Wealth Report H2 2019 | Daft.ie

Daft Reports

- Ronan Lyons (House Price, Q1 2024)

- Ronan Lyons (Rental Price, Q4 2023)

- Ronan Lyons (House Price, Q4 2023)

- Ronan Lyons (Rental Price, Q3 2023)

- Ronan Lyons (House Price, Q3 2023)

- Ronan Lyons (Rental Price, Q2 2023)

- Ronan Lyons (House Price, Q2 2023)

- Ronan Lyons (Rental Price, Q1 2023)

- Ronan Lyons (House Price, Q1 2023)

- Ronan Lyons (Rental Price, Q4 2022)

- Ronan Lyons (House Price, Q4 2022)

- Ronan Lyons (Rental Price, Q3 2022)

- Ronan Lyons (House Price, Q3 2022)

- Ronan Lyons (Rental Price, Q2 2022)

- Ronan Lyons (House Price, Q2 2022)

- Ronan Lyons (Rental Price, Q1 2022)

- Ronan Lyons (House Price, Q1 2022)

- Ronan Lyons (Rental, Q4 2021)

- Ronan Lyons (House Price, Q4 2021)

- Ronan Lyons (Rental, Q3 2021)

- Ronan Lyons (House Price, Q3 2021)

- Ronan Lyons (Rental, Q2 2021)

- Ronan Lyons (House Price, Q2 2021)

- Ronan Lyons (Rental, Q1 2021)

- Ronan Lyons (House Price, Q1 2021)

- Ronan Lyons (Rental, Q4 2020)

- Ronan Lyons (House Price, Q4 2020)

- Ronan Lyons (Wealth, H2 2020)

- Ronan Lyons (Rental, Q3 2020)

- Ronan Lyons (House Price, Q3 2020)

- Ronan Lyons (Housing, July 2020)

- Ronan Lyons (Housing, June 2020)

- Ronan Lyons (Housing, May 2020)

- Ronan Lyons (Rental, Q1 2020)

- Ronan Lyons (House Price, Q1 2020)

- Ronan Lyons (Rental, Q4 2019)

- Ronan Lyons (House Price, Q4 2019)

- Ronan Lyons (Wealth, H2 2019)

- Ronan Lyons (Rental, Q3 2019)

- Ronan Lyons (House Price, Q3 2019)

- Pierre Yimbog (Rental, Q2 2019)

- Ronan Lyons (House Price, Q2 2019)

- Ronan Lyons (Wealth, H1 2019)

- Ronan Lyons (Rental, Q1 2019)

- Ronan Lyons (House Price, Q1 2019)

- Ronan Lyons (Rental, Q4 2018)

- Ronan Lyons (House Price, Q4 2018)

- Ronan Lyons (Wealth, H2 2018)

- Ronan Lyons (Rental, Q3 2018)

- Ronan Lyons (House Price, Q3 2018)

- Shane De Rís (Rental, Q2 2018)

- Ronan Lyons (House Price, Q2 2018)

- Ronan Lyons (Wealth, 2018)

- Ronan Lyons (Rental, Q1 2018)

- Ronan Lyons (House Price, Q1 2018)

- Ronan Lyons (Rental, Q4 2017)

- Ronan Lyons (House Price, Q4 2017)

- Ronan Lyons (Rental, Q3 2017)

- Ronan Lyons (House Price, Q3 2017)

- Katie Ascough (Rental, Q2 2017)

- Ronan Lyons (Wealth, 2017)

- Ronan Lyons (House Price, Q2 2017)

- Ronan Lyons (Rental, Q1 2017)

- Ronan Lyons (House Price, Q1 2017)

- Ronan Lyons (Rental, Q4 2016)

- Ronan Lyons (House Price, Q4 2016)

- Ronan Lyons (Rental, Q3 2016)

- Ronan Lyons (House Price, Q3 2016)

- Ronan Lyons (School Report, 2016)

- Conor Viscardi (Rental, Q2 2016)

- Ronan Lyons (Rail Report, 2016)

- Ronan Lyons (House Price, Q2 2016)

- Ronan Lyons (Rental, Q1 2016)

- Ronan Lyons (House Price, Q1 2016)

- Ronan Lyons (Rental, Q4 2015)

