Property market in Dublin showing signs of stabilisation

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

2nd Apr 2013

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

The Dublin differential - some warning signs for Government

The last 12 months has been one of changes in Ireland's housing market. Cast your mind back to late 2011. Then, asking prices in Dublin were falling at a rate of more than 20%, year-on-year. The year following Ireland's entry into the Troika programme in December 2010 was probably the worst in Ireland's property market crash, with rapidly falling prices and an even more precipitous fall in transactions symptoms of a lack of confidence in Ireland's economic future.

With the launch of this Q1 report for 2013, however, there is a vastly different picture emerging. The Daft.ie asking price index in March 2013 stood just 2.3% lower than a year previously, the slowest pace of price falls since late 2007. The new house price index based on the Residential Property Price Register shows a similar slow-down in house price falls. But that national average hides huge differences around the country.

In South County Dublin, asking prices are now 6% higher than a year ago, a rate of change not seen since early 2007. After 19 straight quarters of falling prices, they have now risen in that area in four of the last five quarters. Prices are also higher, year-on-year, in Dublin city centre and in the South City region, while in the North City region, they are roughly stable (down -0.5% year-on-year).

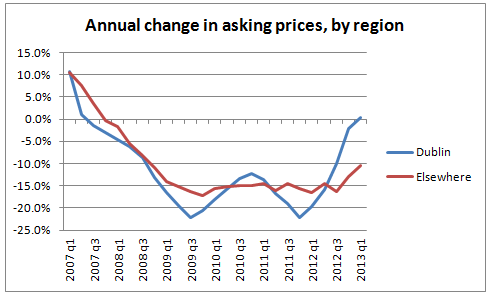

In contrast, in Connacht-Ulster, asking prices are 15% lower now than a year ago. This means that the fall from the peak in Dublin is now smaller than in Connacht-Ulster. The first graph below shows the huge contrast between prices trends in Dublin and those elsewhere. It seemed - from late 2007, when prices in Dublin had started to fall but were still rising elsewhere, to mid-2010, when the rate of decline outside had persistently been lower than in the capital - that house prices in Dublin were being punished for past excesses.

In fact, this was just a result of differences in properties around the country. A key point to remember in Ireland's property crash is that smaller properties have seen larger falls from the peak. Once this is joined up to the fact that Dublin has on average smaller properties than elsewhere, it is easier to see that the apparently larger fall in house prices in Dublin is mostly a reflection of different stocks of property in urban and rural areas.

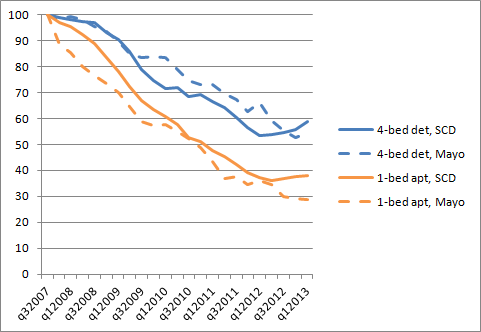

Once the switch is made to a like-for-like basis, a very different picture is emerging. The second graph below shows what has happened prices for two like-for-like properties in South County Dublin (solid line) and in Mayo (the dashed line): a four-bedroom detached house (the orange lines) and a one-bedroom apartment (the blue lines). For all properties, the peak - the third quarter of 2007 - has been set to 100.

First, it is immediately clear just how much prices for smaller properties have fallen by more. Prices for a one-bedroom apartment in South County Dublin are down 62% from the peak while in Mayo they are down almost 72%. In contrast, the price of the detached home is down just over 40% in Dublin and just over 45% in Mayo.

Second, it is also clear how different the trend in prices in South County Dublin (the solid lines) has been from the trend in Mayo, since early 2012. Put another way, the gap between Dublin prices and those elsewhere is growing. In 2007, at the height of the bubble, a 4-bedroom detached home in South County Dublin was 3.2 times the prices of the same property in Mayo. That ratio fell to 2.6 by early 2012 but has since risen - and risen rapidly - to 3.5. Similarly, the price of a 1-bed apartment in South County Dublin was between 2 and 2.5 times one in Mayo throughout the end of the bubble and first years of the crash. In the last 12 months, though, the ratio has increased from 2.2 to 2.8.

This has huge implications for the Government. If prices were still falling, a widening differential would signify that first-time buyers are no longer prepared to sprawl and pay the opportunity and petrol costs of long commutes. But with prices actually rising again and only in certain parts of the country, this may be a signal that not only is this the case, but that also there are not enough properties in Dublin for them. If areas close to jobs and other amenities need new homes, hoping that even more sprawl will solve the problem is not a viable option. Density works well elsewhere - it can work in Ireland too.

HIGHLIGHTS:

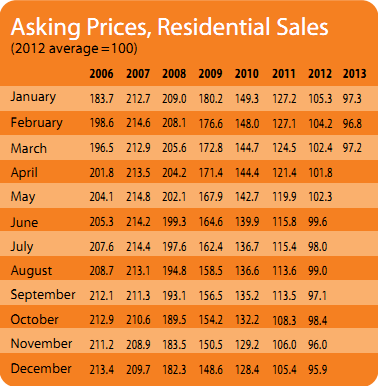

Asking Prices, Residential Sales

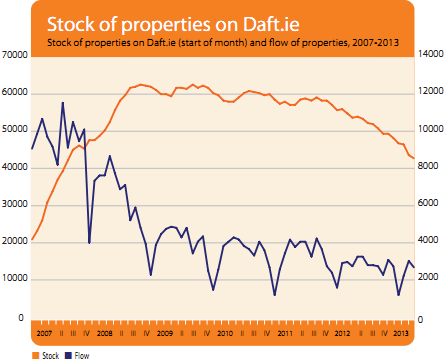

Stock and Flow of Sale Properties

SNAPSHOT:

Snapshot of Asking Prices Nationwide