two-tier housing market, with growth in Dublin and stasis in many rural parts of the country. If anything, the problem now is the opposite.

And therein lies an issue with the new mortgage system. Certainly, the minimum deposit requirement is a well- proven measure in fighting what economists term “excess leverage” - in other words taking on too much debt, which merely pushes prices up. However, the loan-to-income cap is a very crude extra measure that seems to bring far additional problems than additional safety, above and beyond the minimum deposit.

Banks already stress-test the borrower's disposable monthly income to see if the debt burden is too high. In principle, banks can also acknowledge the very real trade-offs borrowers face. For example, a borrower that wants to buy a more energy efficient home that is also more expensive can be accommodated if the extra debt translates into healthier household finances through reduced energy bills. Similarly, a household may want to borrow more to live closer to work, rather than to live further away and have to unnecessarily waste time and petrol.

This may sound somewhat theoretical but we are seeing this play out in the Irish housing market today. Since the start of the year, Dublin's Commuter Counties have seen average increases of 10% in just six months. The rest of Leinster has seen increases of 8%. Dublin's growth has always been viewed as something of a negative for the country as a whole by the political and planning system, despite overwhelming international evidence that the stronger the larger city, the more economically healthy its hinterland. Unfortunately, the Central Bank measures tilt the scale further against compact city growth.

At least, that is the case given the rest of the housing system currently. The Central Bank certainly can't be expected to solve the housing market on its own. And the solution to macroprudential measures encouraging people to live further out is not to remove those measures - instead, it is to address the high cost of building new homes, whether houses or apartments, in Ireland. This includes both the hard costs of a unit and the soft costs on top, including land, where the market in Ireland is highly dysfunctional.

Capping mortgages is just the start of building a healthy housing sector in Ireland. The Central Bank has done its bit. Now it is time for the rest of the policy system to act.