- Ronan Lyons (House Price, Q4 2015)

- Ronan Lyons (Rental, Q3 2015)

- Ronan Lyons (House Price, Q3 2015)

- Marcus O'Halloran (Rental, Q2 2015)

- Ronan Lyons (House Price, Q2 2015)

- Ronan Lyons (Rental, Q1 2015)

- Ronan Lyons (House Price, Q1 2015)

- Ronan Lyons (Rental, Q4 2014)

- Ronan Lyons (House Price, Q4 2014)

- Ronan Lyons (Rental, Q3 2014)

- Ronan Lyons (House Price, Q3 2014)

- Domhnall McGlacken-Byrne (Rental, Q2 2014)

- Ronan Lyons (House Price, Q2 2014)

- Ronan Lyons (Rental, Q1 2014)

- Ronan Lyons (House Price, Q1 2014)

- Ronan Lyons (Rental, Q4 2013)

- Ronan Lyons (House Price, Q4 2013)

- Ronan Lyons (Rental, Q3 2013)

- Ronan Lyons (House Price, Q3 2013)

- Ronan Lyons (Rental, Q2 2013)

- Ronan Lyons (House Price, Q2 2013)

- Ronan Lyons (Rental, Q1 2013)

- Ronan Lyons (House Price, Q1 2013)

- Ronan Lyons (Rental, Q4 2012)

- Ronan Lyons (House Price, Q4 2012)

- Lorcan Sirr (Rental, Q3 2012)

- Padraic Kenna (House Price, Q3 2012)

- John Logue (Rental, Q2 2012)

- Ronan Lyons (House Price, Q2 2012)

- Barry O'Leary (Rental, Q1 2012)

- Seamus Coffey (House Price, Q1 2012)

- Joan Burton (Rental, Q4 2011)

- Ronan Lyons (House Price, Q4 2011)

- Philip O'Sullivan (Rental, Q3 2011)

- Sheila O'Flanagan (House Price, Q3 2011)

- Rachel Breslin (Rental, Q2 2011)

- Constantin Gurdgiev (House Price, Q2 2011)

- Cormac Lucey (Rental, Q1 2011)

- Eoin Fahy (House Price, Q1 2011)

- Lorcan Roche Kelly (Rental, Q4 2010)

- Ronan Lyons (House Price, Q4 2010)

- John Fitzgerald (Rental, Q3 2010)

- Patrick Koucheravy (House Price, Q3 2010)

- Gary Redmond (Rental, Q2 2010)

- Jim Power (House Price, Q2 2010)

- Jill Kerby (Rental, Q1 2010)

- Brian Lucey (House Price, Q1 2010)

- Michael Taft (Rental, Q4 2009)

- Alan McQuaid (House Price, Q4 2009)

- Dr. Charles J. Larkin (Rental, Q3 2009)

- Emer O'Siochru (House Price, Q3 2009)

- Ronan Lyons (Rental, Q2 2009)

- Oliver Gilvarry (House Price, Q2 2009)

- Brian Devine (Rental, Q1 2009)

- Dr. Liam Delaney (House Price, Q1 2009)

- Gerard O'Neill (Rental, Q4 2008)

- Ronan Lyons (House Price, Q4 2008)

- Dr. Stephen Kinsella (Rental, Q3 2008)

- Moore McDowell (House Price, Q3 2008)

- Shane Kelly (Rental, Q2 2008)

- Fergal O'Brien (House Price, Q2 2008)

- Eoin O'Sullivan (Rental, Q1 2008)

- Dermot O'Leary (House Price, Q1 2008)

- Dan O'Brien (Rental, Q4 2007)

- Frances Ruane (House Price, Q4 2007)

- John McCartney (Rental, Q3 2007)

- Ronnie O'Toole (House Price, Q3 2007)

- Ronan Lyons (Rental, Q2 2007)

- Constantin Gurdgiev (House Price, Q2 2007)

- Fintan McNamara (Rental, Q1 2007)

- Rossa White (House Price, Q1 2007)

- Geoff Tucker (Rental, Q4 2006)

- Damien Kiberd (House Price, Q4 2006)

- Pat McArdle (House Price, Q3 2006)

- Marc Coleman (House Price, Q2 2006)

- David Duffy (House Price, Q1 2006)

- Austin Hughes (House Price, Q4 2005)

- David McWilliams (House Price, Q2 2005)

15th Dec 2019

An analysis of recent trends in the premium property market in 2019

Housing forms a huge part of Irish wealth. For this reason, its ups and downs - of which there seem to be many - are followed by far more than would follow the ups and downs of the Irish stock market. This report takes a closer look at Ireland's housing wealth, at both an aggregate level and from the perspective of individual homes and streets.

