Falling prices and rising stocks point to adjustments in the housing market in 2007 and 2008

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

10th Jan 2008

Professor Frances Ruane is our guest blogger, commenting on the latest Daft research on the Irish property market.

As we enter 2008, to make sense of the Irish housing market during 2007, it is necessary to consider fundamentals. There are two markets to which all of us relate very strongly - the labour market and the housing market. The labour market determines how we fare - what incomes we earn, what conditions of employment we have, how easy it is to change jobs. The housing market impacts strongly on our standard of living as a major expense in our budget and, in the case of homeownership, it impacts on the value of one of our major assets. These markets are important to the economy as a whole - the labour market determining employment and influencing unemployment, while the health of the housing market is often seen as reflecting the overall health of the economy.

Good house price increases versus bad ones

When both the housing stock and house prices grow gradually over time, this is seen as a positive

indicator of economic well-being. This usually occurs in an environment of income growth and

population growth. When house prices rise rapidly and unsustainably, the situation changes, as

has happened in the Irish house market over the past decade. For many potential home-owners,

houses became unaffordable. So, for example, while many parents have enjoyed real increases in the

value of their housing asset, their adult children have felt excluded from the market as prices rose to

impossible levels. From the perspective of the economy, high and rising prices brought about further

increases in housing supply. This was positive up to a certain point, after which the effect turned

negative, as resources drawn into the sector grew to unsustainable levels.

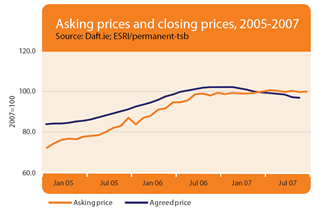

It is not surprising then that the overall reaction to the slowdown in the housing market in 2007 was mostly one of relief, as some level of normality was seen as returning to house price increases. This period has seen a significant shift in expectations about house prices - reflected in both Daft's asking price index, which measures changes in the prices sellers were looking for when placing their houses on the market, and the ESRI/permanent-tsb house price index, which measures the changes in the agreed prices at which houses are sold. While the two indices measure different things, it is possible to compare them - Figure 1 shows the two indices together, with the average for 2007 set to 100.

Asking prices and closing prices compared

As the graph shows, back in early 2005 there was a significant gap in the relative price indices,

compared with their late 2007 levels. The agreed price index was above the asking price index,

showing that the price that sellers typically achieved was above what they initially sought. The

increase in asking-prices began to slow down in 2006, and asking prices have been pretty static

since late 2006. Meanwhile, the index for agreed prices continued to rise until early 2007 and since

then has been in decline. In effect, prior to 2007, the market increase was beating what sellers were

expecting to get, whereas in recent times this pattern has reversed. The different patterns suggest

that sellers' expectations have moved more steadily to the present levels than have actual market

prices. This is consistent with anecdotal evidence that people were expecting to get more than the

asking price up to 2007 and now expect to get less.

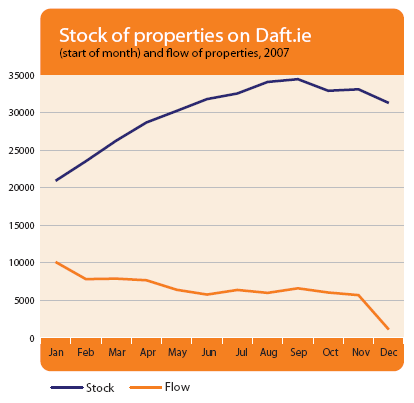

Large increases in stocks around the country

A key addition to the Daft report this quarter is the information on stocks and flows of houses onto the market for each month

in 2007. These data give us some insight into the 'time to sale' of houses on the market. They show that the stock of houses for

sale rose in all areas over the period - so that by January 1 2008 there were on average around 62 percent more houses on the

market than in January, with the lowest increase experienced in Connacht/Ulster (51%).

Interest rates and job prospects hold key to buyer confidence

What of the prospects for 2008 and beyond? To the extent that the recent changes in stamp duty are seen as reducing

uncertainty, they should lead to increased confidence. Economic growth rates will be lower than in previous years but not low

relative to the rest of the EU, and taken with the growth in the population seeking housing should have a positive effect on

demand. The labour market is forecast to show slowly in 2008, with both incomes and employment rising but at a much slower

rate than in recent years. On the other side, threats of increases in the ECB rate have not gone away, and this will lead buyers to

be cautious. Furthermore, buyers may be affected by the credit tightening as banks seek to strengthen their loan portfolios. In

terms of market prices and volumes, the behaviour of builders and developers in releasing stocks for sale will also be important

in certain parts of the market. The ESRI's Winter Quarterly Economic Commentary anticipates that house prices will stabilise

during 2008. While many factors influencing the housing market remain positive, it is the level of confidence felt by consumers

feel over the course of the year that will be crucial in determining the final outcome.

HIGHLIGHTS:

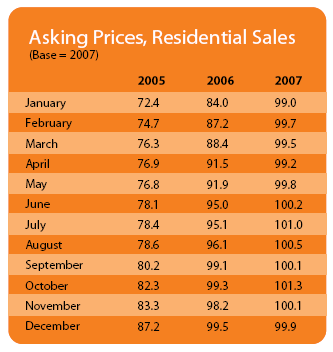

The Daft.ie Asking Price Index |

Stock and flow of properties on Daft.ie, 2007 |

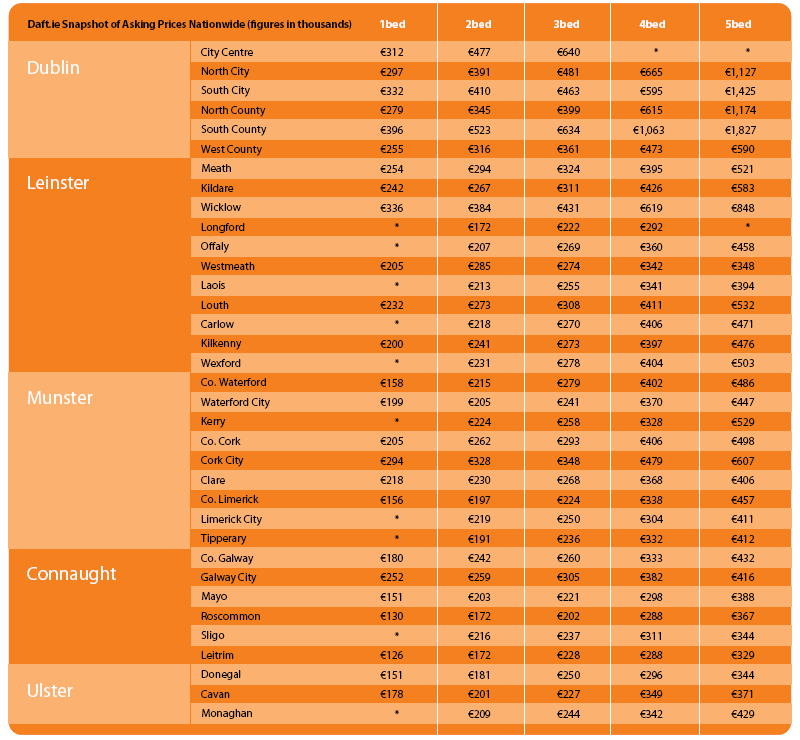

ASKING PRICE SNAPSHOT:

Asking price snapshot across Ireland, 2007 |