Economic outlook means property market adjustment not over yet

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

4th Jul 2011

Dr. Constantin Gurdgiev is the Head of Research and Strategy for St. Columbanus IA, and Adjunct Lecturer in Finance with Trinity College.

With property supplements in recent weeks featuring some 'news' about the impending revival in the commercial property lettings and the alleged reports of crowds of foreign investors flogging to the shores of Ireland, one gets an impression that things are only getting more desperate in the Irish property market.

Irish consumption is dead and household investment has collapsed. Their demise will persist for a long time as the state continues to drain savings and income through taxation and services inflation. Domestic businesses are starved of operating capital, and are in no position to invest as their state and private households customer base is shrinking. Not surprisingly, eight companies per day were going out of business in the first quarter of 2011.

Per latest quarterly national accounts, exports-oriented companies might be starting to cover some depreciation and amortization accumulated over three years of this depression, but any sizeable investment here is unlikely to materialize as long as the Euro crisis rages across the continent. At any rate, the MNCs are big on the exporting side of our national accounts, but our net exports, once repatriated profits are subtracted, accounted for just 3.42% of our GDP in Q1 2011. In other words - no realist today would count on MNCs riding to our rescue any time soon.

In the mean time, our banks and financial services in general will be deleveraging on the orders of regulators, into highly uncertain and risk-averse markets. No market participant outside the 'green jerseys' club in Dublin believes that this process will lead to a normalized lending environment before 2015 at best.

And then there is NAMA which, given its undefined and unchecked objectives and operational means, has the power and incentives to distort property markets for a decade.

All of this is consistent with historical evidence relating to the outcomes of combined occurrences of severe assets busts and debt overhangs in advanced economies. It is taking advanced economies like Japan decades of economic misery to come out of such busts with both monetary and fiscal policy tools at their disposal, plus long-term well-established competitive advantages in global trade.

Ireland has none of these three pillars of recovery.

Courtesy of the Euro we have no control over our interest rates and this time around, unlike post-2001-2002 slowdown, the ECB is not going to be accommodative of Irish need for negative real interest rates. Courtesy of the sky-high Government and quasi-Government debts, we have no fiscal policy pillar left either. Lastly, due to our excessive over-reliance in the past 20 years on MNCs for trade and investment, we have no specialisation of our own when it comes to international trade outside the small food sector. Irish comparative advantage vis-á-vis other small open economies around the world is our corporate tax rate - now much eroded by other countries lowering their taxes, and by the sky-high costs of state-controlled services and utilities. We have no well-anchored indigenous knowledge or skills and no unique specialisation to prevent gradual exits of MNCs activities from Ireland.

All of this adds up to a bleak forecast for Irish property markets both commercial and residential going forward.

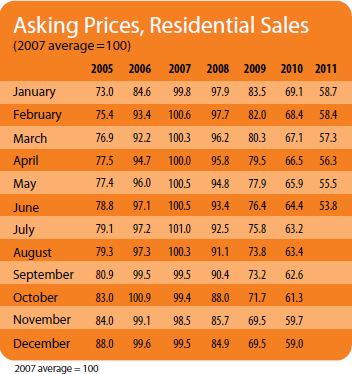

The latest data from daft.ie on asking rents and prices clearly shows that there is some room for continued significant losses in residential real estate. Across all geographies covered in today's report, asking prices continued to fall and these falls are accelerating once again. Nationwide, asking prices are down 5% in three months through June 2011 - the steepest quarterly decline in 18 months.

Greater Dublin areas asking prices are now down between 44% (North County Dublin) and 55% (Dublin City Centre) relative to the peak. Taking assumed 5% average premium over asking prices at the peak and a similar discount today, the swing in prices in the capital is probably between 50% and 60%.

During the Celtic Tiger, city centre properties were the core focus for younger, professional and upwardly mobile families and individuals. These first time buyers were the core of our knowledge-intensive internationally traded services future. The lack of such buyers in the market today, despite growing presence of internationally trading services firms in Dublin and lower unemployment in professional occupations points to two features of our economy. Firstly, our upwardly mobile professionals do not feel confident in their medium-term future here in Ireland. Instead of putting down their roots here, they remain ready to up and move on with their careers abroad. Secondly, much of the new jobs created by the MNCs in traded services are being filled by imported highly mobile talent.

One more slightly technical factor is important to the consideration of the future of the property markets here. Looking at historical monthly data from 2005 through present, continued declines in asking prices are now putting renewed pressure on rents, which remain out of sync with long-term relationship to asking prices.

Using a simple rule of thumb that at the long-term real interest rates of 3% (the scenario toward which we are heading with ECB policies), the ratio of household income to purchase price should be around 2.8:1, the 3 year horizon average property prices projections based on per capita income in Ireland is in the region of €156,000. That is about 13.4% below today's average asking prices, allowing for a 5% sales discount currently - or 57% below the peak.

In other words, the vicious cycle of low yields and collapsing capital gains still has some room to run before Irish property markets can see a sustained stabilisation.

HIGHLIGHTS:

Asking Prices, Residential Sales

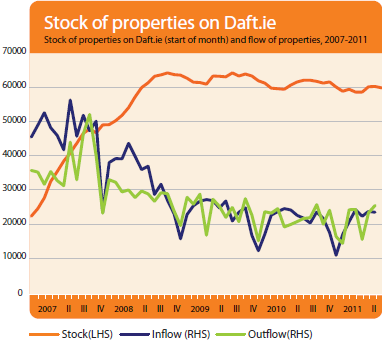

Stock and Flow of Sale Properties

SNAPSHOT:

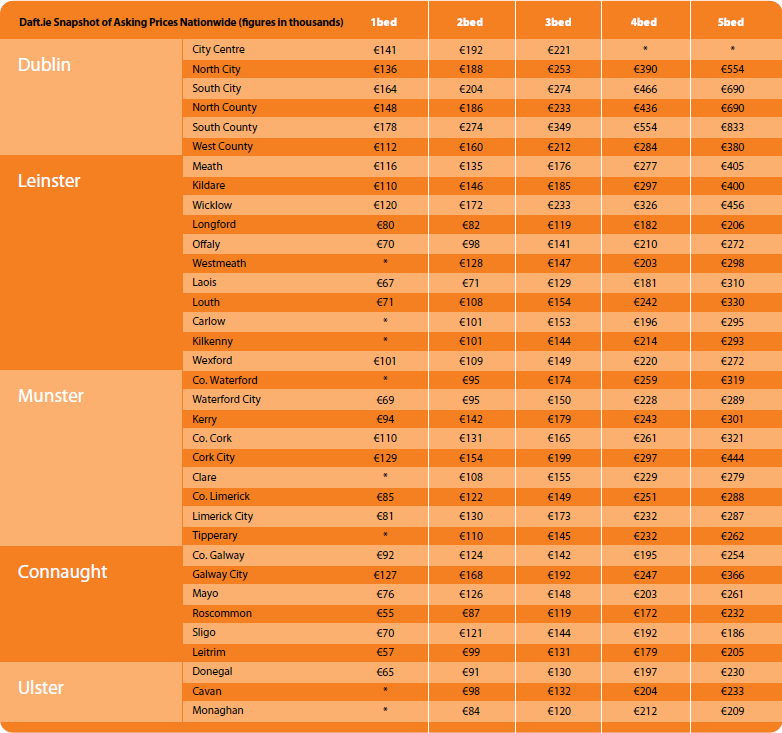

Snapshot of Asking Prices Nationwide