Fear factor dominating Ireland's property market

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

3rd Oct 2011

Sheila O'Flanagan is an internationally best-selling novelist and former sovereign bond trader.

The most recent daft.ie property report comes amid turbulent times on stock markets which have seen some of the biggest falls and subsequent rises since the collapse of Lehman Brothers in September 2008. The cause of these roller-coaster rides is the European sovereign debt crisis which is dominating the global economic agenda. European leaders have been trying to deal with a pan-European problem as though it were the responsibility of the few, rather than the many. The markets have seen these efforts as risible and have punished the Eurozone accordingly. However the problems of Europe are also the problems of the world, and leaders of other countries and other economies have begun to put the pressure on European policymakers to get their house in order to avoid a return to global recession.

UK Chancellor George Osborne complained that the international community is 'losing patience' with Europe; in the US both President Obama and his Treasury Secretary Timothy Geithner have tried to galvanise European leaders by saying that the crisis is 'scaring the world' and that the threat of 'catastrophic risk' needs to be taken off the table; Christine Lagarde, recently appointed MD of the IMF, and with an in-depth knowledge of some of the Eurozone's darkest financial secrets, noted that the challenge 'could not be more urgent'.

Until now, stop-gap measures have been made on a regular basis by politicians who are more concerned with approval domestically than the bigger picture, and who therefore disagree over the best course of action. Like the Hydra of Greek mythology, as soon as one disaster is averted by last minute intervention, two more appear in its place. Meanwhile the modern day Greeks protest daily about the austerity measures being imposed upon them and edge ever closer to a sovereign default.

The last few weeks have brought deep pessimism lifted by occasional bouts of (possibly irrational) optimism, and the overall background to world economic issues remains still extremely difficult. Notwithstanding their comments about Europe, both the UK and the US have major debt problems of their own. The fact is that growth and stability are still a long way off for economies that have spent the last decade gorging on debt. During those times, world markets were motivated by greed. They are currently motivated by fear. Fear in markets is much more powerful than greed.

Fear continues to provide the backdrop to the Irish housing market because it is impossible to view it in isolation from all other markets. The rationale for buying a house might be more self-motivating than for equities or commodities, but when the reward is uncertain and the fear is palpable it is a decision that can easily be deferred. Notwithstanding a tendency to seize on any piece of positive news and hope that it signals a return to economic stability if not growth, it is only when the possibility of either being sustainable is evident that the fear of the participants is outweighed by the prospect of reward and they become motivated towards taking action. If the fear factor was taken away, would the Irish domestic market be considered value for prospective home owners? Clearly, the trend has been unremittingly downwards as the bubble-inflated prices of the peak continue to undergo a savage correction. The question now is whether seeing prices at about half their peak-time levels provides a natural floor from which buyers see value again, thus signaling a change in the trend.

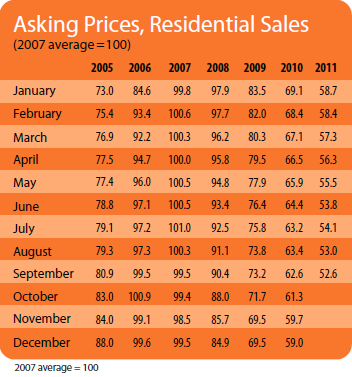

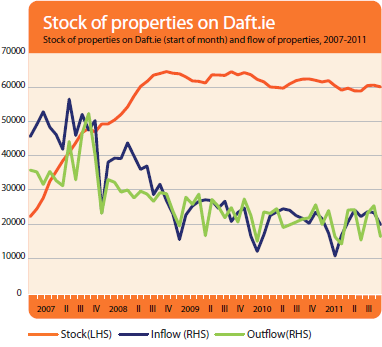

The daft.ie report shows that property prices in Dublin are 53% below their peak valuations. Around the rest of the country, price declines of between 40-50% from the peak are the norm, with only Mayo (37%), Kerry (38.1%) and Limerick City (39.5%) showing smaller declines. As far as corrections go, it's a substantial one. Is it enough? For a real and definitive change to take place in the perception of the housing market in Ireland, a real and definitive change in people's perception of their ability to service mortgages has to take place too. In order for them to make an informed decision, they need to be confident about their long-term employment prospects, the value of their net incomes and the direction of interest rates in the future. The Irish economy continues to lose jobs and the government's troika-led austerity measures continue to affect net incomes which makes it difficult for potential purchasers (and current mortgage holders) to feel confident about their ability to service their debt. However even if they are, they also are faced with an additional problem, the lack of liquidity in the market. This is not the same as a lack of available stock. The stock of houses, at 59,000 is close to the 18 month average and slightly lower than the 62,000 average in 2008-2009. But availability of houses does not equate to a turnover of houses, because the market is constrained by the low level of mortgage approvals by banks who have locked the stable door long after the horse has bolted, and who cannot access international credit markets in a meaningful way. Furthermore, dysfunctional credit markets, courtesy of banks with paranoia about counter-party risk, do not provide a stable background from which a sustained recovery can be made.

The average time a property spends on the market has come down by two weeks since last year, which, for optimists, could provide a level of comfort, although that average hides sharp differences in location: it takes about 4 months for a house to sell in Dublin but 13 months in Ulster. The property bubble was a consequence of plentiful cheap credit and lax lending. Even if the Eurozone leaders finally stop kicking the can down the road, the availability of credit in Ireland is likely to remain extremely limited for the foreseeable future. The market may be near the bottom but it can still spend a considerable amount of time there before the trend changes.

HIGHLIGHTS:

Asking Prices, Residential Sales

Stock and Flow of Sale Properties

SNAPSHOT:

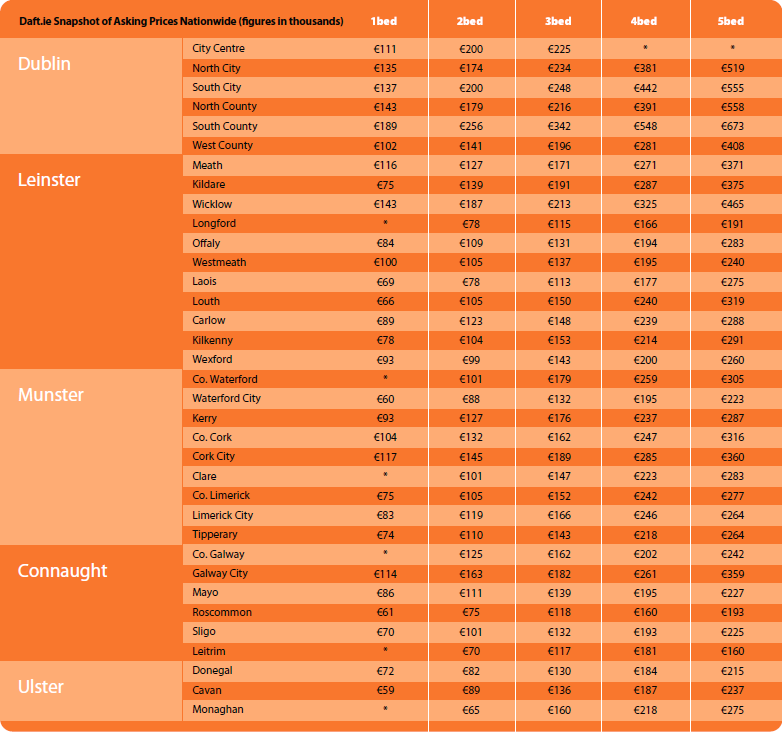

Snapshot of Asking Prices Nationwide