First off, the aggregate wealth in Irish housing continues to rise. The value of all residential real estate in Ireland, as of 2019Q3, is estimated to be €519bn. This is an increase of 60% from the low-point reached in late 2013, when Ireland's housing was worth just under €325bn. Most of the increase since late 2013 has been from average prices rising again. However, in recent quarters, the driver of added housing wealth has shifted.

In the last 12 months, Ireland's housing wealth has increased by just 1%, or €5.3bn. Almost all of this increase - just over €5.1bn - has come from newly built homes adding to the stock of housing. The much more modest increase in the average value of all homes - €1.1bn - is almost entirely offset by losses due to depreciation and obsolescence (€0.9bn).

While Ireland's homeowners may disagree, adding extra housing wealth through building more homes - rather than pushing up the value of existing homes - is the healthier way of doing so, at least in a country where there is strong demand for accommodation. There is, of course, a link between the two: the more new homes are built, the less likely it is that the value of existing homes will soar.

A second aspect of housing wealth that relates to public policy is property taxation. Ireland has one of the lowest rates of annual property taxation in high-income countries. It is debated but certainly reasonable to argue that Ireland's relatively weak local authorities and municipalities are as weak as they are because property taxes are so low.

In the typical high-income country, roughly 1% of housing wealth is taxed each year. The rate is as high as it is in part because real estate is immobile - property tax is basically impossible to avoid, unlike taxes on other forms of wealth. It is also as high as 1% in most of Ireland's peers because it is the principal way that local services are funded. The exact list of local services funded varies hugely by country, but it may fund schools, public transport and healthcare services, as well as other services, such as libraries and green spaces.

Ireland's 'Local Property Tax' (LPT) generated €482m in revenue in 2018. This is less than 0.1% of all housing wealth. In theory, the rate of property tax in Ireland is 0.18% - but this is 0.18% of its mid-2013 value, when prices were effectively at their lowest. In addition, property owners 'self-assessed' the value of their homes and, being charitable, it is unlikely that many property owners erred on the side of too high a value by mistake.

If Ireland's LPT were at 1% of market value, as in many of its peers, and updated regularly, property tax would bring in €5.2bn, rather than €0.5bn. In other words, by choosing such a low rate of property tax, the Irish state - and more specifically its local authorities - are foregoing over 90% of potential revenues!

Some might argue against further taxes but the overall level of taxation is a separate point to the composition of taxation. If society agreed that the overall tax take was high enough, then it could simply redirect taxation away from labour, which would stimulate employment, or from consumption, which would benefit those on lowest incomes, as VAT is regressive.

So much for the big picture issues. The report also covers some more local issues, including which markets are the most expensive by region - and which are the cheapest in the country. The honour of the country's cheapest housing market remains with Ballaghaderreen, in Roscommon, which is still the only market in the country where average property values remain below €100,000. Meanwhile at the top end of the market, values have fallen back slightly over the last few months - not least because of the new supply coming on at higher price points.

