Cacophony of voices shouldn't mask the simple steps to fix housing

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

6th Oct 2014

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Cacophony of voices shouldn't mask the simple steps to fix housing

The latest Daft.ie House Price Report shows a 14% annual rise in asking prices nationally, led in particular by Dublin, but with Leinster and the urban centres of Cork and Galway also showing significant prices increases. The same trend is evident from Property Price Register transactions, where analysis, controlling for location, size and type of the unit, shows a 17% annual rise, again driven by Dublin and Leinster.

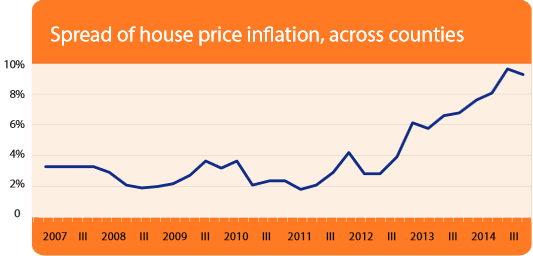

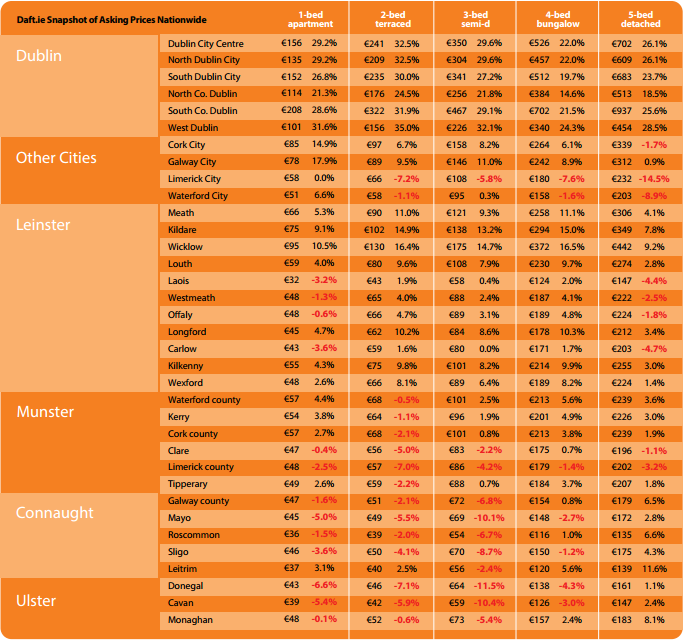

Nonetheless, there remain large swathes of the country which have shown little or no increase in property values in recent quarters. Asking prices are still lower, year-on-year, in Limerick, both county and city, Clare, Mayo, Donegal and Cavan, while in the rest of Munster, Connacht and Ulster outside the cities increases have been small. This has been the case even as values have risen by a third in most parts of Dublin and by more than 40% in both central Dublin and south county Dublin. The graph below shows how spread out house price inflation has become since 2012.

Figure 1. Spread of house price inflation, across counties

Unsurprisingly, such a dysfunctional housing market has attracted a lot of commentary. The first of October saw no less than six reports on the market but perhaps the most important development in recent days has been the Central Bank's intervention. The Central Bank is proposing to limit two key ratios - the loan-to-value (LTV) and loan-to-income (LTI) ratios - in order to prevent a credit-driven bubble from occurring again.

The importance of these measures simply cannot be understated. It is said that you should have 20-20 hindsight about the last crisis and, given Ireland's housing bubble was almost entirely credit-driven, it is frankly somewhat surprising that almost eight years on from the peak of the market, these measures have not been introduced already. While experts can quibble about the exact structure of the limits on LTV and LTI, policymakers and households can go about their business, knowing that, roughly speaking, if first-time buyers save up one year's salary, they will be lent four times that, and can plan accordingly.

Setting the maximum loan-to-value, and potentially also the maximum loan-to-income, is one step in ensuring a healthy housing sector. But the Central Bank's work is not done there. It needs to address the preponderance of variable rate mortgages in Ireland. Ireland is more heavily reliant that any other development country on mortgages whose repayment could increase dramatically in the space of a year. Such mortgages are viewed as Weapons of Financial Destruction in the US, where increasing mortgage repayments played such a crucial role in igniting the housing market downturn that turned into the Great Depression from which Europe in particular is still trying to escape.

Prudential regulation of the mortgage market is about protecting borrowers, banks and taxpayers. This could be achieved by switching to a Danish-style covered bond system. This can be summed up as follows: for a bank to issue 30-year mortgages worth €100m next year, they have to go off to the international capital markets and raise a 30-year bond worth €100m. This tells everyone the real cost of finance and, perhaps more importantly from the Government's point of view, means that the taxpayer need not worry about having to bail out banks.

If credit is one side of the housing market coin, supply is the other. Rationing credit, however sensibly, puts a limit on house prices: indeed, that is the point. To put some (round) numbers on it, suppose the average household has a total income of €50,000 and, when the Central Bank has done its job, can borrow no more than €200,000 with a €50,000 deposit. This sets a cap on the average house price of €250,000.

Clearly, if the average home costs €300,000 to build, nothing will be built. Even if the average home costs €200,000 to build, this is probably at the limit of acceptable profit margins. If the average home costs just €150,000 to build, this should encourage building. And while many view construction with suspicion given the legacy of the last housing bubble, this was the product of tax breaks and easy credit, not a healthy construction sector.

A healthy construction sector is needed to deliver two of Ireland's most important goals: international competitiveness and the human right to shelter. If it is costly to build, it will be costly to rent and FDI projects that might have come to Ireland will find somewhere elsewhere to call home. If it costly to build, the subsidy required from the taxpayer to cover the cost of accommodating those on the lowest incomes will be larger.

The Central Bank has taken the first steps to building a healthy housing sector. It is up to Government to take the next, and find out how much it costs to build a home and how to reduce that without sacrificing quality.

HIGHLIGHTS:

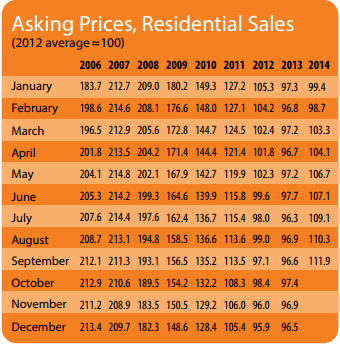

Asking Prices, Residential Sales

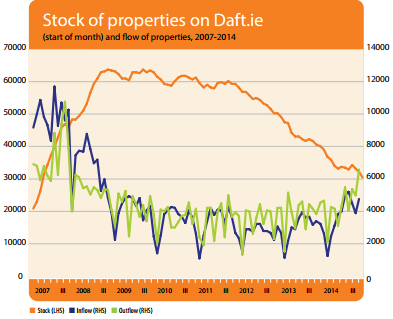

Stock and Flow of Sale Properties

SNAPSHOT:

Snapshot of Asking Prices Nationwide