Rent or Buy Decision Swings Towards Home Ownership

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

27th Nov 2007

John McCartney is our guest blogger, commenting on the lastest Daft research on the Irish property market.

With 2007 drawing to a close, and as all sides draw breath in anticipation of Budget 2008, there has never been a more interesting time to 'read the tea-leaves' of the property market. Property accounts for so much of our wealth that numerous indicators have been developed to keep us updated on market trends. Among these, the Daft rental reports are unusual in that they cover both rents and capital values. Interaction between the rental and sales markets is complex but, judging by the latest data, we are now entering an interesting period indeed.

Rental supply down, demand up

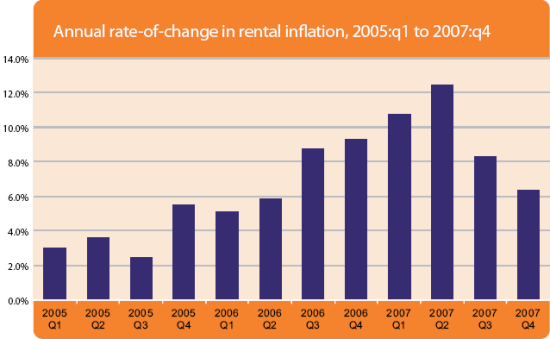

Recent rental trends show a marked contrast to the early years of this decade. Average rents fell by 17% between 2002 and 2003. However the market has recovered since then and year-on-year rental increases have averaged 9.9% over the last 12 months. As ever, this can be explained by supply and demand. Lettings agents report that the supply of good quality rental accommodation has tightened. In part, this reflects higher interest rates and tougher credit conditions for investors. But it also reflects the fact that some landlords were enticed into selling-off their rental properties by the exceptional house prices being achieved in 2006.

While supply is down, the demand for rental accommodation has grown. Rising interest rates and faltering house price growth last Autumn created a 'deflationary psychology' in the minds of would-be buyers. For the first time since 2001 price falls became a realistic possibility and this undoubtedly caused some house hunters to play safe and rent until the market settled down, thereby adding to rental demand. This combination of tightening supply and burgeoning demand has led to a sharp increase in rents, as shown in the Daft rental index.

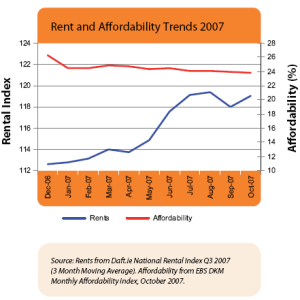

Static rates, falling prices and rising wages mean improved affordability In contrast, however, property prices have fallen. After last year's bumper house price growth, the Daft.ie index shows that asking prices are static, while the ESRI/PTSB index indicates that closing prices are down 4.9% since January. Combined with the ECB keeping base interest rates on hold since June, the costs of servicing a new mortgage have eased. At the same time, net incomes have risen by anything up to 9.25% due to pay increases and tax reform. The impact on affordability has been significant. Mortgage affordability has steadily improved over the course of this year, particularly for first time buyers who benefit from enhanced mortgage interest relief. This trend is illustrated on the right hand axis of our graph using data from the EBS/DKM Affordability Index. At the end of 2006, the average first time buyer's mortgage accounted for 26.4% of disposable income. By October 2007 the figure had fallen to just 23.8% - an affordability improvement of 10%.

Buy-or-rent calculations changing

This leaves us in an interesting place. Generally, households have two tenure choices - they can rent or buy. Over the course of this year the first option has become less attractive due to rising rents. Meanwhile buying has become more appealing due to improving affordability. If this continues, some households will inevitably switch from renting to buying. All else equal, this should lead to a slowdown in rental growth and a pick-up in house prices.

It is difficult to predict exactly when this switch-back might occur, but two conditions would probably have to be in place. Firstly, the absolute gap between mortgage repayments and rent levels would need to become reasonably narrow. However, repayments would not have to sink all the way down to rent levels - most people would be prepared to incur some premium for a home loan because paying down a mortgage leads to ownership of a valuable asset. A second condition is that expectations about future house price growth would need to be positive - no matter how high rents go relative to house prices, buyers will be reluctant to commit if they believe that residential values are going to fall further.

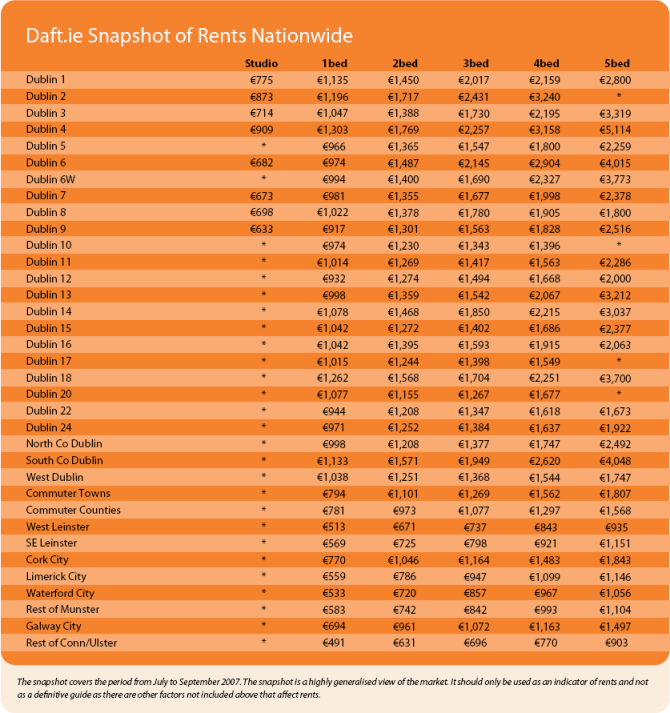

The first of these conditions already appears to have been met. Daft figures show that, while loan repayments remain higher than rents on average, the gap has become quite narrow. Indeed, in some areas like West Dublin where yields are highest and growing most strongly, this gap has been eliminated. Here typical first time buyers face a net loan burden of €1,034 per month for one bed apartments, compared to average rents of €1,038. However, it is too early to say that the second condition - a public perception that house prices have bottomed out - has been met. Average prices fell by 1.3% in October, and despite many economists' assurances that market fundamentals are supportive of medium term house price growth, buyer confidence remains shaky.

Looking forward, I expect rental growth to ease as yields become more challenging. Indeed, this is already happening - annual rent increases have fallen from 16.9% last June to 6.6% in October. In contrast, as buying becomes relatively more attractive, house prices should gain renewed support. Expect this to happen first in areas like West Dublin and Limerick City where high yields make owner occupation more compelling. However this process will not fully take hold until confidence in the housing market recovers. The timing of that is as much a matter of psychology as economics.

HIGHLIGHTS:

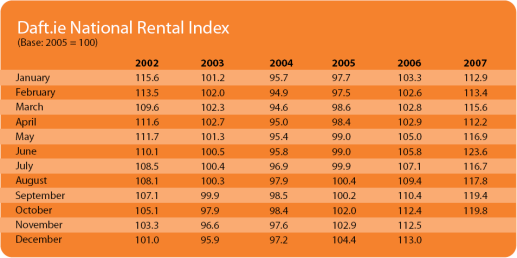

The Daft.ie National Rent Index

Annual rate-of-change in rental inflation, 2005:q1 to 2007:q4

SNAPSHOT:

Average Rents across Ireland in Q3 2007