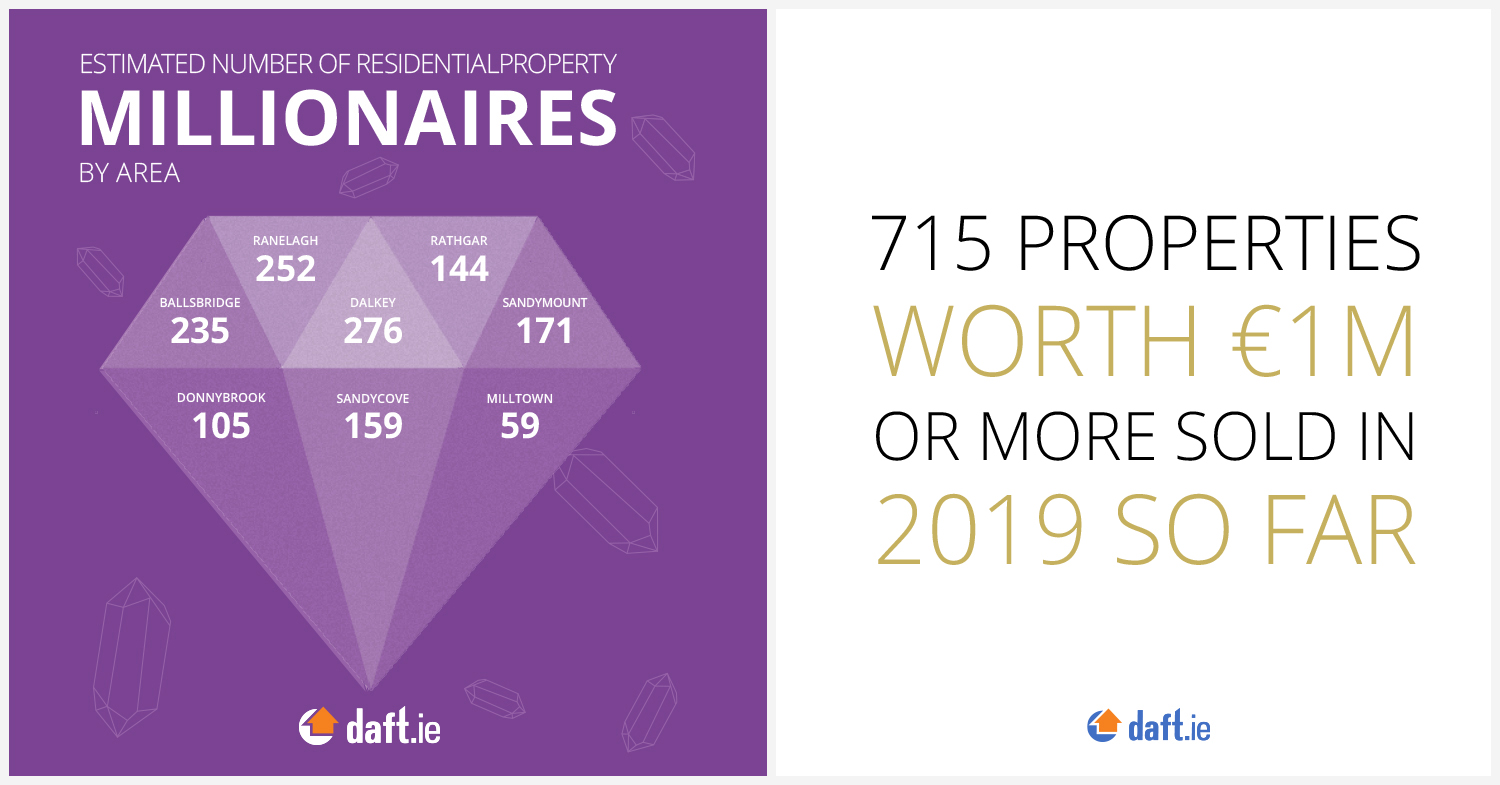

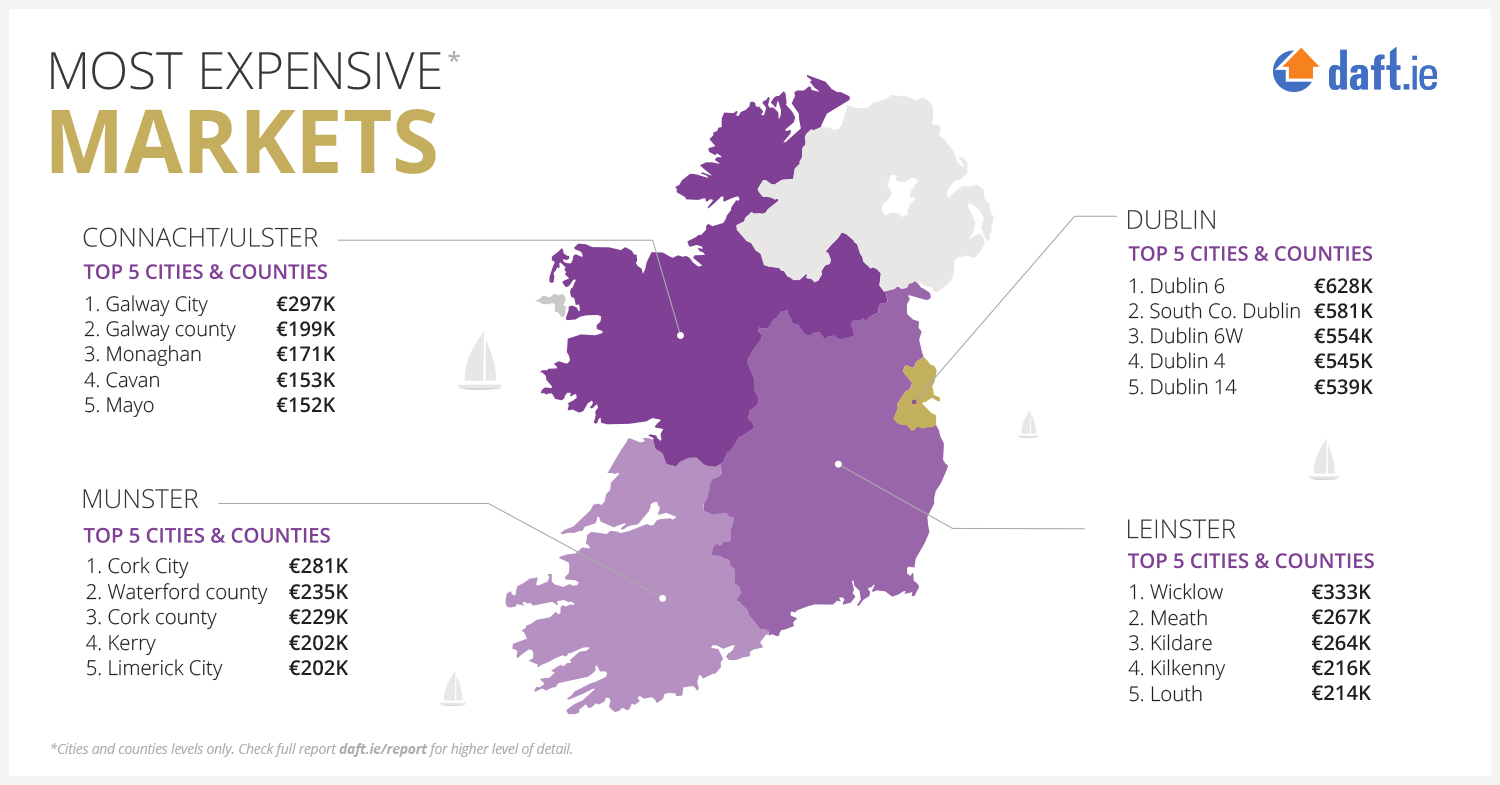

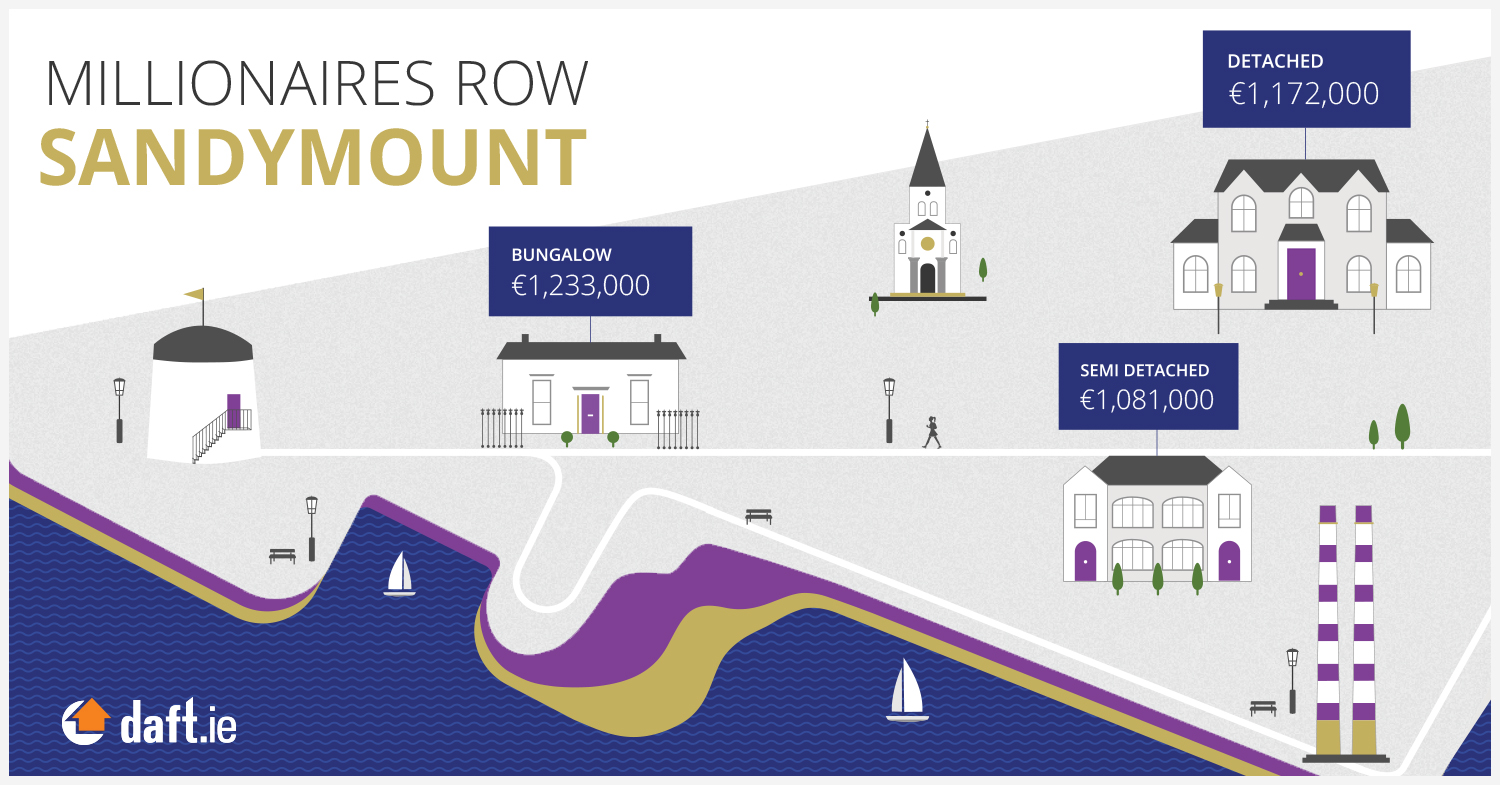

The most expensive markets remain concentrated in Dublin, with Mount Merrion, Dalkey and Sandycove making up Ireland's three most expensive markets. Foxrock and Sandymount round out the top five - and all five have average prices above €700,000. In part, that is because those areas have far fewer smaller properties than some other markets, especially those in Dublin 4 and 6.

