Affordability and confidence pressures mean summer rally will not last

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

5th Jul 2007

Dr. Constantin Gurdgiev is the Head of Research and Strategy for St. Columbanus IA, and Adjunct Lecturer in Finance with Trinity College.

After months of steady, yet to date shallow, house price deflation, the latest figures from the Daft Asking Price Index provide a ray of sunshine. However, the overall market forecast remains gloomy due to structural income growth and credit markets imbalances.

Rental yields on property have been rising since late 2006: the Daft National Rent Index was up by approximately 12% in the year to May 2007, with even stronger gains recorded in the core markets for Dublin city. Rising rents have led to rosy readings of the effect of demographics on the housing market. Such analysis, favoured by some commentators, is a bit too optimistic. Ireland undoubtedly continues to gain from its young population. However, these gains are accounted for by a rising number of Eastern European workers.

While immigration may be providing support for rental prices, foreign workers are employed disproportionately at the lower end of the wage distribution. They are unlikely to settle in the country, meaning their demand for housing is temporary in nature and Spartan in quality. So, rising rental yields signal continued slowdown in the owner-occupier segment of the market.

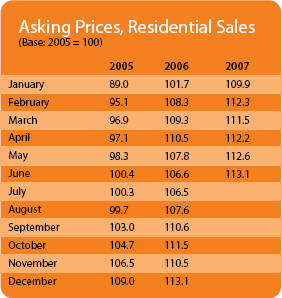

Secondly, house price growth, despite a slight rebound in the asking prices over the three months, remains sluggish. As the ESRI/PTSB closing price figures from late June show, the average price of a second-hand property in Ireland declined by 1.6% during the second quarter of 2007. This suggests an annual fall of 2.7% since January 2007 - in line with forecasts for the entire year. In Dublin, second hand properties prices fell by 3.0% in Q2 2007 - down 5.2% for the year to date.

Some anxiety prior to the elections (fuelled by speculations concerning the stamp duty reform) undoubtedly held back a handful of potential buyers. Yet there is little evidence that this had much of an impact on prices. It is more likely that a rush to sell investment properties, driven primarily by rising interest rates and fears of price depreciation, have created a glut of excess supply at the time of falling demand. A swift, albeit disappointingly shallow, reform of stamp duty does reduce the uncertainty, but it will make little difference to the medium-term price dynamics.

Instead, it is becoming painfully clear that the mixture of adverse affordability shocks and lack of consumer confidence in income fundamentals are driving house prices down in the medium term.

Most of the economic growth over the last 6-9 months has been driven by two factors - robust consumer demand for non-durable, non-capital goods and public expenditure. The former, along with cost hikes in state-controlled services, has triggered runaway inflation. As a result of the latter, the Exchequer figures are now recording rising deficits. For example, the May 2007 exchequer deficit was €266 million, a sharp contrast to the surplus of €1,841 million in May 2006 and suggesting a year-on-year deficit of €2,107 million. The ESRI forecasts a swing this year in the government accounts of €2,822 million, accounted for by slower pace of growth in revenues and out of control expenditure, and bringing the Exchequer into deficit.

This growth in public spending has preciously little to do with disposable income. Earnings growth, having grown 0.4% faster than real GNP, by 5.7%, in 2005 slowed down to 5% in 2006, 2.4% slower than GNP growth. Growth forecasts for 2007 place earnings growth at 3-3.5% - well below real GNP growth.

Factoring out the effects of SSIAs, real personal disposable income is set to rise by 5.2% in 2007 relative to 6.1% in 2006, while household debt is expected to grow from 150% of personal disposable income in 2006 to 160.6% in 2007. At the same time, personal savings will remain robust, growing by 11% in 2005, 9.7% in 2006 and 9.2% in 2007.

Households switching their consumption from durables and investment goods to day-to-day consumption and maintaining strong savings at a time of shallower earnings growth signals that they are now in the precautionary savings mode. This underpins consumers' unwillingness to undertake long-term large-ticket purchases. Altogether, households are not likely to return to the housing markets as buyers any time soon.

The core issue here is affordability. Basic estimates suggest that the median per capita disposable income in the country today stands at around €31,300 per annum. Factoring in the savings rates and using a 4.5:1 ratio of disposable income to loan value, a median household entering the market today can afford a mortgage of between €380,000 and €400,000. The stamp duty, legal fees and costs of moving the household and upgrading properties cut roughly 15 percent from the affordability threshold.

This is a far cry from the latest asking prices - according to Daft's statistics, the average family dwelling in Dublin city ranges from €485,000 to €518,000 for a three bed and from €671,000 to €734,000 for a four bed property.

All of this suggests that we are not likely to see a return of buoyant housing markets any time soon and that the rally in asking prices we're currently seeing will not last.

HIGHLIGHTS:

Daft Asking Price Index (API)

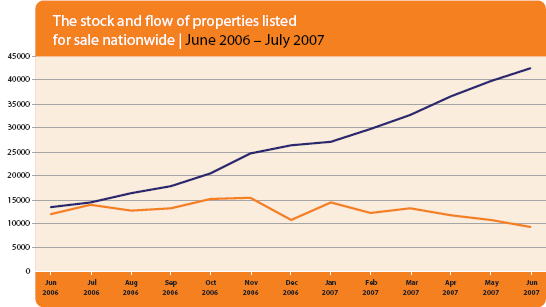

The stock and flow of properties for sale nationwide

SNAPSHOT:

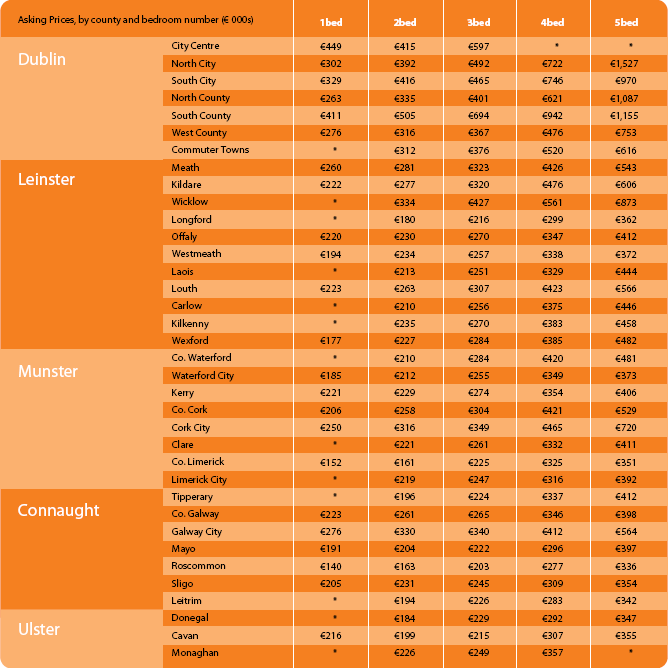

Prices across Ireland in Q2 2007