Housing policy must learn the lessons of the past

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

6th Jan 2014

Ronan Lyons, Daft's in-house economist, commenting on the latest Daft research on the Irish property market.

Housing policy must learn the lessons of the past

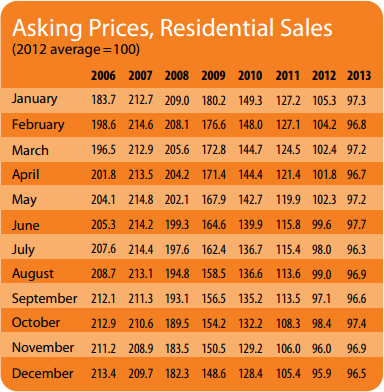

The 2013-in-Review Daft.ie Report out today confirms the on-going trend of a two-tier housing market. Since late 2011, the rate of change in Dublin asking prices has gone from -22% to +11%, with all six regions in the Dublin market now showing strong increases in asking prices in year on year terms. Outside Dublin, the rate of change in asking prices has fallen from the -16% registered in late 2011, but prices are still falling, with an average fall of -6% during 2013.

Such a localised turn-around in housing market conditions, and the huge differences across regions, are by no means unique to Ireland. The US is also characterised currently by prices rapidly rising in some cities but not in others. However, while the economics may be universal, each market has its own unique context.

Recently, Irish politicians and policymakers have expressed concern about rapidly rising house prices. This is encouraging, as it signals an end to the mentality of perceiving house price rises as a good thing. However, as the government prepares to act, it must remember that its previous interventions brought costs, not just benefits. In a market as important as housing, which is the largest chunk of the CPI basket and the biggest asset in most households' portfolios, regulation is required - but it must show an understanding of how housing markets work.

While the exact timing of housing market cycles may forever stump households, policymakers and economists, the underlying economics is straightforward. House prices are the result of three forces: demand and two types of supply, the supply of credit and the supply of dwellings. Demand for accommodation reflects broader economic conditions, in particular the jobs market. Any government that wants to stimulate demand for housing in a meaningful sense must look at jobs.

Where Irish policy got it wrong in the past was thinking that increasing supply of credit was at worst neutral and at best a useful tool for promoting home ownership. If you have the same amount of dwellings and the same amount of households, increasing the supply of credit has the long-run effect of raising the price of housing. By raising wage demands without improving purchasing power, and thus deteriorating Ireland's competitiveness. Where the increase in credit is temporary - as Ireland's was in the run up to 2007 - another effect is creating a housing market cycle and thus large-scale negative equity.

In fairness, policy in the past also recognised the importance of the supply of the housing, as well as the supply of credit. However, housing was built without any consideration of long-run demand. Like all other economies, Ireland depends on its urban centres for creating jobs and wealth. A range of government policies, from decentralisation to the National Spatial Strategy, were predicated on the belief that somehow Ireland was different and that an economy of small towns could compete in a world of cities.

What we are seeing now in the Irish housing market is demand and the two supplies at work. Couples that assess their future and decide to stay in Ireland are overwhelmingly opting to be close to urban centres, and Dublin in particular. So demand is strongest in Dublin. Turning this latent demand into effective demand takes credit and banks are most interested in those couples with lowest risk - they have two incomes and are working in professional services or FDI-dominated sectors. This is why it is the more expensive areas of Dublin that are seeing the biggest increases.

And unlike large parts of the country, Dublin has next to no oversupply from the bubble years left. The vast majority of its "ghost estates" are apartments and even there, most units that are complete are occupied.

So the solution to rapidly rising house prices is simple: Dublin needs more housing. An obvious way to stimulate a one-off increase in supply would be to bring in a tax on the value of empty or derelict sites, not just in Dublin City Council but across the capital. This, indeed, would have been a much smarter property tax than the one brought in last year. But with perhaps as many as 8,000 new units needed in Dublin each year into the medium term, policymakers also need to think about the bigger picture.

A common response is that there is no empty land in Dublin. This misses the point. It's not just about greenfield sites - it's about land use. Why, for example, does the Dublin Industrial Estate take up 170 acres of prime land, close to Tolka Valley Park and Broombridge station, when the city suffers from both a shortage of family homes and a significant overhang of industrial space? (And this, of course, is leaving aside the 600 acres of green fields just around the corner in Dunsink.)

There is plenty of scope for increasing housing supply in the capital, once we as a society not only make better use of empty sites, but are also prepared to re-designate land so that it can be used more effectively and facilitate building up where it pays off. If we are not, we will have to accept that Dublin will increasingly become an enclave for those with the highest incomes

HIGHLIGHTS:

Asking Prices, Residential Sales

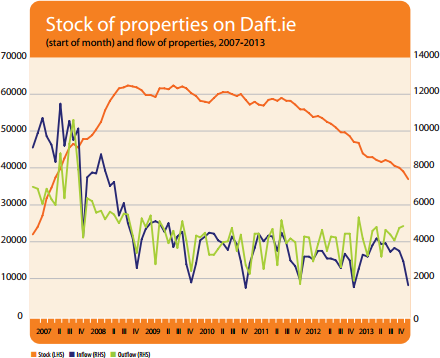

Stock and Flow of Sale Properties

SNAPSHOT:

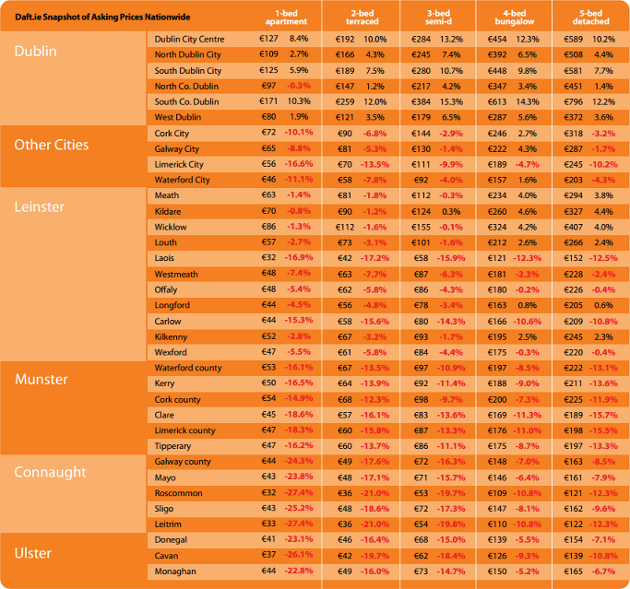

Snapshot of Asking Prices Nationwide