Chronic supply shortages persist in the rental market

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

11th May 2015

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Chronic supply shortages persist in the rental market

Over the last five years, as Ireland entered and then successfully exited its Troika Programme, the housing market has remained one of the most important topics in social debate. However, the specifics being debated have changed fundamentally. When Ireland entered the Troika Programme in late 2010, this was triggered in part by the fall-out from excessive lending and excessive construction. The problem, in brief, was one of too many houses, rather than too few.

However, as became clear when the latest Census findings were published in mid-2011, Ireland's population continued to grow, even when economic conditions were at their weakest. While we won't know exactly until mid-2016 what has happened with the population since 2011, it seems likely that - with net outward migration easing - population growth has continued apace since 2011. This is highly unusual within a European context and is a "problem" most of our European neighbours would love to have.

What this means for the housing sector is simple: more people mean more dwellings are needed. There was, and still remains in some circles, a belief that vacant homes somewhere in the State are a substitute for vacant homes where they are needed. However, the importance of employment means that cities - as natural job creators - are experiencing the bulk of population growth... but without any building. Dublin's population may grow by as many 100,000 families during the 2010s but, halfway through the decade, fewer than 10,000 new homes have been built in the capital.

In brief, the issue now is most certainly too few homes, rather than too many. This can be seen in a variety of problems faced by Irish society in 2015, from the working homeless to the students whose horizons for higher education are limited by expensive accommodation. It affects those on above-average incomes, who push for more mortgage credit to fight amongst each other for scarce commodities and affects those on below-average incomes, who are stuck between a rental market starved of supply and a moribund social housing sector.

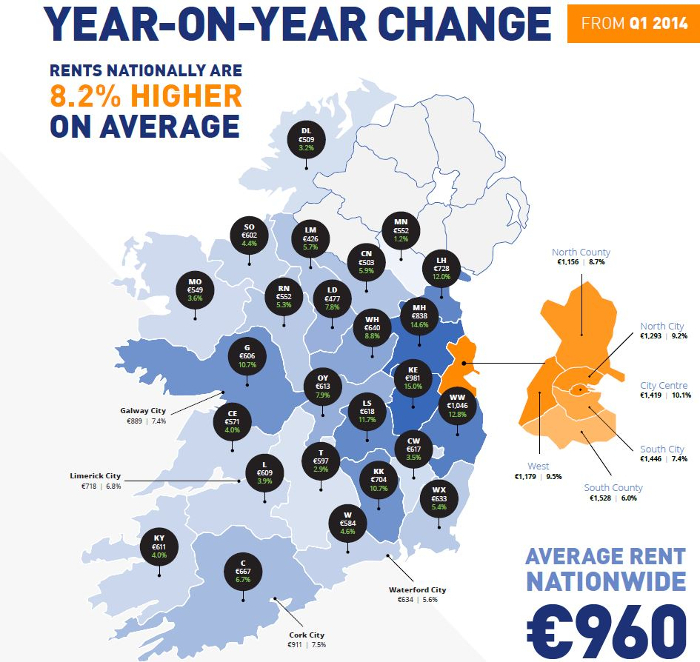

Given this context, the latest Rental Report provides few surprises. In both year-on-year terms and quarterly, rents were higher in the first three months of 2015 across all 35 counties and urban regions analysed in the report. This is the third instance in four quarters of across-the-board quarterly increases. For many counties, particularly in the west of the country, the increase in rents of between 5% and 10% in the last two years reflects an improving real economy, together with a working down of excess supply from the bubble years. But for other areas, rent increases of between one quarter and one third over the last couple of years are far from benign.

In the commentary to the last report, a new trend was highlighted - the worst rates of rental inflation are no longer in the main Dublin markets and have passed instead to its commuter counties. This trend has solidified in recent months. Whereas year-on-year inflation in Dublin rents has eased from 16% to 6% since April 2014, inflation in the Commuter Counties has done the opposite, going from 7.6% in early 2014 to 14% now.

The easing of rental inflation in Dublin has little to do with supply coming on-stream, as the total number of properties on the market at any one time remains unhealthily low. The average number on the market at any one time 2006-2010 was just below 5,000. The current figure is one third of that, and this is a level that has pertained for the bulk of the last 18 months. Whereas 2011 saw almost 60,000 rental properties listed over the course of the year - a little over half of all rental properties in the capital - the last 12 months have seen just 35,000 listed.

As recently as 2006, more than two thirds of Dublin rental properties were listed that year (and almost half of all rental properties nationwide). Even taking the 2011 Census for the stock of rental properties - which is likely to be a conservative estimate of the base - the figure is now less than one third for Dublin and closer to one quarter nationwide. One of the trade-offs for ownership is less mobility, but this is voluntary. In a labour market where mobility matters, we have ended up with a rental market where tenants are afraid to move.

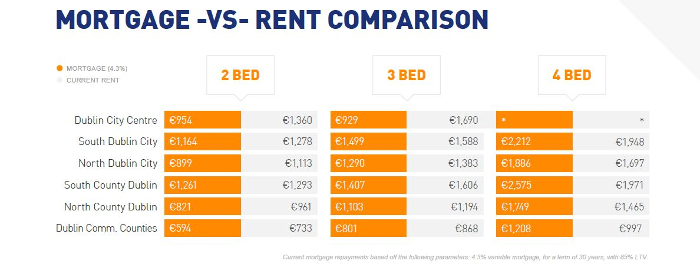

As I have noted on a number of occasions before, the solution to the lack of accommodation is not a cap on rents. This tackles the symptom, not the cause. The solution is to address the high cost of building new homes, whether apartments or houses. Even in a world with free capital (i.e. no profit) and free land, the break-even rent associated with a two-bedroom apartment in Dublin is roughly €1,500 a month. A household earning €45,000 a year can sustainably pay no more than €1,000 a month on its accommodation.

Given the hugely important social and competitiveness implications of the cost of accommodation, it is clear that Ireland - and the greater Dublin area in particular - has a problem: the cost of building homes no longer bears any relation to the real economy. For policymakers, the first step in solving a problem is admitting you have one.