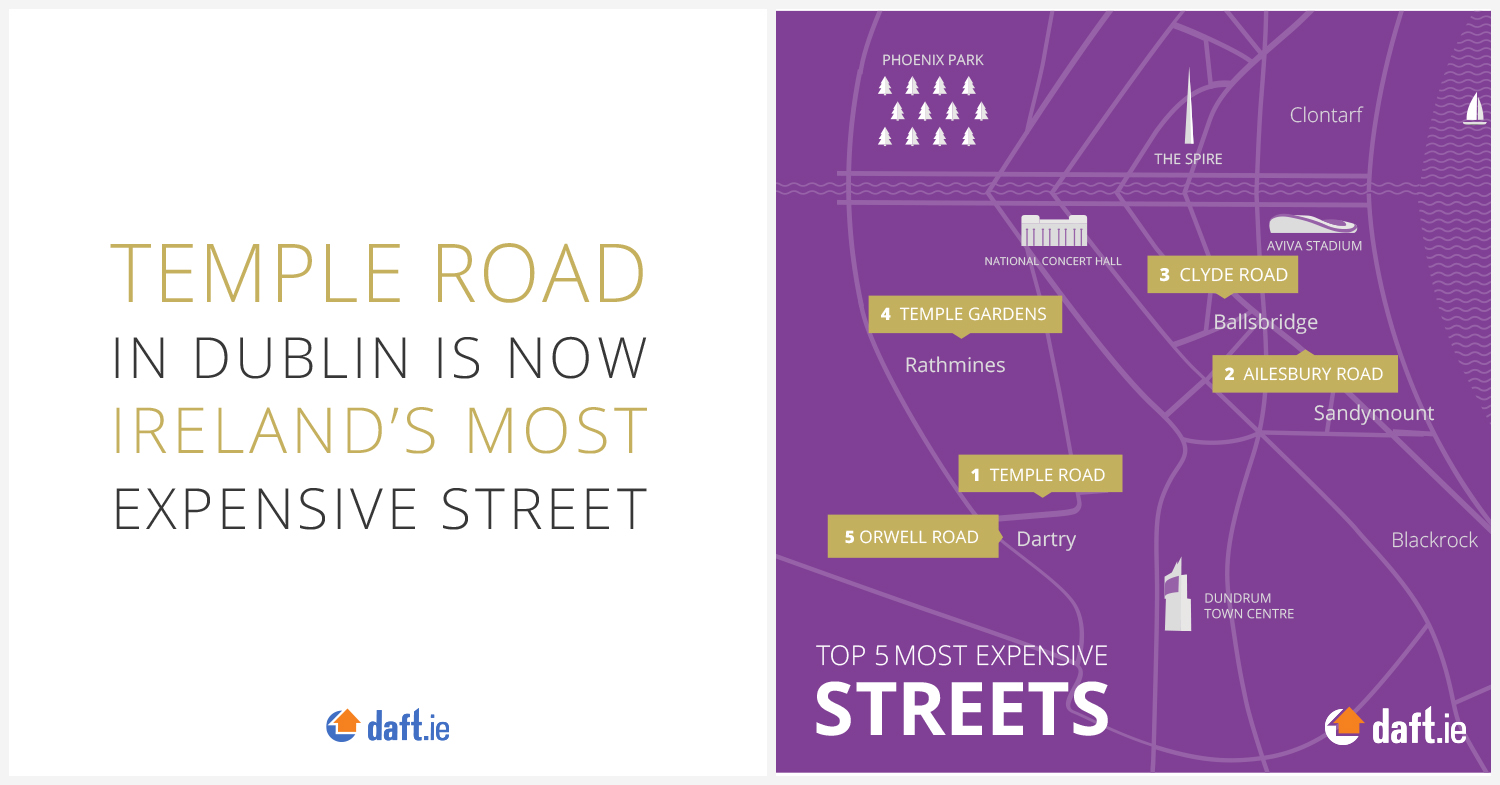

However, when looking at the most expensive streets in the country, Dublin 4 and Dublin 6 dominate. Eleven streets had two or more transactions of €2m or higher for individual properties in 2019, so far. Four of those streets are in Dublin 6. This includes Ireland's most expensive street, Temple Road, which had three properties trade for more than €2m, with an average price tag of €5.5m. Neighbouring streets Temple Gardens, Orwell Road and Palmerston Road also feature in the list - as does Leinster Road, not too far away. Three of the other top ten streets are in Dublin 4 - Ailesbury Road and Clyde Road, which rank 2nd and 3rd, and Park Avenue.

As the country heads into the 2020s, and homes continue to get built, it remains to be seen how the increase in the number of properties compares with the change in average values. From society's perspective at least, more is merrier.

Methodology:

The Daft.ie Wealth Report is based primarily on the output of hedonic price regressions, which reveal average property values for particular classes of property. This can be broken down by period, location and dwelling attribute (such as size or type). To calculate average prices by city or county, these averages by class are weighted by the class frequency to give a meaningful average price by location. For example, Dublin 1 will be more weighted to 1-bedroom apartments than Leitrim, which will be weighted more towards 4- and 5-bedroom bungalow and detached properties. The same methodology allows an estimate of the total number of property millionaires in Ireland, as follows: for each of the 389 micro-market in the country, the average value of 25 main property types, from 1-bed apartment to 5-bed detached, is calculated, giving the average value for almost 10,000 property segments. The number of property millionaires was calculated by focusing on the 43 segment where the average property value was at least €1m and adding up, based on Census information and the Daft.ie listings archive, the total number of dwellings in this segment. The Property Price Register was used to calculate the most expensive streets, with exclusions based on transactions concerning sites for development or containing multiple units.